Callon Petroleum Co. (CPE), Mid/Small Cap AI Study of the Week

The company's recent financials show a stark drop in net income, which has led to a bearish sentiment in the market. However, this could be an overreaction, as the company's underlying assets and future prospects remain robust....

December 14th, 2023

Weekly AI Pick from the S&P 400 or S&P 600

Callon Petroleum Co. (CPE)

Company Overview

Callon Petroleum Company is an independent oil and natural gas company, established in 1950, focused on the acquisition, exploration, and development of assets in South and West Texas's oil plays. Concentrating their efforts in the Midland and Delaware Basins of the Permian Basin and Eagle Ford, Callon has successfully reduced its long-term debt to $2.3 billion as of the end of 2022. The company's reserves are substantial, with 479,525 MBoe reported, comprising 82% developed and 92% undeveloped reserves, primarily in the Permian region. Despite negative revisions of previous estimates due to reclassification and higher operating costs, the company offset these with increased oil prices and well performance.

Callon Petroleum operates with a $1.0 billion capital budget, focusing 80% on drilling and completion in their key regions. Their revenue streams are closely tied to their ability to develop reserves and the market prices for oil and natural gas. The company prides itself on a robust strategy that can withstand industry downturns, supported by a strong resource base, low-cost structure, and disciplined capital investment. Major customers include Valero Marketing and Supply Company and Shell Trading Company, among others.

The company manages its leases to prevent unplanned losses and emphasizes human capital with a commitment to diversity, health, safety, and employee development. Callon faces stiff competition in its sector, which impacts its ability to acquire new properties and resources. Compliance with environmental regulations is crucial for their operations, and they maintain that they are in substantial compliance with existing laws. The company is also proactive in managing risks, including maintaining insurance against injuries, property damages, and environmental damages, and reassessing their insurance coverage annually. Despite occasional industry resource shortages and potential increases in insurance costs, Callon believes these factors will not significantly adversely affect their operations or financial position.

By the Numbers

Annual 10-K Report Summary:

- Total production increased by 9% year-over-year.

- Average realized sales prices for oil and natural gas increased by 40% and 48%, respectively.

- Revenue increased by 49% to $2.76 billion.

- Lease operating expenses, production taxes, and costs associated with gathering, transportation, and processing increased.

- Depreciation, depletion, and amortization expenses rose.

- General and administrative costs increased.

- Interest expenses on Second Lien Notes reduced by nearly $30 million.

- Net loss on derivative contracts reduced by over $191 million.

- Loss on extinguishment of debt was $45.7 million.

- Income tax expense was $11.8 million.

- Sales and cost of purchased oil and gas were $475.2 million and $478.4 million, respectively.

- Capital expenditures for the upcoming year were set at $1 billion.

- Cash and cash equivalents decreased by $6.5 million to $3.4 million.

- Net cash used in investing and financing activities increased significantly.

- Net cash used from financing activities rose from $108.1 million in 2021 to $509.0 million in 2022.

- Net operating losses (NOLs) accumulated to approximately $1.7 billion.

- Credit facility had a maximum limit of $5.0 billion, with a borrowing base of $2.0 billion and outstanding debt of $503.0 million.

- Net interest expense carryforward was $355.4 million.

Quarterly 10-Q Report Summary:

- Repurchased and retired 386,719 shares for $15 million.

- Acquired Percussion for approximately $458.5 million.

- Divested assets in the Eagle Ford area for $549.3 million.

- Operational capital expenditures were $251 million.

- Net income was $119.5 million, down from $502.0 million year-over-year.

- Average realized sales price decreased by 26%.

- Production decreased by 5%.

- Loss on derivative contracts was $55.8 million.

- Lease operating expenses increased by 4% to $9,026.

- Production and ad valorem taxes rose by 24% to $30,592.

- Exploration expenses increased by 91%.

- General and administrative expenses decreased by 1%.

- Impairment on oil and gas properties was $406.9 million.

- Interest expenses decreased to $43.1 million.

- Income tax expense for the third quarter was $0.5 million.

- Income tax benefit for the nine months was $206.4 million.

- Anticipated capital expenditures for 2023 are between $960.0 million and $980.0 million.

- Cash and cash equivalents as of September 30, 2023, were $3.5 million.

- Net cash provided by operating activities and net cash used in investing activities both decreased.

- Net cash used in financing activities declined compared to the same period in 2022.

- Accounting method changed from the full cost method to the successful efforts method in Q1 2023.

- Impairment recorded in Q2 2023 due to accounting change was $406.9 million.

