Etsy Inc. (ETSY), Large Cap AI Study of the Week

May 21, 2024

Weekly AI Pick from the S&P 500

Company Overview

Etsy Inc. operates as an online marketplace connecting creative buyers and sellers globally, primarily focusing on unique and handmade goods through its main platform, Etsy.com. The company also owns Reverb, a musical instrument marketplace, and Depop, a fashion resale marketplace, forming a diverse "House of Brands." Etsy's strategy emphasizes a sustainable competitive advantage through unique seller items, advanced search technology, fostering human connections, and maintaining a trusted brand. In 2023, the company generated $13.2 billion in Gross Merchandise Sales (GMS), with 88% from the Etsy marketplace and the remainder from Reverb, Depop, and former entity Elo7.

Key growth areas for Etsy include expanding in core geographies like the USA, UK, Germany, Canada, Australia, and France, and promoting cross-border sales, especially in markets like India. Revenue is primarily generated from marketplace activities such as transaction fees, payment processing fees, and listing fees, along with optional seller services like advertising and shipping labels. Etsy aims to enhance cross-border transactions and leverage shared expertise in product, marketing, technology, and customer support across its platforms. The company has launched initiatives to improve buyer consideration and achieve long-term growth by highlighting quality listings and expanding awareness of purchase occasions.

Etsy benefited significantly from the COVID-19-induced shift to online shopping, more than doubling its GMS compared to 2019, but faced challenges in 2022 and 2023 due to increased consumer mobility and macroeconomic headwinds. Despite these challenges, Etsy maintained most of its pandemic gains and grew its revenue through strategic changes to seller fees, payments expansion, and technology advancements in Etsy Ads. Reverb and Depop also maintained their pandemic GMS gains and introduced various initiatives to enhance buyer and seller experiences, contributing to revenue growth. Depop saw significant improvement in performance in 2023, driven by its appeal to value-conscious consumers and substantial growth in the U.S. market.

Etsy leverages technology to connect buyers and sellers globally, emphasizing advancements in machine learning and cloud infrastructure to personalize user experiences and improve operational efficiency. The company invested heavily in marketing, spending approximately $451 million on performance marketing and $162 million on brand marketing in 2023, with significant returns from organic brand awareness. Etsy's product development strategy involves customer and market research, data analysis, and advanced search technologies to enhance buyer and seller experiences across its multiple marketplaces. In 2023, Etsy expanded its performance marketing to several new countries and implemented the Offsite Ads program, generating significant revenue. The company also enhanced its social media and influencer marketing strategies, driving increased ROI and buyer engagement. Subsidiaries Reverb and Depop scaled their paid marketing and trust and safety measures, improving brand awareness and user experience while sharing best practices across platforms.

By the Numbers

Annual 10-K Report Summary (Year Ending December 31, 2023):

- Gross Merchandise Sales (GMS): $13.2 billion

- Total Revenue: $2.7 billion

- Net Income: $307.6 million

- Operating Cash Flows: $705.5 million

- Cash and Equivalents: $1.2 billion

- Workforce Reduction: 11%

- GMS Decline: 1.2% to $13.2 billion

- Revenue Growth: 7.1% to $2.75 billion

- Marketplace Revenue Increase: 4.5%

- Services Revenue Increase: 14.6%

- Operating Expenses Decrease: 33.9% to $1.64 billion

- Net Income Recovery: From a net loss of $694.3 million in the previous year to a net income of $307.6 million

- Adjusted EBITDA Margin: Slight decrease to 27.4%

- Active Sellers Increase: 21.0%

- Active Buyers Increase: 1.5%

- Mobile GMS: 68% of total GMS

- International GMS: 45% of total GMS

- Marketplace Revenue Growth: $86.3 million increase

- Services Revenue Growth: $96.0 million increase

- Asset Impairment Charges: $68.1 million, down from $1.045 billion in 2022

- Other Income (Expense), Net: Increase of $16.4 million to $13.0 million

- Income Tax Benefit: $14.7 million, with a $55.9 million tax benefit related to Elo7

Quarterly 10-Q Report Summary (Q1 2024):

