Devon Energy Corp. (DVN), Large Cap AI Study of the Week

January 23, 2024

Weekly AI Pick from the S&P 500

Company Overview

Devon Energy Corp. (DVN) is an independent energy company engaged in the exploration, development, and production of oil, natural gas, and natural gas liquids (NGLs), primarily operating within the United States. Following its merger with WPX Energy in January 2021, Devon has strengthened its position in the Delaware and Williston Basins, focusing on a cash-return business model. The company is committed to delivering competitive shareholder returns, achieving sustainable cash flow growth, and operating with strong environmental, social, and governance (ESG) values. Devon aims for net-zero greenhouse gas (GHG) emissions for Scope 1 and 2, invests in emissions reduction, and emphasizes water conservation.

Devon's workplace culture prioritizes safety, wellbeing, and diversity, offering competitive benefits and focusing on attracting and retaining talent. They maintain rigorous compliance with a Code of Business Conduct and Ethics, and their workforce comprises 23% females and 22% minorities. The company's operational strategy involves consistent production and exploration of new hydrocarbon opportunities, with a focus on economically viable extraction.

The company's reserve estimation process employs various methods and is overseen by an experienced internal Reserve Evaluation Group, adhering to SEC guidelines. In 2022, Devon engaged DeGolyer and MacNaughton to audit a significant portion of their proved reserves. Financially, Devon operates approximately 6,169 gross wells, owns around 2 million net acres of land, and strategically engages in variable and fixed price contracts, along with financial hedging, to manage price volatility.

Devon's operations are subject to a range of laws and regulations that influence exploration, production, conservation, and environmental compliance, which have progressively increased operating expenses. The company adheres to stringent environmental, health, and safety laws, and faces risks of legal action, fines, and operational restrictions in case of non-compliance. Recent regulatory measures, including those proposed by the BLM to curb methane emissions and flaring, may impose additional operational constraints.

By the Numbers

Annual 10-K Report Summary (2022):

- Operating cash flow: $8.5 billion (74% increase from previous year)

- Oil production: 299 MBbls/d (3% increase from 2021)

- Net earnings: $6 billion (more than double from $2.8 billion in 2021)

- Henry Hub natural gas prices: Averaged $6.65 per Mcf (up from $3.85 per Mcf in 2021)

- Capital expenditures: $2.542 billion (approximately 30% of operating cash flow)

- Stock repurchases: $718 million spent on common stock buybacks

- Dividend rate: Increased, with a variable dividend paid quarterly

- Income tax rate for 2023: Expected to increase to mid-teens (up from 7% in 2022)

- Liquidity: Approximately $1.5 billion in cash at end of 2022

- Debt-to-capitalization ratio: 23%

- Share repurchase program: $2.0 billion authorized

- Capital expenditures for 2023: Projected at $3.6 billion to $3.8 billion (35% higher than in 2022)

Quarterly 10-Q Report Summary (Q3 2023):

- Oil production: 321 MBbls/d (9% year-over-year increase)

- Share repurchase program: $3 billion authorized, $2.1 billion spent

- Liquidity: $3.8 billion, including $0.8 billion in cash

- Operating cash flow: $1.7 billion for the quarter

- Net income: $910 million ($1.42 per diluted share)

- Core earnings: $1.1 billion ($1.65 per diluted share)

- Earnings increase from Q2 to Q3 2023: $368 million

- Production expenses and LOE: Increased

- Field-level cash margins: Improved

- Earnings for nine months ending September 30, 2023: $2.6 billion (decrease from $4.8 billion in 2022)

- Production volumes impact on earnings: $1.0 billion increase year over year

- Realized prices impact on earnings: $3.9 billion decrease

- Hedge settlements: Cash settlement loss change of $(1,179) million

- Delaware Basin field-level cash margin: Increased to $57.01 per Boe

- Capital expenditures for first nine months of 2023: $2.973 billion (up from $1.738 billion in 2022)

- Share repurchases and dividends for 2023: $745 million on repurchases, $1.37 billion paid in dividends