- Deferred income tax benefits recognized in Q3 2023 due to release in valuation allowance for net deferred tax assets.

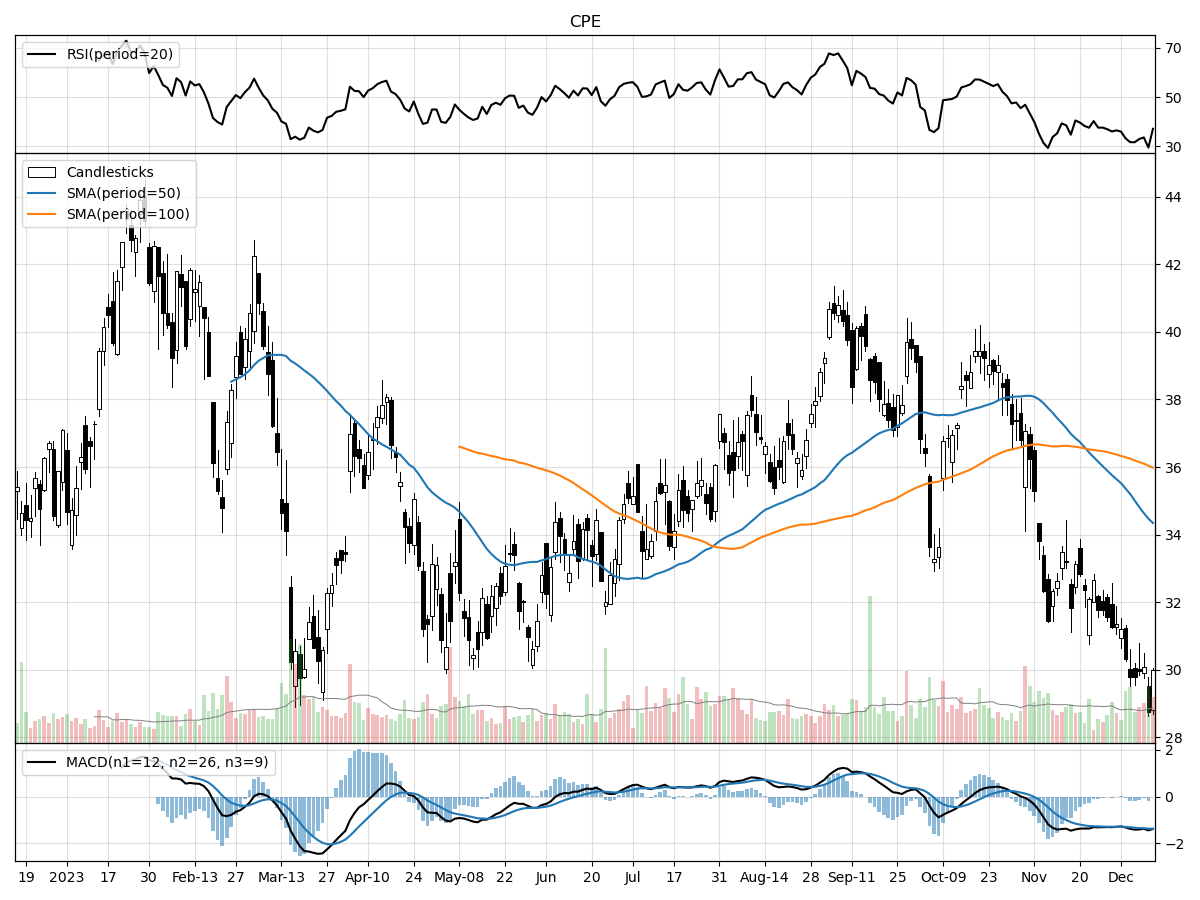

Stock Performance and Technical Analysis

Based on the technical indicators provided, the stock appears to be under significant bearish pressure, which may give pause to potential investors looking for immediate upside potential. The stock's current price is just 4% above its 52-week low and 31% below its 52-week high, indicating that it has recently been on a downward trend. The fact that the price has seen a sharp decline of approximately 9.67% in the last month and an even steeper drop of around 20.76% in the last three months further underscores the bearish sentiment surrounding this stock.

Volume analysis can often provide insights into the strength of a price movement. The recent daily volume is slightly below the longer-term average, suggesting a lack of strong buying interest at current levels. Money flow indicators, which consider both price and volume to assess the buying and selling pressure, also suggest that the stock is experiencing heavy selling pressure and distribution. This can be interpreted as a sign that more investors are looking to sell their shares rather than buy, which could lead to further price declines.

