Bloomin' Brands (BLMN), Mid/Small Cap AI Study of the Week

May 30, 2024

Weekly AI Pick from the S&P 400 or S&P 600

Company Overview

Bloomin' Brands, Inc. is a significant entity in the global casual dining sector, operating well-known restaurant brands such as Outback Steakhouse, Carrabba's Italian Grill, Bonefish Grill, and Fleming's Prime Steakhouse & Wine Bar. As of the end of 2023, the company managed 1,189 company-owned and 291 franchised restaurants across the U.S. and international markets. The business is divided into two main segments: U.S. operations, with nearly 1,150 restaurants, and international operations, encompassing 330 restaurants. Key growth strategies include new restaurant openings, especially the smaller-scaled Outback Steakhouse "Joey" design, and extensive remodeling projects aimed at enhancing guest experiences and operational efficiency. International expansion, particularly in emerging markets like Brazil, is a crucial focus area.

Revenue is primarily generated through company-owned restaurant sales and franchise rights, along with royalties and fees from franchised locations. The company emphasizes cost efficiencies through a global procurement strategy and has invested significantly in technology to support operations, enhance customer experience, and optimize supply chain management. Marketing efforts include public relations programs, national promotions, and digital strategies tailored to local markets. The reintroduction of the "No Rules, Just Right" platform at Outback Steakhouse and the Dine Rewards loyalty program are notable initiatives to attract and retain customers.

Bloomin' Brands is committed to sustainability and food safety, maintaining stringent supplier standards, and leveraging technology for digital marketing, online ordering, and business analytics. The company also emphasizes regulatory compliance, covering labor laws, food safety, and data privacy, and fosters a diverse and inclusive work environment. Employee training in ethics, discrimination prevention, and anti-bribery is prioritized, along with supporting a hybrid work environment to enhance connectivity between corporate and field teams.

The leadership team, led by CEO David Deno since April 2019, includes experienced executives like CFO Christopher Meyer, Chief Supply Chain and Operations Excellence Officer Lissette Gonzalez, and Chief Technology Officer Astrid Isaacs. The company also engages with the community through volunteer programs, charitable donations, and partnerships promoting diversity and inclusiveness. Comprehensive benefits and rewards are provided to motivate and retain employees, including competitive salaries, health and wellness programs, retirement plans, and employee assistance programs.

By the Numbers

Annual 10-K Report Summary for 2023:

- Total revenues: $4,607.4 million, up 5.8% from $4,352.7 million in 2022.

- Operating income: $325.1 million, down from $330.4 million in 2022.

- Operating margins: 7.0%, down from 7.5% in 2022.

- U.S. combined comparable restaurant sales: +1.4%.

- Outback Steakhouse comparable restaurant sales: +1.1%.

- Diluted earnings per share: $2.56, up from $1.03 in 2022.

- Net income attributable to Bloomin’ Brands: 5.3% of total revenues, up from 2.3% in 2022.

- Food and beverage costs: Decreased as a percentage of restaurant sales.

- Labor costs: Increased due to wage inflation.

- Average restaurant unit volumes: Increased across all brand segments.

- General and administrative costs: Increased due to higher legal fees, compensation, travel, and incentives.

- Net interest expense: Remained flat.

- Effective income tax rate: Decreased due to temporary Brazilian tax legislation.

- U.S. revenue: $4,053.6 million, up from $3,911.9 million in 2022.

- International revenue: $617.9 million, up from $504.6 million in 2022.

- Restaurant-level operating income: $746.3 million, up from $676.9 million in 2022.

- Adjusted restaurant-level operating income: $742.1 million, up from $682.8 million in 2022.

- Adjusted net income: $268.2 million, up from $232.9 million in 2022.

- Adjusted diluted earnings per share: $2.93, up from $2.52 in 2022.

- Franchise sales: $1,030 million, up from $964 million in 2022.

- Cash and cash equivalents: $111.5 million.

- Outstanding credit facilities: $785.8 million.

- Unused borrowing capacity: $599.2 million.

- Anticipated capital expenditures for 2024: $270-$290 million.

- Dividends paid in 2023: $83.7 million.

- Shares repurchased in 2023: $70 million.

- New share repurchase authorization for 2024: $350 million.

Quarterly 10-Q Report Summary for Q1 2024:

- U.S. combined comparable restaurant sales: -1.6%.

- Outback Steakhouse comparable restaurant sales: -1.2%.

- Total revenues: $1,179.5 million, down 4.0% from $1,228.2 million in Q1 2023.

- Operating income: $77.1 million, down from $120.6 million in Q1 2023.

- Operating margins: 6.4%, down from 9.7% in Q1 2023.