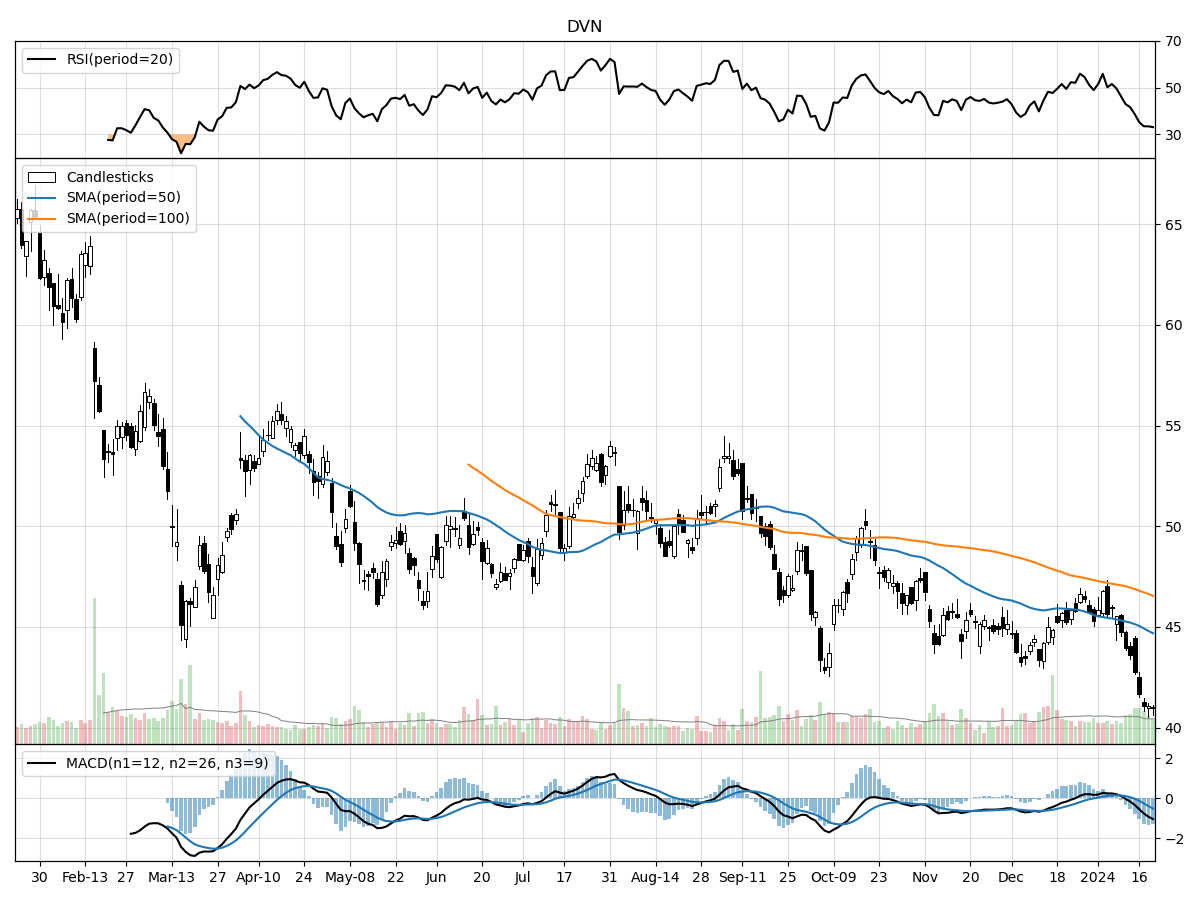

Stock Performance and Technical Analysis

As a stock analyst, I would approach the technical analysis of this stock by looking at several key indicators and trends. The stock is currently trading at $40.97, which is at the same level as its 52-week low, indicating a potential lack of upward momentum or confidence from investors. The proximity to the 52-week low could be perceived as an attractive entry point for value investors if they believe the stock is undervalued. However, it is also 37% below its 52-week high, which signals a significant decline in the stock's price over the past year, possibly reflecting a bearish sentiment or a response to unfavorable market conditions or company-specific news.

The recent trading volume is slightly below its longer-term average, which might suggest a decrease in investor interest or trading activity. This could be a result of the stock's recent performance, where we see a decline of 9.44% in the last month and 13.69% over the last three months. Such a downtrend can often lead to a bearish outlook among investors, potentially causing a further decrease in volume as investors may be exiting their positions or holding off on new investments.

