Hormel Foods Corporation (HRL), Large Cap AI Study of the Week

February 27, 2024

Weekly AI Pick from the S&P 500

Company Overview

Hormel Foods Corporation, a global food company founded in 1891, has seen significant growth, boasting over $12 billion in annual revenue. The company's recent strategic moves include acquiring the Planters® snack nuts business in fiscal 2021 and purchasing a 30% stake in Garudafood, an Indonesian food and beverage company, in fiscal 2023. Hormel operates primarily through three segments: Retail, Foodservice, and International, with a presence in all 50 states and key international markets like China and Brazil. The company markets its branded food products, which are mainly pork and turkey-based, through direct sales, brokers, and distributors, and also has global manufacturing and licensing agreements in place.

Hormel's commitment to its workforce is evident through its investment in development, diversity, and safety, as well as health and wellness programs for its 20,000 employees worldwide. The company is also focused on sustainability, as demonstrated by its 20 by 30 Challenge aimed at reducing environmental impact. Walmart is Hormel's largest customer, accounting for 15% of sales, and the top five customers collectively represent 36% of total sales. Hormel operates in a competitive sector, vying with others based on price, quality, brand recognition, and product innovation. Intellectual property like patents and trademarks, including well-known brands such as SPAM and SKIPPY, are crucial to Hormel's operations, and the company is attentive to regulatory compliance to avoid any significant adverse impacts.

By the Numbers

- Fiscal Year 2023 Annual Report:

- Net sales: $12.1 billion (3% decline from the previous year)

- Net earnings: $792.92 million (21% decrease from the previous year)

- Earnings per share (EPS): $1.45 (from $1.82 the previous year)

- Dividend increase: 3% for 2024

- Cost of Products Sold: $10.11 billion (1.8% decrease)

- Gross profit: Declined by 7.6%

- Gross margin: Decreased from 17.4% to 16.5%

- SG&A expenses: $942.2 million (increased)

- Advertising investments: $160 million (increased)

- Interest expenses: Increased by 17.4%

- Effective tax rate: 21.8% (slightly lower than the previous year)

- Segment Performance (Fiscal Year 2023):

- Retail: 40.3% decline in quarterly profit; 20% annual drop

- Foodservice: 13.1% growth in quarterly profit

- International: 12.0% decrease in net sales; 67.0% reduction in quarterly segment profit

- Fiscal Year 2024 Outlook:

- Sales growth: Anticipated 1-3%

- Earnings per share: Projected range of $1.43 to $1.57

- Adjusted earnings per share: $1.51 to $1.65 (excluding transformation charges)

- Quarterly Report (Q3 Fiscal Year 2023):

- Diluted EPS: $0.30 (25% decrease)

- Adjusted diluted EPS: $0.40 (stable)

- Net sales: 2% decrease

- Segment profit: 2% decrease

- Earnings before income taxes: 28% reduction

- Cash flow from operations: 5% decrease year-to-date

- Segment Performance (Q3 Fiscal Year 2023):

- Retail: 7.3% decrease in quarterly profit; 12.2% decrease over nine months

- Foodservice: 13.6% growth in quarterly profit

- International: 50% decrease in quarterly profit; 42% decrease over nine months

- Financial Position (Q3 Fiscal Year 2023):

- Gross profit: Decreased by 7.1%

- Operating income: Decreased by 7.8%

- Net earnings: Decreased by 9.4%

- Cash and cash equivalents: Significant reduction

- Capital expenditures: Increased

- Cash dividends: Increased to $443 million from $416 million

- Annual dividend rate: $1.10 per share for fiscal 2023

These figures highlight the key financial metrics and changes for Hormel Foods Corp during the reported periods, providing a numerical basis for investment analysis.