- Restaurant-level operating margins: 16.0%, down from 17.9% in Q1 2023.

- Diluted loss per share: $(0.96), down from earnings of $0.93 per share in Q1 2023.

- Average weekly unit volumes for Outback Steakhouse in the U.S.: $83,012, down from $84,506.

- Number of restaurants: 1,451, down from 1,471 year-over-year.

- U.S. segment revenues: $1,043.1 million, down from $1,092.9 million in Q1 2023.

- Income from operations in the U.S.: $97.5 million, down from $133.2 million in Q1 2023.

- International segment income from operations: $15.76 million, down from $24.5 million in Q1 2023.

- Net loss attributable to Bloomin' Brands: $83.9 million, down from net income of $91.3 million in Q1 2023.

- Cash and cash equivalents: $131.7 million.

- Total credit facilities: $955.7 million.

- Unused borrowing capacity: $346.7 million.

- Common stock repurchased under ASR agreement: $220 million.

- Remaining available under the 2024 Share Repurchase Program: $130 million.

- Net cash provided by operating activities: $73.8 million, down from $189.7 million in Q1 2023.

Stock Performance and Technical Analysis

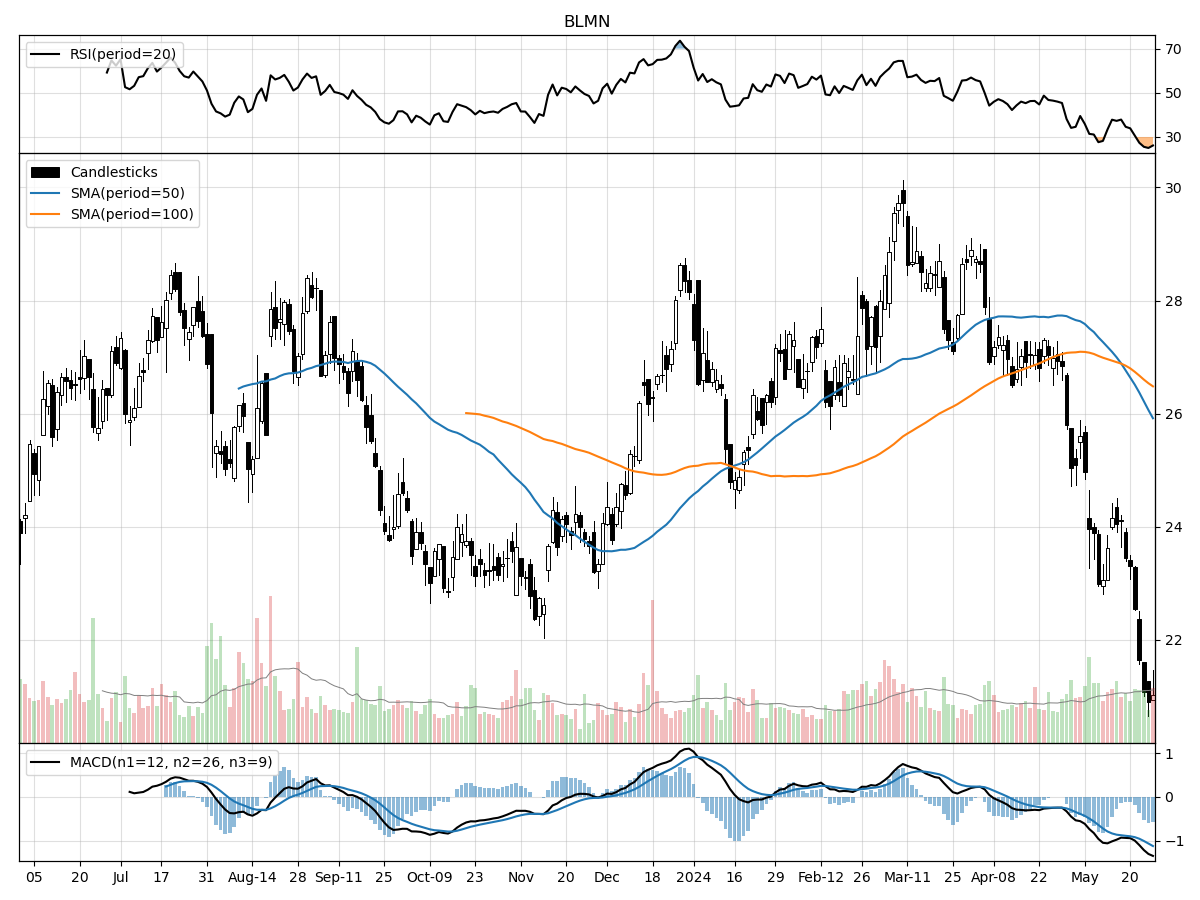

Based on the current technical analysis, there are several indicators that suggest a The technical analysis of a stock involves using historical prices, volumes, and other market indicators to forecast future price movements. In the case presented, the stock is currently trading at $21.02, which is at the same level as its 52-week low. This might suggest that the stock is potentially undervalued or that it has been experiencing a significant downtrend, and investors have not yet found a reason to push the price up. The fact that the current price is 29% below its 52-week high could indicate that the stock has room for an upside if the market sentiment turns positive or if there are favorable changes within the company or industry.

