Corcept Therapeutics (CORT), Mid/Small Cap AI Study of the Week

Corcept Therapeutics Inc. is a pharmaceutical company focused on the development of drugs that modulate the effects of cortisol. Their key product, Korlym, has been on the market since 2012 for the treatment of Cushing's syndrome.

February 8, 2024

Weekly AI Pick from the S&P 400 or S&P 600

Company Overview

Corcept Therapeutics Inc. is a pharmaceutical company focused on the development of drugs that modulate the effects of cortisol. Their key product, Korlym, has been on the market since 2012 for the treatment of Cushing's syndrome. The company is also advancing a robust pipeline of over 1,000 proprietary cortisol modulators, with relacorilant as a leading candidate currently in Phase 3 trials for the same condition, but with reduced side effects compared to Korlym. Despite setbacks due to the COVID-19 pandemic, Corcept continues clinical trials for life-threatening conditions and has received orphan drug status for relacorilant in the treatment of Cushing's syndrome from both the FDA and the European Commission, which could secure exclusive marketing rights upon approval.

In addition to its work on Cushing's syndrome, Corcept is exploring the application of relacorilant in treating advanced ovarian cancer, with promising results in improved survival rates leading to a Phase 3 trial. The company is also investigating the potential for relacorilant in adrenal and prostate cancer treatments. Other research includes the development of a diagnostic assay for hypercortisolism and the investigation of dazucorilant for ALS. After discontinuing miricorilant for NASH due to adverse effects, Corcept plans to redirect its focus on treating antipsychotic-induced weight gain with a Phase 2 trial slated for late 2023.

Corcept's commitment to innovation is evident from their significant investment in R&D, with expenses ranging from $113.9 to $131.0 million over the past three years. Their intellectual property portfolio includes patented compounds with potential to treat a variety of conditions, with patents extending to 2039. The company faces competition and regulatory challenges, actively defending its patents while navigating extensive FDA requirements for drug approval and post-marketing regulations. Additionally, Corcept operates under a complex healthcare regulatory environment influenced by recent reforms such as the ACA and IRA, with laws like the Anti-Kickback Statute and the False Claims Act imposing strict compliance requirements and severe penalties for violations, which could impact the company's business and financial outcomes.

By the Numbers

Annual 10-K Report Summary:

- Net product revenue: $401.9 million in 2022 (up from $366.0 million in 2021 and $353.9 million in 2020)

- Cost of sales: 1.3% of revenue in 2022

- Research and development expenses: $131.0 million in 2022 (increase from previous years)

- Selling, general, and administrative expenses: $152.8 million in 2022 (up from $122.4 million in 2021)

- Interest and other income: $3.6 million in 2022 (up from $0.5 million in 2021)

- Income tax expenses: $14.8 million in 2022 (up from $12.5 million in 2021)

- Cash, cash equivalents, and marketable securities: $436.6 million as of December 31, 2022

Quarterly 10-Q Report Summary:

- Increase in net product revenue in Q3 and first nine months of 2023 compared to 2022 (specific numbers not provided)

- Research and development expenses: $45.5 million for Q3 and $129.6 million for the first nine months of 2023

- Selling, general, and administrative expenses: Increased in 2023 (specific numbers not provided)

- Interest and other income: Increased in 2023 due to higher market interest rates (specific numbers not provided)

- Income tax expense: Increased for the first nine months of 2023 (specific numbers not provided)

- Cash, cash equivalents, and marketable securities: $414.8 million as of September 30, 2023

- Operating cash flow: $121.2 million for the first nine months of 2023

- Investing cash flow: $73.8 million for the first nine months of 2023

- Financing cash flow: Use of $149.5 million for the first nine months of 2023

- Retained earnings: $371.2 million as of the first nine months of 2023

Please note that the specific numbers for the increase in net product revenue, as well as the exact amounts for selling, general, and administrative expenses, interest and other income, and income tax expense for the quarterly report were not provided in the summary.