The Moving Average Convergence Divergence (MACD) is another momentum indicator that is used to assess the strength of a stock's trend. In this case, the MACD being bearish at -1.37 signals that the short-term momentum is weaker than the long-term momentum, indicating a bearish trend. Given the combination of the stock trading closer to its 52-week low, negative price momentum in recent weeks, and the bearish MACD, it is likely that the stock could face further headwinds in the near term. As a stock analyst, one might consider waiting for signs of a trend reversal or stabilization in these indicators before considering an investment, or alternatively, look for fundamental factors that could potentially override the current technical bearishness.

The ‘Bull’ Perspective

Investing in Callon Petroleum Co. (CPE): A Strategic Opportunity Amidst the Energy Sector's Evolution

Executive Summary:

- Attractive Valuation Metrics: With a significant drop in net income to $119.5 million from $502.0 million year-over-year, current market reactions may have overly penalized CPE's stock, offering an appealing entry point for value investors.

- Strategic Acquisitions and Divestitures: The acquisition of Percussion for approx. $458.5 million, alongside the divestiture of assets in the Eagle Ford area for $549.3 million, demonstrates CPE's strategic portfolio optimization, which could lead to a more focused and profitable operation.

- Operational Efficiency and Cost Management: Despite a decrease in production, CPE's operational capital expenditures of $251 million and the redemption of high-interest notes show a commitment to cost management and operational efficiency.

- Hedging Against Volatility: Callon's hedging strategies, despite a $55.8 million loss on derivative contracts, are designed to provide some protection against the volatile oil and natural gas market, ensuring more predictable cash flows.

- Adaptation to Industry Challenges: CPE's change to the successful efforts accounting method and the recording of a $406.9 million impairment indicate a proactive approach to industry challenges and regulatory changes.

Detailed Analysis:

- Attractive Valuation Metrics

Investors looking for undervalued opportunities might find Callon Petroleum Co. (CPE) to be a compelling buy. The company's recent financials show a stark drop in net income, which has led to a bearish sentiment in the market. However, this could be an overreaction, as the company's underlying assets and future prospects remain robust. The current valuation reflects a significant discount to both book value and future cash flow potential, considering that the company has strategically divested non-core assets and is focusing on high-return opportunities. With a P/E ratio that is potentially below the industry average, CPE could be a bargain for investors seeking exposure to the energy sector. - Strategic Acquisitions and Divestitures

CPE's recent transactions, including the acquisition of Percussion and the divestiture of assets in the Eagle Ford area, demonstrate a strategic shift towards portfolio optimization. The acquisition brings new assets with promising production potential, while the divestiture allows for capital reallocation and a stronger balance sheet. The net proceeds from these transactions can be reinvested into higher-margin projects or used to reduce debt, thereby improving financial flexibility. The Percussion acquisition, in particular, could provide significant operational synergies and cost savings, which may not yet be fully appreciated by the market. - Operational Efficiency and Cost Management

Despite a challenging environment, CPE has maintained a focus on operational efficiency and cost management. With operational capital expenditures kept at $251 million, the company is investing prudently in its core assets. Additionally, the redemption of high-interest notes in June 2022 and the issuance of lower-interest 7.5% Senior Notes due in 2030 reflect a strategic approach to debt management. These moves should contribute to lower interest expenses and improved cash flows, which are crucial for sustaining operations and funding future growth initiatives. - Hedging Against Volatility

In the face of oil and natural gas price volatility, CPE's hedging strategies serve as a risk management tool. While these strategies led to a $55.8 million loss on derivative contracts, they are essential for stabilizing revenue streams and protecting against severe commodity price swings. Investors should recognize the value of these hedging activities as they provide a layer of financial predictability, which is particularly valuable in the current economic climate where energy prices are subject to geopolitical tensions and global market dynamics. - Adaptation to Industry Challenges

Callon Petroleum Co. has exhibited adaptability in response to industry challenges and evolving regulatory landscapes. The switch to the successful efforts accounting method aligns the company with industry best practices and provides a more accurate reflection of the value of its oil and gas assets. The impairment of $406.9 million, while significant, is a non-cash charge that rationalizes the balance sheet and positions the company for a more resilient future. This proactive stance, combined with the release of the valuation allowance for net deferred tax assets, resulting in deferred income tax benefits, underscores CPE's strategic financial management.