Volume analysis shows that recent daily volumes are higher than the longer-term average, which could signal increased investor interest or heightened activity due to recent news or events. However, given the price has fallen by 18.5% in the last month and 26.1% over the last three months, the higher volume might be associated with selling pressure rather than buying interest.

Money Flow indicators suggest the stock is under heavy selling pressure and is experiencing distribution, meaning that shares are moving from accumulation (buying) to distribution (selling), which is typically considered a bearish signal. The Moving Average Convergence Divergence (MACD) is also bearish at -1.12, which implies that the short-term momentum is lower than the long-term momentum, reinforcing the potential downtrend.

The confluence of these technical indicators—price at a 52-week low, high selling volume, bearish money flow, and a negative MACD—suggests that the stock is currently facing significant bearish sentiment. Before making an investment decision, one should consider whether these indicators align with broader market conditions, the company's fundamental health, and potential catalysts that could reverse the downtrend. It is also important to consider risk tolerance and whether the stock's current position aligns with the investor's strategy for capitalizing on potential undervalued conditions or if it indicates a deeper underlying issue with the company.

The ‘Bull’ Perspective

- Strategic Positioning for Recovery: Despite a decrease in comparable restaurant sales, Bloomin' Brands has demonstrated strategic resilience, positioning itself for recovery through cost management and operational efficiency.

- International Growth Prospects: The company's significant growth in international markets, especially the 14.3% rise in Brazil, indicates potential for global expansion and revenue diversification.

- Aggressive Share Repurchase Program: Bloomin' Brands' commitment to returning value to shareholders is evident through its aggressive stock buyback program, with $220 million repurchased and $130 million remaining under the 2024 Share Repurchase Program.

- Adaptation to Market Trends: The company's continuous adaptation to evolving consumer preferences and investment in technology initiatives are key drivers for future growth and competitiveness.

- Robust Financial Management: Despite the current headwinds, Bloomin' Brands' strong balance sheet, with $131.7 million in cash and cash equivalents and a total credit facility of $955.7 million, showcases robust financial management and resilience.

Strategic Positioning for Recovery

Bloomin' Brands' recent performance has undeniably faced headwinds, with a 1.6% decrease in U.S. combined comparable restaurant sales and a 4.0% drop in total revenues year-over-year. However, it's essential to look beyond these figures and recognize the strategic maneuvers the company is undertaking. The exploration of strategic alternatives for its Brazil operations, for instance, could unlock significant value and streamline the business. Moreover, the company's focus on operational efficiency, as evidenced by the management of its restaurant portfolio and the optimization of its cost structure, positions it well for a bounce-back as market conditions improve. With a strategic emphasis on high-margin offerings and an improved customer experience, Bloomin' Brands is laying the groundwork for sustainable recovery and profitability.

International Growth Prospects

Bloomin' Brands has not only maintained a foothold in the competitive U.S. market but has also seen impressive international performance, particularly in Brazil, where comparable sales surged by 14.3%. This international success is a testament to the brand's global appeal and its ability to cater to diverse consumer tastes. The potential sale of the Brazil operations could provide a significant influx of capital, which could be redeployed into other growth initiatives or used to strengthen the company's balance sheet further. Additionally, the company's international presence mitigates the risk of overreliance on the U.S. market and provides a buffer against domestic economic fluctuations.

Aggressive Share Repurchase Program

A strong indicator of Bloomin' Brands' confidence in its future is the aggressive share repurchase program, with $220 million of common stock already bought back. Share buybacks signal to the market that the company believes its stock is undervalued and that it is committed to enhancing shareholder value. The remaining $130 million available for repurchases under the 2024 Share Repurchase Program provides additional support for the stock price and reflects the company's robust capital allocation strategy. Share repurchases also contribute to earnings per share (EPS) accretion, providing a direct benefit to investors.