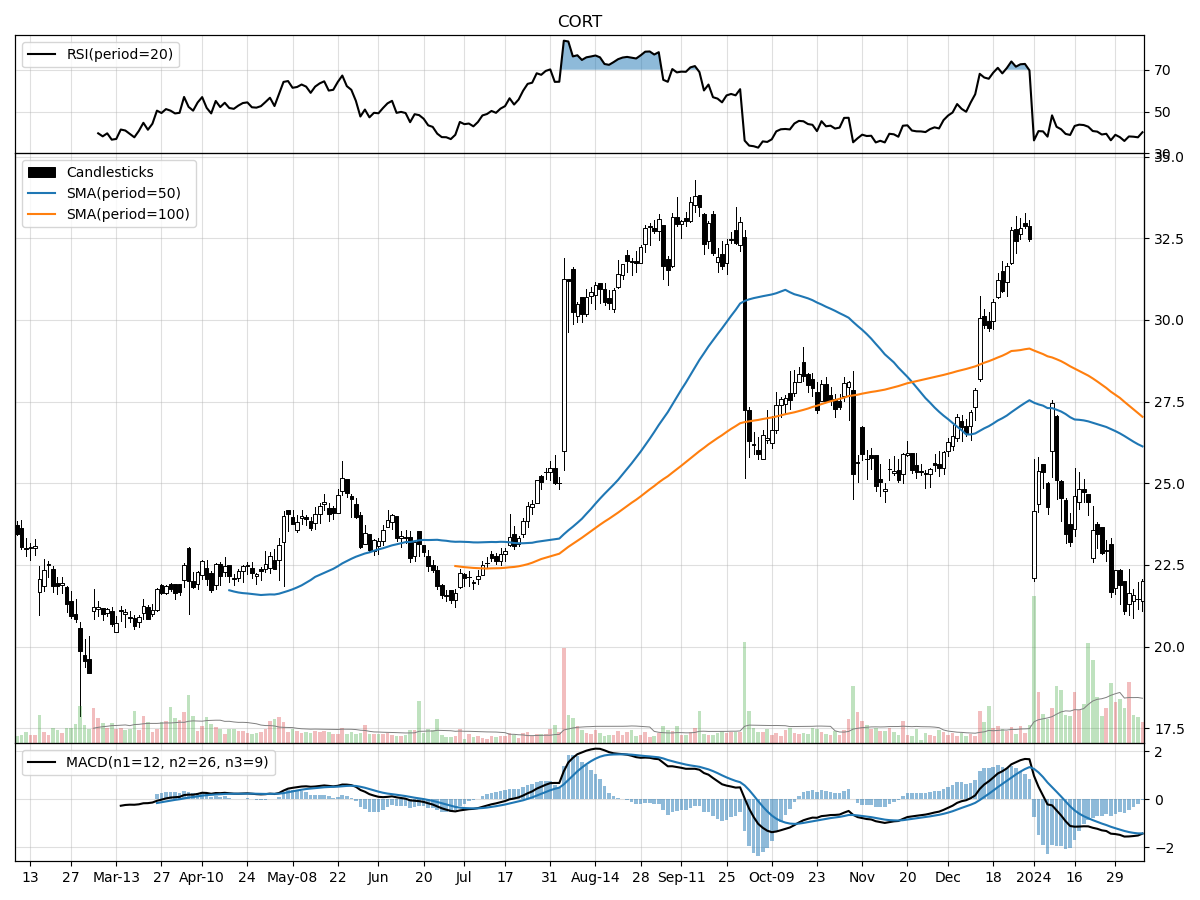

Stock Performance and Technical Analysis

The technical analysis of a stock involves studying past market data, primarily through charts, to forecast future price movements. The current technicals for the stock in question present a mixed outlook, with the stock trading at $22.02, which is 14 percent above its 52-week low, indicating some level of support or possible accumulation at lower levels. However, it's also 34 percent below its 52-week high, suggesting that the stock has undergone a significant retracement from its peak and may be in a longer-term downtrend or correction phase.

The recent trading volume is substantially higher than the longer-term average, with daily volume at 2,253,856.25 shares compared to an average of 899,892.56 shares. This increased volume, particularly if associated with price declines, could point to a heightened level of distribution, where larger players may be exiting their positions, thus exerting downward pressure on the stock price. This interpretation is corroborated by the Money Flow indicators, which suggest the stock is under heavy selling pressure and distribution. Such conditions often indicate a bearish sentiment among investors.

