Capri Holdings Ltd. (CPRI), Mid/Small Cap AI Study of the Week

February 27, 2024

Weekly AI Pick from the S&P 400 or S&P 600

Company Overview

Capri Holdings Limited is a renowned global fashion conglomerate that manages three luxury brands: Versace, Jimmy Choo, and Michael Kors. Each brand is recognized for its distinctive luxury and style, with Versace known for Italian fashion, Jimmy Choo for high-end shoes and accessories, and Michael Kors for its luxury sportswear and fashion collections. The company operates globally with a significant presence in the Americas, EMEA, and Asia, generating revenue through retail, wholesale, and licensing channels. Despite the pandemic's impact, the luxury market is projected to grow, with e-commerce, the Chinese market, and younger consumers driving this trend.

For the fiscal year ending April 1, 2023, Capri Holdings reported revenues of $5,619 million. The company is focusing on expanding its accessories line for Versace and Jimmy Choo, aiming for these to make up 50% and 30% of their revenues respectively. With hundreds of stores worldwide for each brand and a robust e-commerce presence, the company is also looking to enhance its wholesale operations. Capri Holdings is strategizing to grow Versace to $2 billion in revenue by increasing its retail footprint and e-commerce, while Jimmy Choo is targeted to reach $1 billion in revenue through product expansion and global retail growth. Michael Kors is positioned as the foundation of the group, with plans to grow its men's line and double its revenue in Asia.

Revenue is primarily derived from accessories, footwear, and apparel, with a smaller portion from licensed products and other sources. Capri Holdings invests significantly in marketing, spending $374 million in fiscal 2023, and places a strong emphasis on e-commerce for future growth. The company relies on independent third-party contractors for manufacturing, predominantly in Italy and Asia, and is aiming to centralize production to create efficiencies.

Capri Holdings is also focusing on technology and human capital investment. They resumed their major ERP system project in Fiscal 2021, and employee initiatives are in place to promote learning, diversity, and inclusion. The company is committed to workplace safety, adapting health practices due to COVID-19, and engages with employees for feedback to maintain a positive work environment.

By the Numbers

Annual 10-K Report Summary for Fiscal 2023:

- Total revenue: $5.619 billion (decrease of $35 million or 0.6% from $5.654 billion in Fiscal 2022)

- Revenue by segment: Versace $1.106 billion, Jimmy Choo $633 million, Michael Kors $3.880 billion

- Income from operations: $679 million (decline from $903 million in Fiscal 2022)

- Income from operations by segment: Versace $152 million, Jimmy Choo $38 million, Michael Kors $868 million

- Corporate expenses, asset impairment, and other charges: Not specified

- Reserves for estimated returns and allowances: $73 million (up from $70 million in FY2022)

- Increase in raw materials and work-in-process inventory: From $31 million in FY2022 to $47 million in FY2023

- Impairment charges: $158 million in FY2021, $83 million in FY2022, $36 million in FY2023

- Goodwill and intangible assets impairment: Jimmy Choo $82 million for goodwill and $24 million for intangible assets in FY2023

- Net income: $619 million (decrease of 24.8% from the previous year)

- Net income attributable to Capri: $616 million

Quarterly 10-Q Report Summary for Q3 Fiscal 2024:

- Total revenue for Q3: $1.427 billion (decrease of 5.6% from $1.512 billion in the same quarter of the previous year)

- Revenue decrease on a constant currency basis for Q3: 6.6%

- Revenue by segment for Q3: Versace down 8.8%, Jimmy Choo down 1.2%, Michael Kors down 5.6%

- Gross profit for Q3: $928 million (decrease of 7.7%)

- Gross profit margin for Q3: Contracted from 66.5% to 65.0%

- Operating expenses for Q3: Rose by 4.8% to $806 million

- Income from operations for Q3: $122 million (decrease of 48.3%)

- Operating income by segment for Q3: Versace $14 million loss, Jimmy Choo $4 million, Michael Kors $219 million

- Interest expenses for Q3: Decreased by $11 million

- Provision for income taxes for Q3: Increased to $18 million (from $3 million)

Nine-Month Period Ending December 2023:

- Total revenue for nine months: $3.947 billion (decrease of 7.9%)

- Gross profit for nine months: $2.572 billion (decrease of 10%)

- Net income for nine months: $243 million (decrease of 62.6%)

- Income from operations for nine months: $302 million (down from $719 million)

- Asset impairment charges: Higher, mainly related to Versace and Michael Kors store locations

- Cash and cash equivalents: $249 million

These figures highlight the financial challenges faced by Capri Holdings, including declining revenues, shrinking profit margins, and increased operating expenses, amidst a difficult global economic environment.

