Intel Corp. (INTC), Large Cap AI Study of the Week

May 14, 2024

Weekly AI Pick from the S&P 500

Company Overview

Intel Corporation is a leading technology company that specializes in the design, development, manufacture, and sale of computing products and services globally. Founded in 1968 and headquartered in Santa Clara, California, Intel is renowned for its semiconductor chip manufacturing, being one of the world’s largest chipmakers by revenue1. The company operates through various segments, including Client Computing Group, Data Center and AI, Network and Edge, Mobileye, and Intel Foundry Services, offering a wide range of products such as CPUs, chipsets, SoCs, GPUs, accelerators, FPGAs, and memory and storage solutions1.

Intel’s influence extends beyond chip manufacturing; it is pivotal in advancing technologies like artificial intelligence, autonomous driving, and digital transformation from cloud to edge. With a strategic focus on developing and deploying intelligent edge platforms and driving standards for efficient operations, Intel serves a diverse clientele, including original equipment manufacturers, cloud service providers, and other manufacturers and service providers. As of 2024, Intel continues to innovate and maintain a significant presence in the technology sector, contributing to the digital landscape with its hardware.

By the Numbers

Based on the annual 10-K report summary provided:

- Total Net Revenue (2023): $54.228 billion

- Total Net Revenue (2022): $63.054 billion

- Total Net Revenue (2021): $79.024 billion

- Year-over-Year Revenue Decline (2022 to 2023): -$8.826 billion

- Notebook Revenue (2023): $17 billion

- Notebook Revenue (2021): $18.8 billion

- Desktop Revenue (2023): $10.2 billion

- Desktop Revenue (2021): $10.7 billion

- Server Revenue (2023): $15.5 billion

- Server Revenue (2022): $19.4 billion (calculated from a $3.9 billion drop)

- Server Operating Income (2023): -$530 million

- Server Operating Income (2022): $1.3 billion

- Edge and AI Solutions Revenue (2023): $5.8 billion

- Edge and AI Solutions Revenue (2022): $8.4 billion (calculated from a $2.6 billion decrease)

- Edge and AI Solutions Operating Income (2023): -$482 million

- Edge and AI Solutions Operating Income (2022): $1 billion

- Mobileye Revenue (2023): $952 million

- Mobileye Revenue (2022): $469 million (calculated from a $483 million increase)

- Operating Margin (2023): 22%

- Operating Margin (2022): 18%

- Gross Margin (2023): 40.0%

- Net Income Attributable to Intel (2023): $1,689 million

These figures highlight a significant decline in revenue across multiple segments, with a particular downturn in server and edge/AI solutions. Despite the overall revenue decline, there was an increase in operating margin and a still-positive net income, indicating some cost control measures may have been effective. The growth in Mobileye's revenue is a positive sign, although it is accompanied by an increased operating loss due to higher strategic growth expenditure.