The Moving Average Convergence Divergence (MACD) is a trend-following momentum indicator that shows the relationship between two moving averages of a stock’s price. The MACD being bearish at -1.42 indicates that the short-term momentum is declining at a faster rate than the long-term momentum, suggesting that the downward trend is likely to continue in the near term. The price declines of 12.27% in the last month and 11.60% in the last three months further support the notion of a bearish trend. Investors should approach with caution, considering additional analysis and possibly looking for confirmatory signals before deciding on an investment, as the current technicals suggest that the bearish momentum may persist.

The ‘Bull’ Perspective

Investing in Corcept Therapeutics Inc. (CORT): A Strategic Opportunity in Biopharmaceuticals

Upfront Summary:

- Robust Financial Performance: Corcept has demonstrated consistent revenue growth, with a notable increase in net product revenue in recent quarters, showcasing the company's financial health and market demand for its products.

- Pipeline Progression and Diversification: The company's promising pipeline, especially with relacorilant in Phase 3 trials, positions CORT for potential market expansion and diversification beyond its flagship product, Korlym.

- Strategic Positioning Amidst Market Dynamics: Despite the broader market's volatility and the looming risks of the healthcare sector, CORT's strategic positioning and proactive management of risks present a compelling investment case.

- Strong Cash Position and Financial Prudence: With a solid cash reserve and prudent financial management, CORT is well-equipped to navigate through R&D investments and market uncertainties without the immediate need for additional financing.

- Potential for Long-Term Growth: Given the company's focused R&D efforts, strong intellectual property portfolio, and the growing need for effective treatments in endocrine disorders, CORT holds significant potential for long-term growth.

Elaboration on Key Points:

- Robust Financial Performance:

Corcept has been on a financial uptrend, with its net product revenue experiencing a substantial uptick in the recent quarters of 2023. This growth is not just a number; it reflects the increasing market penetration and acceptance of Korlym, as well as the potential for its pipeline products. The company's financial resilience is further underscored by its ability to implement strategic price increases, which have contributed positively to the revenue stream despite the challenges imposed by new healthcare legislation. This financial fortitude, particularly in the face of the Inflation Reduction Act of 2022, demonstrates Corcept's agility in navigating market headwinds while maintaining profitability. - Pipeline Progression and Diversification:

Investors should pay close attention to Corcept's pipeline, particularly relacorilant, which is advancing through Phase 3 trials with promising results. The drug's orphan drug designation is a significant milestone, potentially offering regulatory benefits and market exclusivity upon approval. Moreover, the diversification into oncology, with positive signals from Phase 2 trials in ovarian cancer, suggests a broader horizon for the company's market presence. The pipeline's progression is not just about numbers of compounds; it's about the strategic expansion of Corcept's therapeutic reach, which could translate into substantial revenue streams in the future. - Strategic Positioning Amidst Market Dynamics:

The current market dynamics, characterized by volatility and economic uncertainties, present a complex backdrop for biopharmaceutical investments. However, Corcept's strategic positioning, with a focus on serious endocrine disorders—a niche yet essential medical need—provides a degree of insulation against broader market swings. The company's awareness and proactive management of risks, such as potential generic competition and legal challenges related to mifepristone, indicate a forward-thinking approach that is crucial for investor confidence. - Strong Cash Position and Financial Prudence:

Corcept's cash reserves of $414.8 million as of September 30, 2023, speak volumes about the company's financial prudence. This strong cash position ensures that Corcept can sustain its R&D endeavors and navigate market fluctuations without the pressing need for external financing. The company's disciplined approach to cash flow management, as evidenced by the operating, investing, and financing activities, positions it well to capitalize on strategic opportunities and mitigate financial risks. - Potential for Long-Term Growth:

The long-term growth prospects of Corcept are underpinned by the company's dedicated R&D efforts and a robust portfolio of intellectual property. With a growing global incidence of endocrine disorders and the unmet medical needs within this domain, Corcept's focus on developing innovative treatments holds the promise of addressing these challenges. The potential market for relacorilant and other pipeline products, coupled with the company's commitment to expanding its therapeutic footprint, suggests a trajectory of long-term value creation for shareholders.