Adaptation to Market Trends

In the face of shifting consumer preferences and a highly competitive landscape, Bloomin' Brands has shown a commitment to staying relevant and competitive. By leveraging technology and data analytics, the company is enhancing the customer experience and operational efficiency. Investments in digital marketing, menu innovation, and customer engagement platforms are critical to driving traffic and customer loyalty. The company's ability to quickly adapt to market trends, such as the growing demand for delivery and takeout options, positions it well to capitalize on evolving dining habits.

Robust Financial Management

Despite a challenging quarter, Bloomin' Brands' solid financial position, marked by $131.7 million in cash and cash equivalents and significant credit facilities, demonstrates the company's financial resilience. The management team's prudent financial stewardship has ensured a strong liquidity position to weather economic uncertainties. Additionally, the company's proactive approach to debt management, as evidenced by the partial repurchase of 2025 Notes, reflects a strategic focus on optimizing its capital structure. The ability to generate $73.8 million in net cash from operating activities, even in a tough quarter, underscores the underlying strength of Bloomin' Brands' business model.

In conclusion, while Bloomin' Brands faces industry-wide challenges, its strategic initiatives, international growth, shareholder-friendly actions, market adaptability, and solid financial management indicate a strong foundation for future success. For investors seeking a resilient opportunity with potential upside, Bloomin' Brands presents a compelling case for inclusion in a diversified investment portfolio.

The ‘Bear’ Perspective

Bearish Outlook on Bloomin' Brands, Inc. Amidst Challenging Market Conditions

- Declining Sales and Earnings: Bloomin' Brands reported a 1.6% decrease in U.S. combined comparable restaurant sales and a significant drop in diluted earnings per share from $0.93 to a loss of $(0.96).

- Operational Challenges: The company's operating income plummeted by 36% year-over-year, with a notable margin contraction from 9.7% to 6.4%.

- Market and Competition Risks: Intense competition and evolving consumer preferences are putting pressure on market share and profitability.

- Supply Chain and Cost Pressures: Rising commodity and labor costs, coupled with supply chain vulnerabilities, threaten to erode margins further.

- Regulatory and Environmental Concerns: Compliance with stringent regulations and the demand for sustainable practices could lead to increased operational costs.

- Declining Sales and Earnings

Bloomin' Brands has shown troubling signs with its latest quarterly report, as U.S. comparable restaurant sales have dipped by 1.6%. More alarmingly, the diluted earnings per share took a sharp turn from a positive $0.93 in the previous year to a loss of $(0.96). This stark reversal highlights underlying issues in the company's profitability and raises concerns about its ability to reverse the downward trajectory in the near term. With total revenues falling by 4.0% to $1,179.5 million and a net loss of $83.9 million, investors are right to question the company's financial health and future prospects. - Operational Challenges

The operational efficiency of Bloin' Brands is in question, as evidenced by the 36% drop in operating income from $120.6 million to $77.1 million. The company's operating margin has contracted significantly, falling from 9.7% to 6.4%. These numbers reflect deeper issues in the business model, including the ability to manage costs effectively. With restaurant-level operating margins also in decline, from 17.9% to 16.0%, the company is facing a challenging environment to maintain profitability. - Market and Competition Risks

In an industry as competitive as casual dining, Bloomin' Brands is struggling to keep up. The market is saturated with alternatives such as quick-service restaurants, supermarkets, and meal kit services, all vying for the consumer's dollar. With consumer preferences shifting rapidly, Bloomin' Brands faces the risk of losing relevance if it cannot adapt quickly enough. Competitors may outpace the company by implementing more effective business strategies or by embracing technological advancements that enhance the dining experience. - Supply Chain and Cost Pressures

Bloomin' Brands' financial performance is being squeezed by external pressures, including rising commodity prices and a tight labor market. The company is particularly vulnerable due to its dependence on limited suppliers for key ingredients, which poses a risk of supply chain disruptions and increased costs. With average weekly unit volumes declining across most brands, the company must navigate these cost pressures without alienating customers through price hikes or compromising on food quality. - Regulatory and Environmental Concerns

The current regulatory landscape presents another layer of complexity for Bloomin' Brands. Increasing demands for sustainable practices and corporate citizenship could result in additional costs that the company is ill-prepared to absorb. Compliance with new tax laws, employment regulations, and environmental standards will require significant investment, potentially diverting resources away from core operational needs. These factors, combined with the potential for fines or legal action due to non-compliance, add to the bearish outlook for the company.

In conclusion, while Bloomin' Brands has enjoyed success in the past, the current financial and operational indicators suggest a challenging road ahead. With declining sales, operational inefficiencies, and a plethora of market risks, including intense competition, cost pressures, and regulatory hurdles, investors should approach the stock with caution. The company's ability to navigate these troubled waters remains to be seen, but for now, the bearish case for Bloin' Brands appears to be well-founded.

Comments ()