- Gross Merchandise Sales (GMS): $3.0 billion, a 3.7% decrease from Q1 2023

- Total Revenue: $646.0 million, a 0.8% increase from Q1 2023

- Net Income: $63.0 million, a 15.5% decrease from Q1 2023

- Adjusted EBITDA: $167.9 million, a 1.4% decrease from Q1 2023

- Adjusted EBITDA Margin: Decrease from 26.6% to 26.0%

- Active Sellers: 9.1 million, a 15% increase from Q1 2023

- Active Buyers: 96.4 million, a 0.9% increase from Q1 2023

- Services Revenue Growth: 3.2% increase from Q1 2023

- Marketplace Revenue: Nearly flat with a 0.1% decline from Q1 2023

- GMS outside the U.S.: 3% decrease from Q1 2023

- Marketing Expenses: 12% increase from Q1 2023

- Product Development Costs: 5.2% decrease from Q1 2023

- Net Working Capital: $839.3 million

- Operating Cash Flow: $69.0 million, an increase from $55.6 million in Q1 2023

- Cash Used in Investing Activities: $25.1 million, a decrease from $36.1 million in Q1 2023

- Cash Used in Financing Activities: $163.0 million, a slight increase from Q1 2023

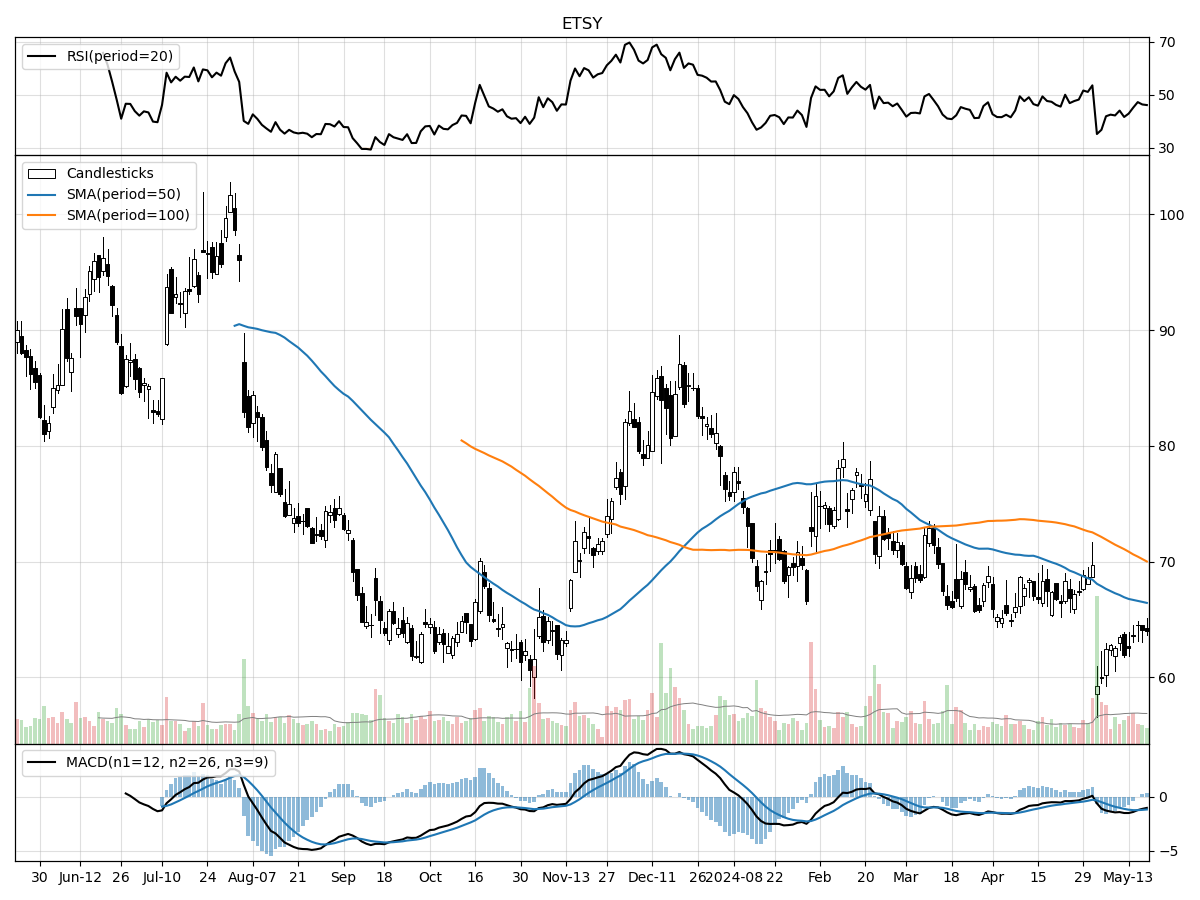

Stock Performance and Technical Analysis

When analyzing a stock from a technical perspective, it is critical to consider several indicators to understand the market sentiment and potential future price movements. The current stock price is 7% above its 52-week low and 37% below its 52-week high, which suggests that the stock has recently been in a downtrend but has recovered from its lowest point. Investors might view this as a potential sign of stabilization or a base formation, indicating a possibly attractive entry point if they believe the stock's fundamentals are strong and the market has overly punished the stock.

