Dropbox Inc. (DBX), Mid/Small Cap AI Study of the Week

March 21, 2024

Weekly AI Pick from the S&P 400 or S&P 600

Company Overview

Dropbox, Inc. is a cloud-based service provider that has expanded from a file synchronization service to a comprehensive collaboration platform, aiming to streamline work for individuals and teams. With a user base of over 18.12 million paying customers, the company has developed a suite of products including Dropbox Passwords, Vault, and Dropbox Sign, and integrates with major tech platforms like Microsoft and Google. Its revenue largely comes from users who upgrade to paid subscriptions, with a self-serve model accounting for over 90% of its income. The company also offers a developer platform, with close to a million developers and extensive API activity, indicating a vibrant ecosystem for app integration.

Dropbox provides a variety of services such as file storage, backup, and collaborative tools, and has introduced features like Dropbox Rewind and Computer Backup. Security is a priority, with measures like encryption and file recovery in place, especially for Dropbox Business users. The company caters to a diverse customer base with different subscription plans and has a strong commitment to privacy and regulatory compliance, including HIPAA and GDPR. Despite stiff competition in the cloud storage market, Dropbox differentiates itself through user-friendly design and continuous innovation, backed by a significant portfolio of patents and trademarks.

In terms of workforce and corporate culture, Dropbox has reduced its global staff by 16% to bolster growth and profitability, now employing 2,693 full-time workers. It has embraced a "Virtual First" work policy, supporting remote work with resources like Dropbox Studios and On-Demand Spaces. Compensation for employees includes a mix of salary, bonuses, equity awards, and benefits, with an emphasis on diversity, wellness, and community involvement. The company is transparent about its operations and financial status, sharing information through its website and SEC filings.

By the Numbers

Certainly, here are the key numerical highlights from Dropbox, Inc.'s annual and quarterly reports:

Annual 10-K Report Summary:

- Total users: Over 700 million

- Paying customers: 18.12 million

- Workforce reduction: 16%

- Workforce reduction expenses: $39.3 million

- Impairment charge on real estate assets: $3.6 million (down from $175.2 million in 2022)

- One-time gain from lease termination: $158.8 million

- Total Annual Recurring Revenue (ARR): $2,523 million (up from $2,514 million in 2022)

- Average Revenue Per Paying User (ARPU): $139.38 (up from $134.51)

- Free Cash Flow (FCF): $759.4 million (down from $763.5 million in 2022)

- Annual revenue: $2,501.6 million (up 7.6%)

- Net income: $453.6 million (down from $553.2 million in 2022)

- Cost of revenue: $478.5 million (up 7.7%)

- Gross margin: Consistent at 81%

- Increase in provision for benefit from income taxes: $461.3 million

- Cash and cash equivalents: $614.9 million

- Short-term investments: $741.1 million

- Stock repurchase authorization: Additional $1.2 billion

- Future cash commitments: $674.7 million in operating leases, $307.2 million in finance leases

Quarterly 10-Q Report Summary:

- Paying subscribers: 18.17 million

- Workforce reduction costs: $38.9 million (to be recognized by Q3 2023)

- Total Annual Recurring Revenue (Total ARR): $2.525 billion

- Average Revenue Per Paying User (ARPU) for Q3 2023: $138.71 (up from $134.31 in Q3 2022)

- ARPU for the nine months ending September 30, 2023: $140.63 (up from $134.41 in 2022)

- Free Cash Flow (FCF) for the nine months ending September 30, 2023: $569.1 million (down from $581.8 million in 2022)

- Quarterly revenue: $633.0 million (up 7.1%)

- Gross profit for the quarter: $513.4 million

- Gross margin: Consistent at 81%

- Net income for the quarter: $114.1 million (up from $83.2 million)

- Revenue for the nine months ending September 30, 2023: $1.866.6 million (up 8.1%)

- Cash and equivalents: $604.3 million

- Short-term investments: $704.6 million

These figures provide a snapshot of Dropbox's financial health, growth trajectory, and operational changes. The company has demonstrated resilience in its revenue growth and ARPU, despite a slight decline in net income and free cash flow, largely due to workforce reduction costs and macroeconomic factors.