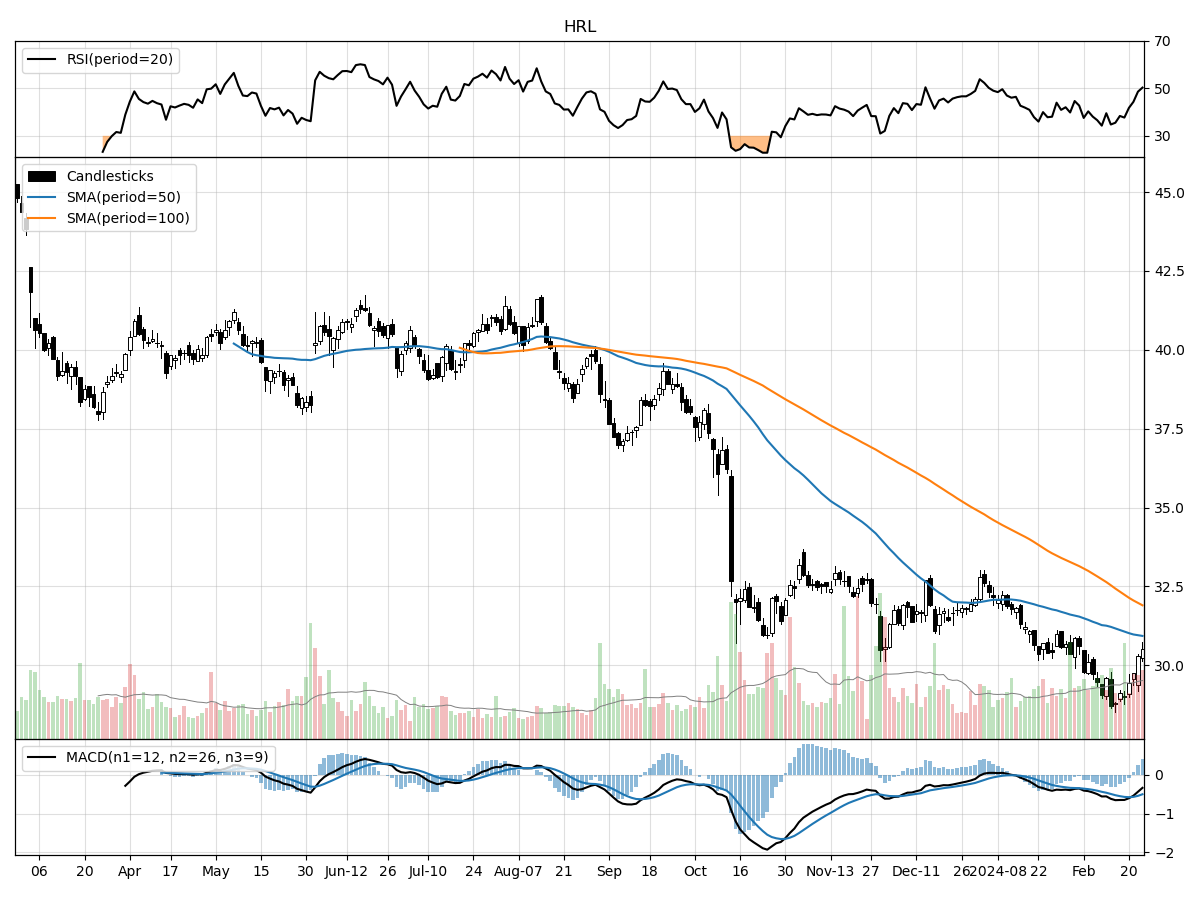

Stock Performance and Technical Analysis

The technical analysis of the stock in question presents a mixed picture with some bearish signals. The stock is currently trading at $30.51, which is 6% above its 52-week low and 32% below its 52-week high. This suggests that while the stock has rebounded somewhat from its lowest point in the past year, it is still significantly below the peaks it has seen, indicating potential room for recovery if bullish sentiment returns. However, caution is warranted as the stock is substantially off its highs, which could suggest that there has been a change in the fundamentals or market sentiment around the company.

The fact that the current daily volume is higher than the longer-term average volume may indicate increased investor interest or volatility in the stock. Typically, a higher trading volume can correspond with significant price movements, either bullish or bearish, depending on the context. However, it's noted that the price has remained relatively stable in the last month and three months, which could mean that despite the increased volume, there is a lack of direction or conviction in the market about the stock's future price movements.