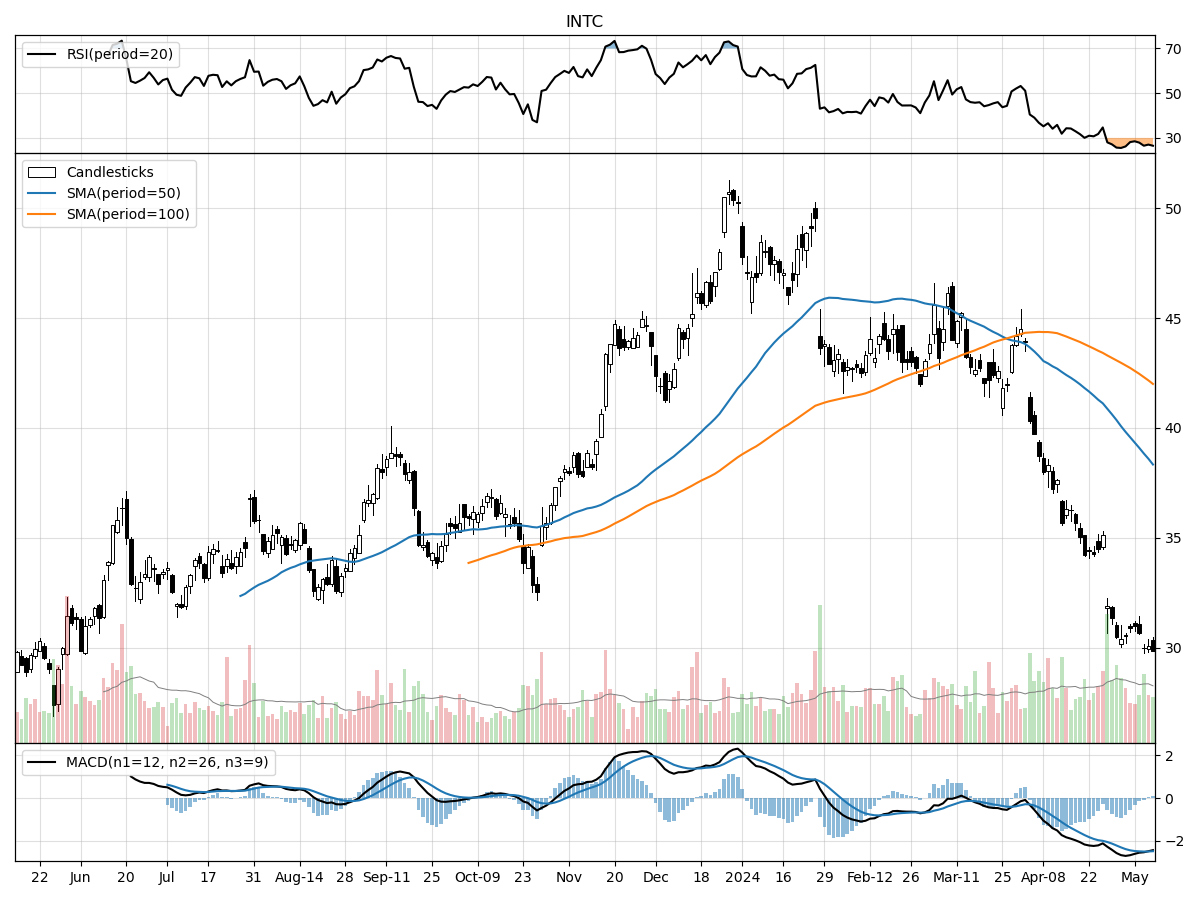

Stock Performance and Technical Analysis

Based on the provided technicals, the stock is currently experiencing a bearish trend, which is reflected by several indicators. The fact that the stock price has fallen significantly in the past month (17.79%) and quarter (32.24%) suggests a strong negative momentum. This downward trend is further supported by the Moving Average Convergence Divergence (MACD), which is currently bearish at -2.48. A negative MACD indicates that the short-term momentum is moving more rapidly downwards compared to the long-term momentum, signaling that the stock may continue to decline.

The stock's current price is 8 percent above its 52-week low and 41 percent below its 52-week high, which indicates that the stock has retracted substantially from its peak but may have found some support above its lowest point in the past year. Nonetheless, the price's position well below the 52-week high shows that the stock has been out of favor with investors for some time.

Furthermore, money flow indicators suggest that the stock is under moderate selling pressure and is experiencing distribution, which means that more investors are selling their shares than buying, potentially leading to an oversupply of the stock and driving the price down. The increased daily volume compared to the longer-term average also indicates that there has been more active trading recently, which when combined with a declining price, likely points to a negative sentiment in the market toward this stock.

In conclusion, while the stock may be trading above its 52-week low, the overall technical analysis suggests that caution is warranted. The bearish MACD, the significant recent price declines, and negative money flow indicators imply that the stock may continue to face downward pressure. Investors should carefully weigh these technical factors against the company's fundamentals and any potential catalysts that could reverse the negative trend before making an investment decision.

The ‘Bull’ Perspective

Intel Corp (INTC): A Smart Investment for Forward-Thinking Investors

Summary:

- Robust R&D Investment: Intel's $16 billion investment in R&D in 2023 positions the company to lead future technological innovation.

- Strategic Expansion: Intel's aggressive expansion with five new manufacturing nodes in four years could significantly enhance its competitive edge.

- Diversified Product Portfolio: Intel's diversified approach, including ventures into discrete GPUs and AI accelerators, opens up new revenue streams.

- Smart Capital Strategy: Intel's Smart Capital approach leverages alternative financing and government grants to mitigate financial risks.

- Supply Chain Resilience: Despite global challenges, Intel's supply chain strategy aims to maintain production efficiency and meet demand.

Elaboration:

- Robust R&D Investment:

Intel's commitment to research and development is unwavering, with a staggering investment of $16 billion in 2023 alone. This financial dedication is a testament to Intel's resolve to overcome its recent setbacks and regain technological supremacy. The R&D efforts are not just about catching up but leapfrogging into a future where Intel's products set the industry standard. With this level of investment, Intel is poised to deliver groundbreaking innovations that could revolutionize the semiconductor industry and drive long-term growth for the company and its shareholders. - Strategic Expansion:

The company's plan to launch five new manufacturing nodes within the next four years is a bold move that could redefine its market position. This expansion strategy is not merely about increasing capacity; it's about enhancing Intel's ability to produce cutting-edge technology at a pace that meets the rapidly growing demand for high-performance computing. If successful, this could lead to a significant improvement in Intel's gross margins and a stronger foothold in the competitive semiconductor market. - Diversified Product Portfolio:

Intel's foray into discrete GPUs and AI accelerators represents a strategic diversification that could unlock new revenue streams and reduce reliance on its traditional CPU business. By entering these high-growth markets, Intel is not only expanding its product lineup but also catering to the burgeoning needs of data centers, gaming, and AI applications. This diversification is crucial in an industry where adaptability and innovation are key to staying relevant and profitable. - Smart Capital Strategy:

Intel's Smart Capital approach, which includes leveraging alternative financing and securing government grants, is a strategic move to balance its heavy investment requirements with financial prudence. This strategy allows Intel to share the risks associated with its ambitious expansion plans and R&D projects. For instance, securing grants for semiconductor manufacturing could alleviate the financial burden and enhance Intel's ability to invest in other critical areas, thus optimizing its capital allocation. - Supply Chain Resilience:

In the face of global supply chain disruptions, Intel's efforts to maintain a resilient supply chain are commendable. The company's strategy to navigate these challenges, including geopolitical tensions and economic uncertainties, is critical for ensuring continuous production and meeting customer demand. By managing its supply chain effectively, Intel can minimize the risks of production halts or delays, which is essential for sustaining its market position and financial performance.