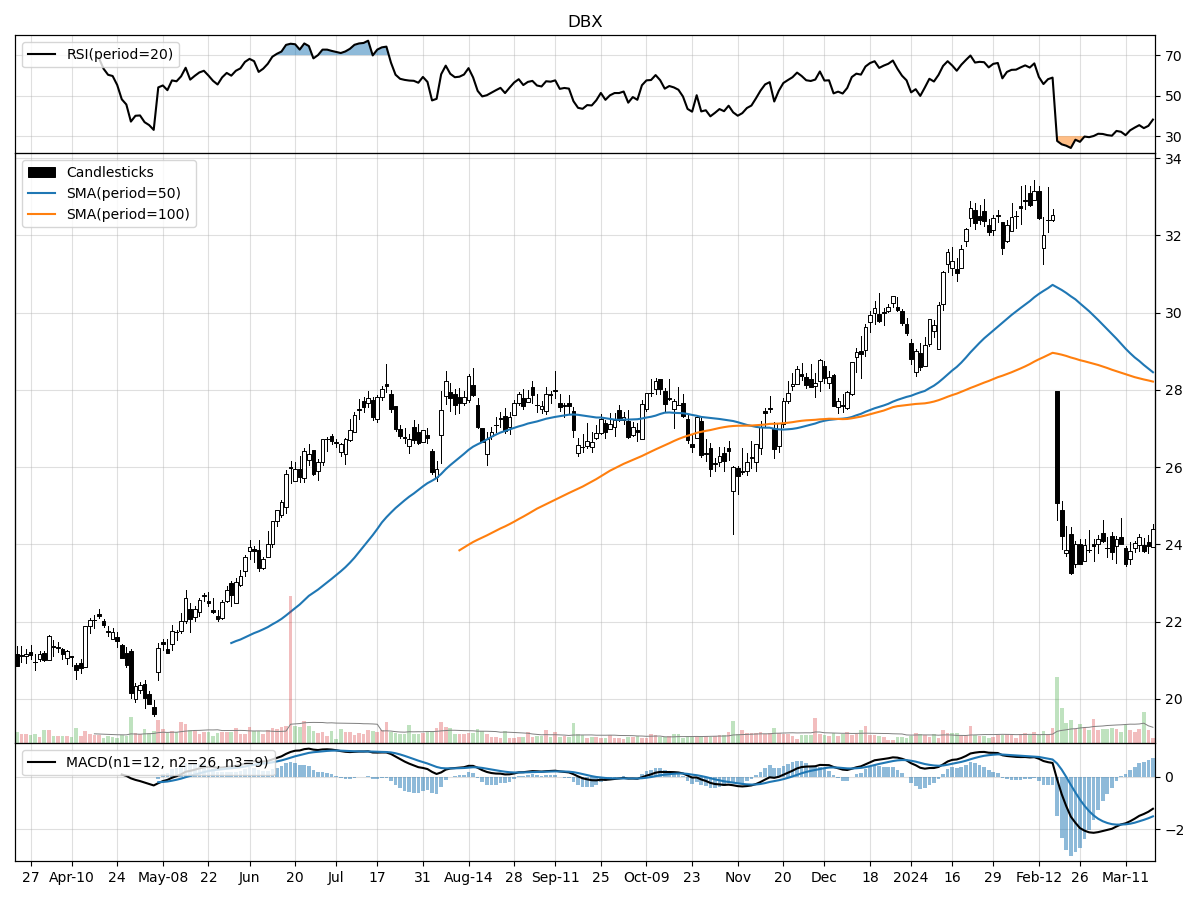

Stock Performance and Technical Analysis

Based on the provided technical data, there are several indications of the stock's performance and potential future direction. The current stock price being 24% above its 52-week low and 26% below its 52-week high suggests that the stock has seen better days but has also rebounded from its lowest point in the past year. This middle-ground positioning might indicate that the stock has room for growth but is also not without its risks, as it has not yet shown signs of challenging its previous high.

The recent daily volume of 5,119,812.3 shares is significantly higher than the longer-term average of 3,644,073.2 shares per day, which could imply increased investor interest or volatility. A high trading volume can be a double-edged sword; it may mean that the stock is gaining attention due to a positive catalyst, or it could also reflect uncertainty and higher levels of trading activity due to investor concern.