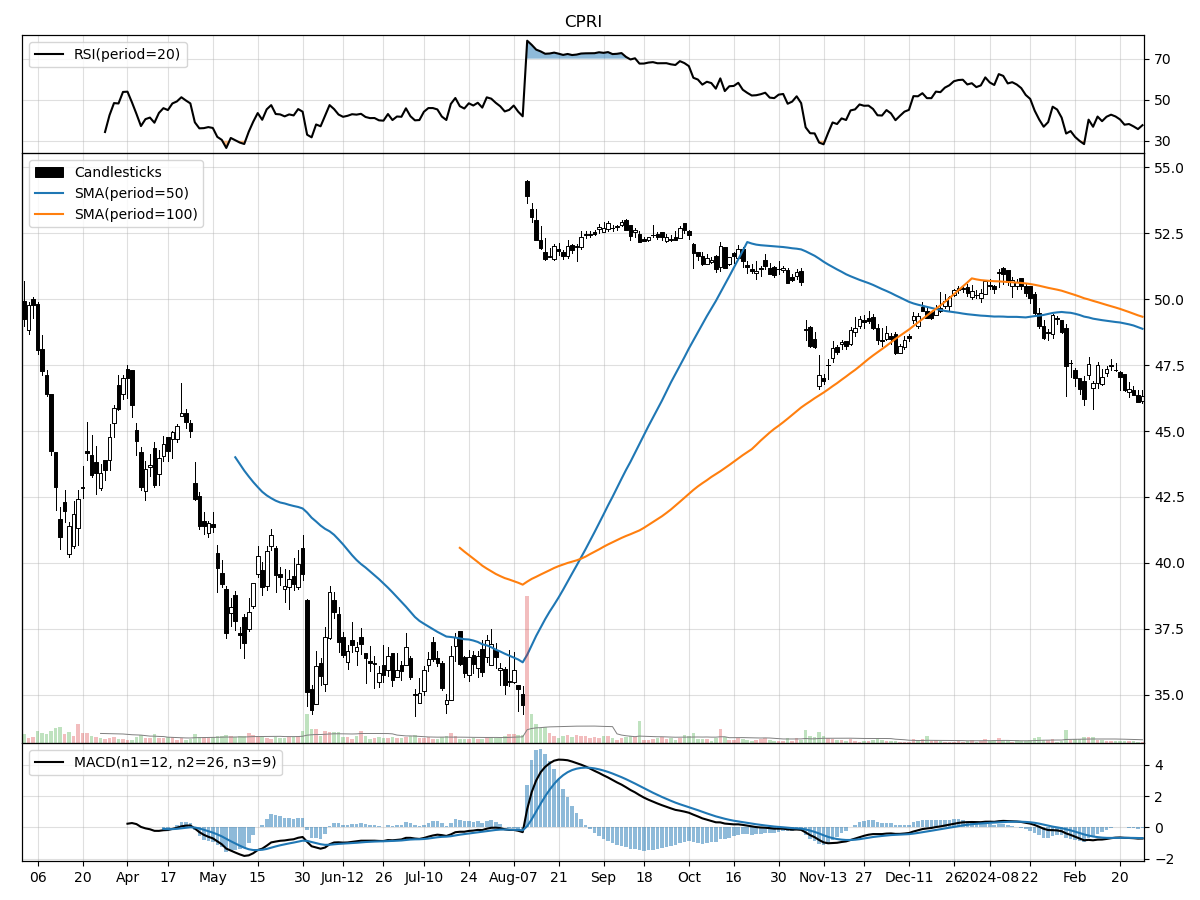

Stock Performance and Technical Analysis

The technical analysis of the stock in question reveals a mixed picture of its performance and potential direction. The current stock price is positioned notably above its 52-week low, by 34 percent, which may indicate that the stock has seen considerable appreciation over the past year and could be in a generally upward trend or in a period of consolidation after a run-up. However, it's also 14 percent below its 52-week high, suggesting that the stock has retracted from its peak, potentially offering a discounted entry point if the fundamental outlook remains strong.

The recent daily trading volume is below the longer-term average, which could signify a decrease in trader interest or confidence in the near term. This diminished volume could lead to higher volatility or indicate a period of accumulation or distribution before a more significant price move. The price decline of approximately 5.95% in the last month, alongside a relatively stable price over the last three months, suggests that the stock might be experiencing a short-term bearish trend within a longer-term sideways market.