The Money Flow indicators and the Moving Average Convergence Divergence (MACD) also provide valuable insights. The stock is currently under heavy selling pressure and is experiencing distribution, according to the Money Flow indicators. This suggests that more investors are selling their shares than buying, which can contribute to the downward pressure on the stock price. The MACD, being bearish at -0.51, indicates that the short-term momentum is lower than the long-term momentum, reinforcing the bearish trend. The negative MACD value typically suggests that it may not be an optimal time to buy as the stock could continue to decline before finding support.

Overall, the technical analysis paints a bearish picture for the stock. Despite being at its 52-week low, which may attract some investors, the combination of declining prices, selling pressure, and bearish momentum indicators would make me cautious about investing in this stock without further analysis of the company's fundamentals and market conditions. It's essential to consider whether the stock's downturn is due to temporary market volatility or deeper underlying issues before making an investment decision.

The ‘Bull’ Perspective

Unlocking Value in Devon Energy: A Smart Investment for the Future

Executive Summary:

- Robust Production Growth: Devon Energy's oil production surged by 9% year-over-year, reaching 321 MBbls/d, reflecting the company's operational excellence and strategic asset base.

- Aggressive Shareholder Returns: With a $3 billion share repurchase program well underway and a strong dividend track record, DVN is committed to delivering shareholder value.

- Solid Financial Position: A liquidity cushion of $3.8 billion, including $0.8 billion in cash, positions DVN to weather market volatility and continue strategic investments.

- Strategic Hedging in Place: Despite potential earnings volatility due to commodity price fluctuations, DVN's hedging strategy offers a layer of financial stability.

- Resilience Amid Sector Challenges: Considering the identified risks, DVN's strategic initiatives and operational efficiencies enable it to navigate industry headwinds effectively.

Detailed Analysis:

- Robust Production Growth:

Devon Energy's impressive 9% year-over-year increase in oil production to 321 MBbls/d is a testament to its operational prowess. This growth is not just a number; it's a reflection of the company's ability to efficiently extract value from its assets. In an industry where production levels are king, DVN's ability to ramp up output while others struggle is a bullish signal for investors. Furthermore, as the company continues to optimize its asset portfolio, investors can anticipate continued production enhancements, which, given the current market conditions, could translate into significant revenue growth, especially if oil prices remain favorable. - Aggressive Shareholder Returns:

Devon Energy's commitment to shareholder returns is unwavering. The company's share repurchase program, with $2.1 billion already spent, underscores its confidence in its own value proposition. Moreover, the company's dividend payments, which amounted to $1.37 billion year-to-date, demonstrate a strong yield potential for investors. In a market that is increasingly looking for tangible returns, DVN's approach to capital allocation is likely to attract income-focused investors and those looking for a buyback-driven share price appreciation. - Solid Financial Position:

A strong balance sheet is the bedrock of any resilient company, and DVN's $3.8 billion liquidity reserve is a fortress in uncertain times. This financial flexibility enables the company to not only survive but thrive amid market fluctuations, allowing for strategic acquisitions, exploration, and technological investments that can drive future growth. With the ability to generate $1.7 billion in operating cash flow for the quarter, DVN is well-positioned to fund its operations and shareholder return programs without compromising its financial health. - Strategic Hedging in Place:

In an environment where oil and gas prices can be unpredictable, DVN's strategic hedging provides a safety net against severe price swings. By locking in prices for a portion of its 2023 and 2024 production, the company can ensure a more predictable cash flow, which is crucial for planning and executing long-term strategies. While hedging may limit upside potential during price spikes, it is a prudent measure that protects the company's core earnings and provides a stable platform for growth. - Resilience Amid Sector Challenges:

Devon Energy's proactive approach to managing industry risks is indicative of a company that is not only aware of its operating environment but also prepared to confront it head-on. From regulatory changes to environmental concerns, DVN has shown adaptability and foresight in its operations. For instance, its focus on cost efficiencies and margin management helps mitigate the impact of inflationary pressures. Moreover, its attention to environmental, social, and governance (ESG) factors aligns with the broader industry shift towards sustainability, potentially reducing regulatory risk and positioning the company favorably among socially conscious investors.