Two important technical indicators to consider are the Money Flow indicators and the Moving Average Convergence Divergence (MACD). Money Flow indicators suggest that the stock is under moderate selling pressure and is experiencing distribution, which means that more investors might be selling their shares than buying, potentially leading to a downward pressure on the stock price. The MACD is currently bearish at -0.49, which typically indicates that the short-term momentum is lower than the long-term momentum and could be considered a sell signal.

In conclusion, the technical analysis suggests caution. The combination of the stock trading well below its 52-week high, the presence of moderate selling pressure, and a bearish MACD would typically advise against taking a long position at this time. However, each investor should consider their risk tolerance, investment horizon, and the context of the broader market and any company-specific fundamental analysis before making a decision.

The ‘Bull’ Perspective

Upfront Summary:

- Robust Dividend History: Hormel Foods boasts an impressive track record of 57 consecutive years of dividend increases, a testament to its financial stability and shareholder commitment.

- Strategic Acquisitions: The company's strategic investments, including a $426 million investment in Garudafood, position it for diversified growth and access to new markets.

- Foodservice Segment Strength: Hormel's Foodservice segment saw a 13.6% profit increase in Q3, highlighting resilience and growth potential in this division.

- Strong Brand Portfolio: Hormel's portfolio includes leading brands like SPAM® and Skippy®, which continue to drive consumer loyalty and sales.

- Adaptability to Market Trends: Hormel is actively adapting to consumer trends, such as the demand for sustainable and plant-based options, positioning it well for future market shifts.

Elaborating on the Investment Case:

- Dividend Aristocrat Status:

Hormel Foods Corporation's dividend history is nothing short of remarkable. For 57 years, the company has not only paid but also increased its dividends, showcasing a robust financial foundation that can weather market volatility. With an annual dividend rate set at $1.10 per share for fiscal 2023, Hormel demonstrates a commitment to returning value to shareholders. This consistency is particularly appealing in an environment where other companies may cut dividends due to economic pressures. Hormel's ability to maintain and grow its dividend payout ratio is a clear indicator of its operational efficiency and prudent financial management, making it an attractive stock for income-focused investors. - Growth Through Strategic Acquisitions:

Hormel's forward-looking growth strategy is evident in its recent $426 million investment in Garudafood, a move that expands its international footprint and diversifies its product offerings. This strategic acquisition opens up new avenues for revenue growth and mitigates risks associated with market concentration. While acquisitions carry inherent risks, such as integration challenges, Hormel's management has historically demonstrated a capacity to effectively navigate these waters, as reflected in its stable financial performance. The company's willingness to invest in growth, even during economic downturns, underscores its long-term vision and potential for sustained expansion. - Foodservice Segment as a Growth Driver:

The Foodservice segment's 13.6% increase in profit during Q3 is a clear indicator of Hormel's strength in this area. This performance is particularly noteworthy given the broader economic context, where other companies have struggled with fluctuating demand. Hormel's ability to grow its Foodservice profits suggests that it has a competitive edge in terms of product mix and operational efficiency. The growth in this segment could continue to be a significant contributor to Hormel's overall profitability, especially as the economy recovers and demand for dining out potentially increases. - Powerhouse Brands Driving Consumer Loyalty:

Hormel's portfolio is a competitive moat filled with iconic and beloved brands such as SPAM® and Skippy®. These brands have stood the test of time and continue to command significant shelf space and consumer loyalty. The strength of Hormel's brands provides a buffer against market downturns and helps maintain steady cash flows. In an era where brand value is paramount, Hormel's strong brand equity is a significant asset that can drive long-term sales and profitability. - Adapting to Consumer Preferences:

Hormel is not resting on its laurels; the company is actively adapting to evolving market trends. With increased consumer interest in sustainability and plant-based diets, Hormel is positioning itself to capture this growing demographic through product innovation and marketing. By staying attuned to these trends, Hormel can pivot its product offerings to meet emerging consumer demands, thereby ensuring relevance and continued market penetration. This adaptability is crucial in maintaining Hormel's competitive edge in a rapidly changing food industry landscape.