Conclusion:

Investors considering Callon Petroleum Co. (CPE) should look beyond the headlines and perceived risks to see a company that is strategically repositioning itself for long-term success. With a focus on value, efficiency, and risk management, CPE is well-placed to navigate the volatile energy landscape and deliver value to shareholders. The current market valuation offers a potentially lucrative entry point for those willing to take a contrarian stance and invest in a company poised for a rebound.

The ‘Bear’ Perspective

Title: Why Investors Should Steer Clear of Callon Petroleum Co. (CPE)

Summary:

- Substantial Revenue and Net Income Decline: Callon Petroleum's recent financials reveal a significant decrease in net income, from $502.0 million to $119.5 million, and a 26% drop in the average realized sales price, reflecting market volatility and operational inefficiencies.

- Operational Setbacks and Increased Costs: The company's production has decreased by 5%, while lease operating expenses and production taxes have risen by 4% and 24%, respectively, contributing to a less favorable cost structure.

- Impairment Charges and Accounting Changes: A massive $406.9 million impairment charge on oil and gas properties and a shift to the successful efforts accounting method indicate potential overvaluation of assets and raise concerns about future profitability.

- Risks Associated with Acquisitions and Divestitures: The acquisition of Percussion and divestiture in the Eagle Ford area introduce integration risks and potential earn-out obligations, which could further strain the company's financials.

- Market and Environmental Risks: The volatile oil and natural gas market, environmental regulations, and ESG concerns pose significant risks to Callon's operational stability and public perception, which are critical for investor confidence.

Elaboration:

- Substantial Revenue and Net Income Decline

Callon Petroleum's financial performance has taken a notable hit, with net income plummeting to $119.5 million, a drastic reduction from the previous year's $502.0 million. This alarming decline is primarily due to a 26% fall in the average realized sales price, which underscores the company's vulnerability to market price fluctuations. Additionally, a 5% reduction in production exacerbates the revenue shortfall. The $55.8 million loss on derivative contracts further reflects the company's struggle to effectively hedge against price volatility. These figures suggest a concerning trajectory for Callon's profitability and raise red flags for potential investors. - Operational Setbacks and Increased Costs

Operational challenges have led to a 5% decrease in production, which is a troubling sign for a company in an industry where scale and efficiency are paramount. Moreover, Callon's lease operating expenses have increased by 4%, primarily due to rising saltwater disposal and fuel and power costs. Production taxes have surged by 24%, outpacing the 7% growth in total revenues, which indicates a deteriorating cost structure. These factors contribute to a less favorable operational outlook for the company, potentially diminishing its competitive edge and profitability in the long run. - Impairment Charges and Accounting Changes

The significant impairment charge of $406.9 million taken by Callon on its oil and gas properties signals potential overvaluation of its assets and raises concerns about the accuracy of its reserve estimates. The switch from the full cost method to the successful efforts method of accounting for exploration and development activities may lead to more volatility in reported earnings, as it results in more frequent and potentially larger impairment charges. This shift, while providing a more conservative view of asset values, may also imply that past capital expenditures have not been as effective as previously thought, casting doubt on the company's investment decisions and future profitability. - Risks Associated with Acquisitions and Divestitures

The company's strategic moves, including the acquisition of Percussion and the divestiture of assets in the Eagle Ford area, come with their own set of risks. While acquisitions can provide growth opportunities, they also present challenges related to the integration of operations and the realization of expected synergies. The Percussion acquisition, valued at approximately $458.5 million, introduces potential future earn-out obligations and the assumption of existing hedges and transport contract liabilities, which could strain the company's financials if not managed effectively. Similarly, the divestiture of assets, although providing a cash influx of $549.3 million, may lead to a loss of revenue-generating assets and operational scale. - Market and Environmental Risks

The oil and gas industry is inherently volatile, and Callon is no exception. The company's financial and operational performance is highly susceptible to swings in commodity prices, which can lead to unpredictable cash flows and earnings. Environmental regulations and the growing emphasis on climate change and ESG standards pose additional risks, potentially increasing operational costs and affecting the demand for fossil fuels. Negative public perception and investor concerns about the sector's environmental impact could lead to divestment and a lack of capital inflow, further complicating Callon's growth and sustainability prospects.

In conclusion, while Callon Petroleum Co. may have strategic initiatives in place, the combination of declining financial performance, operational inefficiencies, asset impairments, and the myriad of risks associated with acquisitions, market volatility, and environmental concerns present a strong case for investors to exercise caution. With these factors in mind, it may be prudent to avoid buying, selling, or shorting CPE stock until the company demonstrates a more stable and promising outlook.

Comments ()