The Money Flow indicators present a mixed picture. The stock is under moderate buying pressure, which suggests that there is some accumulation of shares, potentially signaling optimism among investors. Conversely, the claim that the stock is under distribution indicates that there might be a selling pressure, as holders of the stock could be offloading their shares, possibly due to a lack of confidence in future price appreciation.

The Moving Average Convergence Divergence (MACD) being bearish at -1.50 adds to the cautious outlook. A bearish MACD indicates that the short-term momentum is declining relative to the long-term momentum, suggesting that the stock could be entering a downtrend or losing steam in an existing downtrend.

In summary, the stock presents some positive signs with moderate buying pressure and a price level that has recovered from its lows. However, the bearish MACD, mixed Money Flow indicators, and significant drop over the last three months introduce caution into the analysis. An investor should weigh these technical indicators against the company's fundamental qualities, recent news, and market conditions before making an investment decision.

The ‘Bull’ Perspective

Dropbox, Inc. (DBX): A Buy for the Forward-Looking Investor

Upfront Summary:

- Robust User Base and ARPU Growth: With over 700 million users and an ARPU that has increased to $138.71, Dropbox exhibits strong growth potential.

- Strategic Cost Management: The company's transition to a Virtual First model and workforce reduction is expected to result in significant cost savings.

- Innovation and AI Investment: Dropbox's strategic investments in AI position it to capitalize on the growing demand for smart collaboration tools.

- Financial Resilience Amidst Market Recovery: Despite a challenging economic environment, Dropbox maintains a healthy balance sheet with $604.3 million in cash and equivalents.

- Market Position and Share Repurchase Program: A $1.2 billion share repurchase program signals confidence in the company's value proposition and commitment to shareholder returns.

Elaboration on Key Points:

- Robust User Base and ARPU Growth:

Dropbox's expansive user base of over 700 million users is a testament to its global reach and the value proposition it offers. The company's ability to grow its Average Revenue Per Paying User (ARPU) to $138.71 for Q3 2023, even amidst currency fluctuations, is indicative of its pricing power and successful up-selling strategies. The acquisition of FormSwift and the repackaging of premium plans have contributed to this growth. The slight uptick in ARPU is a positive sign when considering the broader market context where the S&P 500 Index has risen to new all-time highs, suggesting that Dropbox is well-positioned to ride the wave of the current bull market rally. - Strategic Cost Management:

Dropbox's recent workforce reduction is a difficult but necessary step towards streamlining operations and cutting costs. The move to a Virtual First work model is expected to save on facilities costs and reduce real estate asset depreciation, with the full financial impact to be recognized by Q3 2023. This strategic cost management is occurring at a time when the banking system has stabilized post-crisis, and bank deposits have shown resilience. Dropbox's proactive approach to managing its expenses will likely enhance its ability to navigate future economic uncertainties. - Innovation and AI Investment:

The future of work is increasingly reliant on AI and machine learning to enhance productivity and collaboration. Dropbox's investment in AI is a strategic move that positions it to be at the forefront of this technological shift. While the tech sector is known for rapid changes and intense competition, Dropbox's focus on AI innovation could lead to the development of new products and services that differentiate it from competitors. This is crucial as the company operates in a market with tech behemoths like Microsoft and Google, which are also investing heavily in AI. - Financial Resilience Amidst Market Recovery:

Dropbox's solid financial standing, with over $1.3 billion in cash, cash equivalents, and short-term investments, provides it with the resilience to withstand market volatility and invest in growth opportunities. The company's free cash flow, though slightly decreased to $569.1 million, remains robust and is expected to increase in the future. This financial health is particularly reassuring given the past year's market recovery and the strong performance of the stock market, which Dropbox is well-positioned to benefit from. - Market Position and Share Repurchase Program:

The authorization of a $1.2 billion share repurchase program is a strong signal of Dropbox's confidence in its market position and commitment to delivering value to shareholders. This move is likely to support the stock price and reflects a responsible allocation of capital. Dropbox's diversified customer base, with no single customer accounting for more than 1% of revenue, provides stability and reduces dependency on any single revenue source. This positions Dropbox favorably in a market that has seen significant recovery over the past year, and as investors look for companies with sound financial strategies and growth prospects.