Conclusion:

In conclusion, Devon Energy presents a compelling investment case. Its robust production growth, aggressive shareholder returns, solid financial position, strategic hedging, and resilience amid sector challenges paint the picture of a company that is not only well-managed but also well-equipped to capitalize on future opportunities. For investors seeking a combination of growth, income, and stability within the energy sector, DVN stands out as a smart choice.

The ‘Bear’ Perspective

Title: A Prudent Approach: Why Investors Should Exercise Caution with Devon Energy Corp.

Upfront Summary:

- Volatile Commodity Prices: Despite a 9% year-over-year production increase, DVN's earnings are heavily influenced by the volatile nature of oil, gas, and NGL prices, which can lead to unpredictable financial outcomes.

- Increased Operational Costs: Production expenses have risen, and the company has reported increased depreciation, depletion, and amortization expenses, indicating potential margin pressures.

- Regulatory and Environmental Risks: Extensive government regulation and environmental policies, such as the IRA, could significantly raise operating costs and impact future profitability.

- Market and Economic Uncertainty: The subdued and bumpy market conditions in early 2024, alongside the potential for interest rate normalization, suggest that DVN's stock may face headwinds.

- Dependence on Continuous Reserve Replacement: The necessity for ongoing discovery or acquisition of new reserves to sustain production levels involves substantial capital and operational risks.

1. Volatile Commodity Prices:

Devon Energy Corp's latest earnings reflect a strong increase in production, but this growth is overshadowed by the inherent volatility of commodity prices. The company's financial performance is closely tied to the whims of the market, with a $368 million increase in earnings from Q2 to Q3 2023 being partially offset by hedge cash settlement payments. While hedging strategies can mitigate price volatility, they also limit the upside potential during periods of high commodity prices. Furthermore, the company's reported net income of $910 million in Q3 2023, while substantial, cannot be taken for granted as a stable trend due to the unpredictable nature of the energy market.

2. Increased Operational Costs:

Devon Energy has been grappling with increased production expenses, which have risen alongside oil production. This includes a surge in depreciation, depletion, and amortization (DD&A) expenses, as well as general and administrative (G&A) expenses per Boe, primarily due to non-labor cost increases. These rising costs, if not managed effectively, could squeeze the company's margins and reduce profitability. With capital expenditures climbing to $2.973 billion for the first nine months of 2023, reflecting inflation and development activities, there's a clear indication that maintaining and expanding operations is becoming more expensive.

3. Regulatory and Environmental Risks:

The regulatory and environmental landscape presents significant risks for DVN. The company is already anticipating the impact of the Corporate Alternative Minimum Tax (CAMT) and is analyzing the utilization of tax credits. Stringent regulations, particularly those addressing hydraulic fracturing, emissions, and waste disposal, have the potential to further increase operating costs. As governments worldwide intensify their focus on climate change and environmental protection, DVN may face additional compliance costs, operational constraints, and a reduction in demand for its products.

4. Market and Economic Uncertainty:

The financial markets have kicked off 2024 with a sense of caution, following a strong rally in the last few weeks of 2023. With the S&P 500 experiencing only a modest uptick of about 0.2% year-to-date, and sectors like technology and healthcare showing outperformance, energy stocks like DVN could struggle to maintain momentum. The Federal Reserve's stance on interest rates and the possibility of rate normalization, with the 10-year Treasury yield now above 4.0%, could introduce additional volatility that may not bode well for DVN's stock performance.

5. Dependence on Continuous Reserve Replacement:

Devon Energy's ability to sustain its production levels hinges on the continuous discovery or acquisition of new reserves. This ongoing need requires significant capital investment and carries operational risks such as drilling unprofitable wells or encountering higher operational costs. Despite the company's efforts to fund capital expenditures through operating cash flow, the necessity for constant capital deployment to replace reserves presents a long-term challenge that could affect the company's growth and financial stability.

In conclusion, while Devon Energy Corp has shown some operational strengths, the combination of volatile commodity prices, increased operational costs, regulatory and environmental risks, market and economic uncertainty, and the dependence on continuous reserve replacement makes it a potentially risky investment in the current climate. Prudent investors may want to maintain a cautious stance and closely monitor these factors before making any investment decisions regarding DVN's stock.

Comments ()