The stock's recent daily volume is slightly above its longer-term average, which can imply a heightened interest in the stock. However, this increase in volume is not substantial, so we may not infer a strong conviction behind the price moves. The Money Flow indicators suggest moderate buying pressure, and the stock is under accumulation, which could indicate that investors are starting to see value at these levels and are accumulating shares. This is further supported by the Relative Strength Index (RSI), which indicates that the stock is neither overbought nor oversold, suggesting that there hasn't been any extreme sentiment that has pushed the stock price to unsustainable levels recently.

The Moving Average Convergence Divergence (MACD) is bearish at -1.15, showing that the short-term momentum is weaker than the long-term momentum, and that the stock may continue to experience downward pressure in the near term. However, the MACD is just one indicator, and it should be weighed against others, such as the RSI and Money Flow, to get a more balanced view of the stock's potential.

Overall, while there are signs of accumulation and moderate buying pressure, the bearish MACD suggests investors should be cautious. If considering an investment, it may be wise to look for additional confirmatory signals of an upward trend or consider dollar-cost averaging into a position to mitigate the risks of short-term volatility. As always, it is important to align technical analysis with an assessment of the company's fundamentals and any relevant news or sector trends before making an investment decision.

The ‘Bull’ Perspective

Summary:

- Stable Revenue Amidst Economic Headwinds: Despite a slight decrease in Gross Merchandise Sales (GMS), Etsy reported a year-over-year revenue increase to $646.0 million, showcasing its ability to maintain revenue streams even in challenging times.

- Expanding Market Presence: With a 15% increase in active sellers, Etsy continues to grow its marketplace, signaling a robust platform that attracts and retains creative entrepreneurs.

- Solid Financial Position: Etsy's strong liquidity, including $839.3 million in net working capital and a $400.0 million credit facility, provides a cushion against economic fluctuations and supports strategic growth initiatives.

- Operational Efficiency: A decrease in product development costs by 5.2% reflects Etsy's focus on operational efficiency, which is crucial for maintaining profitability.

- Resilient Buyer Base: The platform's slight growth in active buyers amidst economic uncertainties demonstrates the resilience of its consumer base and the enduring appeal of unique, handcrafted goods.

1. Stable Revenue Amidst Economic Headwinds

Despite the broader economic challenges that have led to a 3.7% decline in GMS, Etsy has managed to slightly increase its total revenue to $646.0 million, a testament to its diversified revenue streams and the strength of its business model. This stability is particularly impressive given the current inflationary environment and its impact on discretionary spending. While net income saw a decrease, the company's ability to maintain revenue growth during such periods is a strong indicator of its underlying business health and its potential for recovery when economic conditions improve.

2. Expanding Market Presence

Etsy's 15% increase in active sellers in Q1 2024 indicates that the platform remains an attractive destination for creative entrepreneurs looking to reach a global audience. This growth in sellers expands the variety and uniqueness of products available, which can draw in more buyers and enhance the overall marketplace ecosystem. A larger seller base also diversifies risk and increases the potential for future revenue growth as these sellers become more established on the platform.

3. Solid Financial Position

Etsy's robust liquidity position, with substantial net working capital and access to a sizable credit facility, provides the financial flexibility to navigate the current economic landscape. This strong liquidity position also enables the company to invest in growth opportunities and weather potential downturns without the immediate need for external financing. The positive operating cash flow of $69.0 million further underscores Etsy's ability to generate cash from its operations, which is a critical factor for long-term financial stability.

4. Operational Efficiency

The reduction in product development costs by 5.2% demonstrates Etsy's commitment to operational efficiency. By optimizing its spending on product development while still fostering innovation, Etsy can improve its margins and profitability. This strategic approach to managing expenses is crucial in an economic environment where cost control becomes increasingly important for sustaining business operations and investing in areas that drive growth.