Conclusion:

In light of the aforementioned points, Dropbox, Inc. (DBX) presents a compelling buy opportunity for investors. The company's strategic focus on growing its user base and ARPU, coupled with cost management initiatives and investments in AI, positions it for sustainable growth. Its financial resilience and proactive shareholder value initiatives further bolster the case for Dropbox as a smart addition to an investor's portfolio, especially within the context of a recovering market and a bullish investment climate.

The ‘Bear’ Perspective

Title: The Case for Caution: Evaluating Dropbox, Inc. (DBX) in the Current Market Landscape

Upfront Summary:

- Declining Growth Trends: Dropbox's growth rate is showing signs of deceleration, with increased competition and market saturation posing significant challenges.

- Cybersecurity and Operational Risks: The company faces serious cybersecurity threats and operational risks, including the complexities of managing a Virtual First work model.

- Competitive Disadvantages: Dropbox competes against larger entities with more resources, which could lead to market share erosion and pricing pressures.

- Economic and Market Sensitivity: The company's subscription-based revenue model is sensitive to economic downturns and shifts in consumer preferences.

- Dependence on Key Personnel: Dropbox's reliance on its CEO and other key personnel presents a risk to business continuity and future growth.

Elaboration on Points:

- Declining Growth Trends:

Dropbox, Inc. has been a notable player in the cloud storage and collaboration market, but recent trends indicate a slowdown in growth. While the company has reached over 700 million users, the rate of converting free users to paying subscribers is critical for sustained revenue growth. The latest figures show a growth rate deceleration, which is concerning given the company's heavy reliance on subscription sales. Dropbox's Total ARR has increased to $2.525 billion, but this is largely due to price increases and acquisitions rather than organic growth. The ARPU's modest rise to $138.71 also reflects the challenge of driving significant growth in a mature market. Moreover, the competition from tech giants like Microsoft and Google, with their integrated ecosystems, puts Dropbox at a disadvantage in attracting new users and retaining existing ones. - Cybersecurity and Operational Risks:

In an era where data breaches are increasingly common, Dropbox's cybersecurity risks are a major concern for investors. Despite the company's efforts in security, any potential breach could lead to a loss of user trust, regulatory fines, and significant financial repercussions. The transition to a Virtual First work model, while cost-effective, introduces new complexities in maintaining robust security measures across a distributed workforce. Operational risks also stem from the company's reliance on third-party providers and the need to scale IT systems to match growth. These challenges, coupled with the historical data breach, underscore the vulnerability of Dropbox's business model in the face of sophisticated cyber threats. - Competitive Disadvantages:

Dropbox is up against formidable competitors with deeper pockets and broader product ecosystems. This competition is not just about market share but also about innovation and pricing. Dropbox's investment in AI and new product initiatives is crucial, but it may not be enough to keep pace with the likes of Amazon, Microsoft, and Google, who can leverage their vast resources for rapid development and aggressive pricing strategies. Dropbox's market position could be further weakened if these competitors decide to prioritize their own collaboration tools, potentially sidelining Dropbox's offerings. - Economic and Market Sensitivity:

The subscription-based model that Dropbox relies on is highly sensitive to economic fluctuations and consumer sentiment. In the face of economic downturns or catastrophic events, users may opt for free alternatives or downgrade their subscriptions to save costs. The recent bank crises and the subsequent economic uncertainty could lead to a tightening of consumer and business spending, which would directly impact Dropbox's revenue. Additionally, the company's international presence exposes it to currency exchange rate fluctuations, which have already had a negative impact on its financials. - Dependence on Key Personnel:

Dropbox's success is closely tied to its leadership, particularly CEO Andrew W. Houston. Any changes in the management team could disrupt the company's strategic direction and operational efficiency. The loss of key personnel or the inability to attract and retain talent in a competitive market could hinder Dropbox's innovation and response to market demands. This risk is compounded by the challenges of maintaining a cohesive company culture and effective communication within a Virtual First work environment.

In conclusion, while Dropbox has demonstrated resilience and adaptability, the combination of declining growth trends, cybersecurity and operational risks, competitive disadvantages, economic and market sensitivity, and dependence on key personnel presents a compelling case for caution among investors. The current market landscape, shaped by recent economic events and evolving consumer behaviors, suggests that Dropbox's path forward may be fraught with challenges that could impact its financial performance and market standing.

Comments ()