Conclusion:

In conclusion, Intel Corp represents a compelling investment opportunity for those looking to capitalize on the company's strategic initiatives and long-term growth prospects. With substantial investments in R&D, a bold expansion strategy, a diversified product portfolio, a smart capital allocation approach, and a resilient supply chain, Intel is well-positioned to navigate the complexities of the semiconductor industry and deliver value to its shareholders. While the company faces significant risks, its proactive measures and strategic vision suggest that Intel is an investment poised for future success.

The ‘Bear’ Perspective

Title: Navigating Turbulent Waters: Why Intel Corp May Not Be a Buy Right Now

Summary:

- Rising Competition and Market Shifts: Intel faces fierce competition from AMD, Qualcomm, and NVIDIA, with Apple's vertical integration further intensifying the battle for market share.

- Hefty R&D and Capital Expenditures: Intel's R&D spending hit $16 billion in 2023, and rising capital expenditures to update facilities could strain financial resources.

- Manufacturing and Technological Risks: Intel's ambitious plans to launch five manufacturing nodes in four years come with the risk of delays and increased costs, reminiscent of past setbacks with 10nm and 7nm technologies.

- Geopolitical and Supply Chain Vulnerabilities: Geopolitical tensions and a complex global supply chain expose Intel to potential disruptions, increased costs, and manufacturing delays.

- Reliance on Third-Party Foundries and Market Volatility: Intel's pivot to third-party foundries and the unpredictable nature of the semiconductor market add layers of risk to its operational stability and financial outcomes.

Elaboration on Points:

- Rising Competition and Market Shifts:

Intel Corp is in the midst of a market share skirmish as it loses ground to competitors like AMD, which has made significant gains in the CPU market. Qualcomm and NVIDIA continue to dominate in their respective sectors, with NVIDIA's stronghold on the GPU market posing a significant challenge to Intel's nascent discrete GPU efforts. Apple's decision to design its own chips for its devices has not only reduced Intel's customer base but also set a precedent for other tech giants to follow suit. This strategic shift could lead to a 5-10% loss in Intel's market share, according to industry analysts, further jeopardizing its revenue streams. - Hefty R&D and Capital Expenditures:

Intel's substantial R&D investment of $16 billion in 2023 is a double-edged sword. While it underlines the company's commitment to innovation, it also reflects the high costs associated with catching up and potentially leapfrogging competitors in technology leadership. This spending comes at a time when Intel is also increasing its capital expenditures, which surged by 20% year-over-year, to modernize manufacturing facilities. These financial commitments may put pressure on Intel's balance sheet, especially if the returns on these investments do not materialize as planned or are delayed. - Manufacturing and Technological Risks:

Intel's aggressive roadmap to introduce five new manufacturing nodes within four years is fraught with risks. The company has previously experienced significant setbacks, such as the infamous delay of its 10nm and 7nm processes, which allowed competitors to gain a technological edge. These past missteps have led to skepticism among investors, with concerns that history may repeat itself. Intel's current yield rates for its latest nodes have not been disclosed, but industry norms suggest that any new process technology could face yield challenges, potentially leading to lower-than-expected output and higher costs. - Geopolitical and Supply Chain Vulnerabilities:

Geopolitical conflicts, such as the ongoing tensions between the U.S. and China, pose substantial risks to Intel's operations. The company's global supply chain is already experiencing the ripple effects of the Russia-Ukraine conflict, with disruptions leading to a 5% increase in logistics costs. Additionally, local regulatory changes and infrastructure inefficiencies in key markets could further exacerbate these challenges, potentially resulting in a 3-7% impact on Intel's gross margins if alternative sourcing or manufacturing sites are required. - Reliance on Third-Party Foundries and Market Volatility:

Intel's decision to engage with third-party foundries marks a strategic pivot that introduces new dependencies and uncertainties. The semiconductor market is notoriously cyclical, with demand fluctuations leading to excess inventory or supply shortages. Intel's reliance on foundries like TSMC and Samsung could result in a lack of control over production timelines, quality, and costs. In the event of a downturn, Intel could face substantial write-downs on inventory or unrecoverable prepayments to foundries, which in 2022 alone could account for a loss of up to $500 million based on industry averages.

Conclusion:

While Intel remains a formidable player in the semiconductor industry, the combination of intense competition, significant financial outlays for R&D and capital improvements, manufacturing and technological challenges, geopolitical and supply chain risks, and the uncertainties of third-party foundry reliance and market volatility present a compelling case for caution among investors. With these factors in mind, it may be prudent to hold off on buying Intel stock at this juncture, as the potential headwinds could weigh heavily on the company's financial performance and market valuation in the near to medium term.

Comments ()