Money Flow indicators are pointing to moderate selling pressure and distribution, which means that there is more selling than buying, potentially indicating that investors are taking profits or reducing their positions. This could foreshadow a continuation of the downward trend in the short term. The MACD (Moving Average Convergence Divergence) being bearish, with a value of -0.69, further confirms this sentiment, indicating that the short-term momentum is currently in favor of the bears, and the stock might continue to face downward pressure in the near term.

Overall, the technicals suggest that caution is warranted for potential investors. The stock is not in a clear uptrend, and the recent bearish signals may imply that it is not the optimal time to enter a long position. However, for a contrarian investor or one with a longer time horizon, this could be an opportunity to watch the stock closely for signs of a trend reversal, especially if the fundamental outlook of the company remains positive.

The ‘Bull’ Perspective

Title: Capri Holdings Ltd: A Resilient Luxury Contender in a Volatile Market

Upfront Summary:

- Robust Brand Portfolio: Capri Holdings Ltd's ownership of iconic luxury brands Versace, Jimmy Choo, and Michael Kors positions it favorably in the high-margin luxury market, with a diversified brand appeal that spans various consumer segments.

- E-Commerce Expansion: The company's investment in a new e-commerce platform, despite initial setbacks, signals a commitment to digital growth, a critical avenue for reaching modern consumers and driving future revenue streams.

- Global Footprint: With 47% of its revenue derived from international markets, Capri Holdings has a strong global presence that, while exposing it to currency risks, also allows for diversified revenue sources and growth opportunities outside the saturated US market.

- Strategic Cost Management: In the face of inflation and supply chain challenges, Capri's proactive measures in sourcing efficiencies and production diversification are essential to maintaining profitability.

- Attractive Valuation: Given the recent decline in stock price, Capri Holdings presents an attractive valuation for investors, with the potential for significant upside as market conditions stabilize and strategic initiatives bear fruit.

Elaboration on Points:

- Robust Brand Portfolio

Capri Holdings Ltd's strategic ownership of Versace, Jimmy Choo, and Michael Kors offers a compelling investment thesis. These brands cater to different luxury segments, from high-end couture to premium accessories, which helps mitigate risks associated with changing fashion trends and consumer preferences. Despite a challenging quarter that saw a contraction in revenues and profits, the inherent value of these brands remains. Versace's revenue, for instance, while down 8.8%, is part of a long-term story of brand revitalization and market expansion. The luxury sector often boasts higher margins than mass-market apparel, and Capri's gross profit margin, despite a slight decrease, remains robust at 65.0%. This diversified brand portfolio is a critical asset that can drive long-term shareholder value. - E-Commerce Expansion

Capri Holdings is doubling down on its digital transformation with a significant investment in a new e-commerce platform. Though the rollout has encountered challenges, leading to operational impacts, the move is a critical step towards capturing the growing luxury online retail market. E-commerce offers higher margins than traditional retail due to lower overhead costs and the potential for direct customer engagement and data collection. As the platform's teething issues are resolved and the rollout continues into fiscal 2025, we can anticipate a strong rebound in this segment, tapping into the vast potential of digital sales channels. - Global Footprint

Capri's expansive international presence is a double-edged sword, but one that ultimately offers more opportunities than risks. While the company faces exposure to currency fluctuations and diverse market risks, its global footprint allows for revenue diversification, which is crucial in times of localized economic downturns. The 47% international revenue stream is a testament to the global appeal of Capri's brands, and as economies in Europe and Asia recover from pandemic-induced slumps, Capri is well-positioned to capitalize on renewed luxury spending. - Strategic Cost Management

Inflation and supply chain disruptions have been a thorn in the side of many retailers, but Capri Holdings has been proactive in its approach to cost management. By diversifying production locations and improving sourcing efficiencies, the company is working to mitigate the impact of cost increases. While operating expenses have risen, these strategic initiatives are essential for maintaining a competitive edge in pricing and preserving margins in the long term. - Attractive Valuation

Capri Holdings' stock price has seen a decline in the face of its recent financial performance and broader market conditions. However, this presents an attractive entry point for investors. The company's Price-to-Earnings (P/E) ratio and other valuation metrics are likely to be more favorable compared to historical averages, providing a potential opportunity for investors to buy into a luxury brand conglomerate at a discount. As the market stabilizes and Capri's strategic initiatives, such as its e-commerce rollout and cost management efforts, begin to show results, there is a significant upside for early investors.