Conclusion:

In summary, Corcept Therapeutics Inc. presents a compelling investment case with its robust financial performance, diversified and progressing pipeline, strategic market positioning, strong cash reserves, and the potential for long-term growth. While there are risks inherent in the biopharmaceutical industry, Corcept's strategic management of these challenges and its focus on delivering innovative treatments make it a noteworthy contender for investors seeking opportunities in the healthcare sector.

The ‘Bear’ Perspective

Why Investors Should Exercise Caution with Corcept Therapeutics Inc. (CORT)

Upfront Summary:

- Revenue Concentration Risk: Corcept relies heavily on its flagship product, Korlym, with risks of generic competition and physician preference shifts.

- Regulatory and Development Hurdles: Ongoing R&D projects face uncertainties, including potential regulatory rejections and clinical trial setbacks.

- Legal and Compliance Risks: Legal challenges related to mifepristone and the risk of violating federal laws could lead to significant financial penalties.

- Supply Chain and Manufacturing Dependencies: Single-source third-party manufacturers and specialty pharmacies present a high risk for supply chain disruptions.

- Pandemic-Induced Uncertainties: COVID-19 continues to pose risks to clinical trial progress, regulatory timelines, and overall operational efficiency.

Elaboration on Points:

- Revenue Concentration Risk:

Corcept's financial health is largely dependent on sales of Korlym, which accounts for the majority of its revenue. While the recent increase in net product revenue is encouraging, the looming threat of generic competition could significantly undercut Corcept's market share and revenue. The possibility of physicians opting for alternative treatments also poses a threat to the company's top-line growth. With a single product driving the bulk of its revenue, any negative shift in market dynamics or competitive landscape could have a disproportionate impact on Corcept's financial performance. - Regulatory and Development Hurdles:

Research and development in the pharmaceutical industry are fraught with uncertainty. Corcept's future growth is contingent upon the successful development and regulatory approval of its pipeline products. The company's increased R&D expenses, which have risen to $45.5 million and $129.6 million for the three and nine months ended September 30, 2023, respectively, reflect its commitment to advancing these projects. However, the inherent risk of regulatory rejections, undesirable side effects, and clinical trial delays or failures cannot be overstated. The failure of any key clinical trial could lead to sunk costs and a negative impact on the company's valuation. - Legal and Compliance Risks:

Corcept is navigating a complex legal landscape, particularly concerning mifepristone's association with abortion. Public perception and legal challenges could restrict Korlym's marketability. Moreover, potential violations of federal laws such as the Anti-Kickback Statute and False Claims Act could result in severe financial penalties. The subpoena from the NJ USAO, even though Corcept is not currently a defendant, indicates that legal risks are present and could lead to unforeseen liabilities. - Supply Chain and Manufacturing Dependencies:

The company's reliance on single third-party manufacturers and specialty pharmacies for Korlym introduces significant supply chain risks. Contracts set to expire in 2023 and 2024 could lead to renegotiations under less favorable terms or disruptions in supply. Any interruption in the manufacturing or distribution of Korlym would directly affect Corcept's ability to generate revenue and meet market demand, potentially leading to a decline in investor confidence and a corresponding drop in stock price. - Pandemic-Induced Uncertainties:

The COVID-19 pandemic has already caused disruptions in Corcept's clinical trials and could continue to impact the company's operations. The risks of further enrollment challenges, regulatory delays, supply chain issues, and increased costs cannot be ignored. The pandemic's unpredictable nature adds another layer of risk to Corcept's already uncertain R&D efforts. Market volatility in response to pandemic developments could also lead to erratic stock price movements, making CORT a potentially unstable investment in the short term.

In conclusion, while Corcept Therapeutics Inc. has shown some promising developments, the combination of revenue concentration, regulatory challenges, legal and compliance risks, supply chain dependencies, and pandemic-induced uncertainties create a high-risk environment for investors. Prudence dictates a cautious approach to investing in CORT, as any adverse developments in these areas could significantly impact the company's financial health and stock performance.

Comments ()