Conclusion:

Hormel Foods Corporation represents a resilient investment in the consumer staples sector, backed by a strong dividend history, strategic growth initiatives, robust segment performance, powerful brand portfolio, and adaptability to consumer trends. While the company faces risks such as economic downturns, market volatility, and industry-specific challenges, its proven track record and strategic positioning suggest that it is well-equipped to navigate these challenges and capitalize on opportunities. Investors looking for a stable yet dynamic player in the food industry may find Hormel to be a compelling choice.

The ‘Bear’ Perspective

- Declining Financial Performance: Hormel's Q3 fiscal 2023 report showed a 25% decrease in diluted net EPS to $0.30 and a 2% drop in net sales.

- Concentrated Segment Struggles: The International segment's profit plunged by 50% for the quarter, significantly impacting overall performance.

- Increased Expenses and Debt: Hormel faces a $70 million expense from an adverse arbitration ruling and increased capital expenditures, potentially straining finances.

- Market and Economic Risks: Economic downturns, geopolitical tensions, and industry-specific challenges could adversely affect Hormel's profitability.

- Overreliance on a Few Segments: The company's heavy reliance on particular segments like Foodservice, which saw a profit increase, could be risky if these sectors face downturns.

Elaboration on Key Points

- Declining Financial Performance

Hormel's recent financials reveal concerning trends that investors should not overlook. The 25% dip in diluted net EPS is a red flag, indicating that the company is not just facing a temporary setback but potentially a more systemic issue. The 2% decline in net sales further compounds this narrative, suggesting that Hormel is struggling to maintain its revenue stream in a competitive market. With the broader market rallying, a company showing such a decline in financial metrics should be approached with caution, especially when considering the potential for decreased consumer demand and rising operational costs in the face of economic uncertainty. - Concentrated Segment Struggles

The International segment's 50% profit nosedive is particularly alarming. This drop reflects not only the volatility of international markets but also Hormel's vulnerability to global economic shifts. While the Foodservice segment's 13.6% profit increase for the quarter might seem like a saving grace, it's important to note that over-reliance on a single segment can be risky. Should the foodservice industry face a downturn or if Hormel fails to sustain its growth in this area, the company's financials could be severely impacted. - Increased Expenses and Debt

The $70 million expense due to the arbitration ruling is a significant financial burden that cannot be ignored. This unexpected cost, coupled with increased capital expenditures for expanding capacity, could strain Hormel's financial resources. These expenditures are occurring at a time when cash flow from operations has already decreased by 5% year-to-date. Such financial pressures could limit the company's ability to invest in growth opportunities or return value to shareholders, potentially leading to a less favorable view of the stock. - Market and Economic Risks

Hormel operates in a highly volatile industry, where economic downturns, geopolitical tensions like the Russia-Ukraine conflict, and industry-specific risks such as food contamination can have a drastic impact on performance. The company's recent struggles with international sales and unfavorable commodity markets, particularly in China, underscore the real and present dangers of global instability. These factors could lead to supply chain disruptions, increased costs, and ultimately, a decline in Hormel's profitability. - Overreliance on a Few Segments

While Hormel's Foodservice segment has been a strong performer, the company's reliance on this and a few other segments poses a risk. Market concentration increases vulnerability to sector-specific downturns and reduces the company's ability to weather storms in any single area of its business. This overreliance is further exacerbated by the potential loss of significant contracts and the intense competition Hormel faces not only from traditional meat producers but also from the growing plant-based protein market.

In conclusion, while Hormel Foods Corporation has been a reputable player in the food products industry, the current financial and market indicators suggest a cautious approach for investors. The combination of declining financial performance, concentrated segment struggles, increased expenses and debt, market and economic risks, and overreliance on a few segments presents a compelling case for investors to hold off on buying, selling, or shorting Hormel's stock at this time.

Comments ()