5. Resilient Buyer Base

The growth in active buyers, albeit modest at 0.9%, is a positive sign in the face of economic pressures that could easily dampen consumer spending. Etsy's ability to retain and slightly grow its buyer base suggests that the platform offers products that resonate with consumers' desire for unique and personalized items. This resilience in buyer activity is essential for maintaining a steady flow of GMS and positions the company well for leveraging any upturn in consumer confidence and spending.

In conclusion, while Etsy faces a variety of risks, including fluctuations in revenue growth, macroeconomic uncertainties, operational challenges, and competitive pressures, the company's latest financial results and strategic positioning indicate a resilient platform with a solid foundation for growth. Etsy's stable revenue, expanding market presence, strong financial position, operational efficiency, and resilient buyer base make it a compelling investment opportunity for those looking to capitalize on the long-term potential of e-commerce and the unique value proposition of the Etsy marketplace.

The ‘Bear’ Perspective

Summary:

- GMS Decline: Etsy's Gross Merchandise Sales (GMS) have dropped by 3.7% year-over-year, signaling potential underlying issues in the marketplace's core business model.

- Net Income and EBITDA Downtrend: The company's net income has decreased by 15.5%, with a marginal decline in adjusted EBITDA, raising concerns about profitability and operational efficiency.

- Elevated Marketing Expenses: Marketing expenses have risen by 12%, yet this has not translated into proportional GMS growth, questioning the return on investment for these expenditures.

- Seller and Buyer Dynamics: A significant 15% increase in active sellers outpaces the growth in active buyers, which may lead to market saturation and increased competition among sellers.

- Macroeconomic and Regulatory Risks: Etsy's performance is subject to macroeconomic conditions, regulatory changes, and cybersecurity threats, which could further destabilize the company's financials.

Elaboration:

- GMS Decline:

Etsy's recent GMS decline from $3.1 billion to $3.0 billion is a red flag for investors. This 3.7% decrease is particularly concerning in a marketplace that relies on the vibrancy of its transactions. A decline in GMS could indicate a broader disengagement from buyers or an inability to attract new customers, which is critical for a platform that thrives on a diverse and dynamic range of products. Furthermore, with the GMS outside the U.S. shrinking by 3%, international expansion strategies may be faltering, which could limit future growth opportunities. - Net Income and EBITDA Downtrend:

Etsy's net income slide to $63.0 million, a 15.5% drop, is a stark warning about the company's earning capabilities. Coupled with a 1.4% dip in adjusted EBITDA to $167.9 million, these figures suggest that Etsy's cost management and revenue generation are not as robust as they need to be. The declining adjusted EBITDA margin from 26.6% to 26.0% may seem marginal, but it points to a potential trend of eroding profitability, which is a critical indicator of long-term sustainability for investors. - Elevated Marketing Expenses:

Investing in marketing is essential for growth, but when marketing expenses surge by 12% without a corresponding increase in GMS or active buyers, questions arise about the efficiency of Etsy's marketing strategy. The company needs to demonstrate that its marketing efforts can effectively convert into higher sales and a larger customer base. Otherwise, the increased spending could simply be inflating operational costs without delivering tangible benefits, which is a poor signal for investors. - Seller and Buyer Dynamics:

While a 15% increase in active sellers indicates that Etsy's platform is attractive for creative entrepreneurs, the modest 0.9% growth in active buyers does not bode well for these sellers' potential to succeed. An imbalance between sellers and buyers can lead to increased competition, lower sales per seller, and potential seller attrition. If sellers begin to leave the platform due to lower-than-expected sales, Etsy could face a downward spiral of reducing GMS and further declining revenues. - Macroeconomic and Regulatory Risks:

Etsy operates in a broader economic and regulatory landscape that presents numerous risks. Macroeconomic challenges, such as inflation and interest rate fluctuations, can impact discretionary consumer spending, directly affecting Etsy's core business. Regulatory changes and increased scrutiny could lead to higher compliance costs or operational constraints. Moreover, cybersecurity threats are an ever-present risk, especially for online marketplaces, and any significant breach could erode trust and lead to costly remediation efforts.

In conclusion, while Etsy remains a popular platform for unique and handcrafted goods, the current financial trends and external risks paint a cautious picture for investors. The decline in GMS, coupled with a decrease in profitability metrics and the potential inefficiency of increased marketing spend, suggests that Etsy may be facing headwinds that could impact its future performance. Investors should weigh these factors carefully when considering their investment strategy regarding Etsy Inc.

Comments ()