In conclusion, while Capri Holdings Ltd faces headwinds like any company in today's complex global market, its strong brand portfolio, strategic focus on e-commerce, global market penetration, proactive cost management, and current valuation present a compelling case for investment. The luxury market is notoriously resilient, and Capri's positioning within it offers a potentially lucrative opportunity for investors willing to look beyond short-term volatility.

The ‘Bear’ Perspective

Why Investors Should Steer Clear of Capri Holdings Ltd.

Capri Holdings Ltd. (CPRI) presents several red flags that warrant caution from potential investors. Here's a concise breakdown of the key reasons to avoid buying, holding, or shorting CPRI stock:

- Declining Financial Performance: Recent financial reports show a concerning trend, with total revenue and net income significantly down from the previous year.

- Market Concentration Risks: With nearly half of CPRI's revenue generated from volatile international markets, geopolitical and economic risks are amplified.

- Operational and Strategic Vulnerabilities: CPRI's reliance on a limited number of distribution facilities and the risks associated with ongoing ERP implementation could lead to operational disruptions.

- Competitive and Industry Challenges: The luxury fashion industry is notoriously fickle, and CPRI faces stiff competition and the constant need for innovation to maintain brand relevance.

- Currency and Cost Volatility: Fluctuations in foreign currency exchange rates and raw material costs present additional financial risks that could squeeze margins further.

In-depth Analysis:

- Declining Financial Performance:

Capri Holdings Ltd.'s recent financial performance raises significant concerns. The company's total revenue has decreased by 5.6% year-over-year to $1.427 billion, with a more pronounced decline on a constant currency basis at 6.6%. The gross profit margin has contracted, and income from operations has plummeted by a staggering 48.3% to $122 million. Over a nine-month period, net income has seen a precipitous drop of 62.6% to $243 million. These numbers suggest that CPRI is struggling to maintain profitability and growth, which is a red flag for investors looking for stable or expanding financial health in their portfolio companies. - Market Concentration Risks:

Capri Holdings Ltd. is heavily reliant on international markets, with 47% of its revenue stemming from outside the United States. This exposes the company to a multitude of risks, such as political unrest, economic instability, and regulatory changes in foreign jurisdictions. The luxury market is particularly sensitive to such external factors, which can lead to swift and unpredictable shifts in consumer spending. The recent geopolitical tensions and the potential for a global recession further exacerbate these risks, making CPRI's international exposure a liability rather than an asset. - Operational and Strategic Vulnerabilities:

The company's operational infrastructure is another area of concern. CPRI's dependence on a limited number of distribution facilities means that any disruptions, whether from natural disasters, labor disputes, or other unforeseen events, could have a disproportionate impact on its ability to deliver products. Additionally, the ongoing implementation of a new enterprise resource planning (ERP) system introduces the risk of technical glitches and delays, which could disrupt operations and lead to financial losses. These factors contribute to a precarious operational situation that could undermine CPRI's strategic efforts and financial stability. - Competitive and Industry Challenges:

The fashion industry is in a constant state of flux, requiring brands to continually innovate and adapt to changing consumer tastes. CPRI's brands—Versace, Jimmy Choo, and Michael Kors—are not immune to these pressures. With a decline in revenues across all brands, it's clear that CPRI is facing difficulties in maintaining its market position against fierce competition. The company's ability to stay relevant and desirable in the luxury market is critical to its success, and any missteps in trend forecasting or brand management could lead to further declines in sales and profitability. - Currency and Cost Volatility:

Capri Holdings Ltd. is subject to the whims of foreign currency exchange rates and raw material cost volatility. A stronger U.S. dollar can adversely affect the company's translated earnings from international markets and may force price adjustments that could eat into profit margins. Additionally, fluctuations in the cost of raw materials used in the production of luxury goods can lead to increased production costs, putting further pressure on the company's profitability. These financial risks are difficult to predict and manage, adding another layer of uncertainty for investors.

Conclusion:

In light of these points, it's clear that Capri Holdings Ltd. faces a multitude of challenges that could negatively impact its stock performance. From declining financial metrics and market concentration risks to operational vulnerabilities, competitive pressures, and cost volatilities, CPRI presents a high-risk investment profile. Prudent investors should consider these factors carefully and perhaps look for more stable and less risk-laden opportunities in the current market environment.

Comments ()