Merck & Co., Inc. (MRK), Large Cap AI Study of the Week

The financial health of Merck & Co. is robust, as evidenced by its impressive Q3 2023 worldwide sales growth of 7%, totaling $16 billion...

December 5, 2023

Weekly AI Pick from the S&P 500

Merck & Co., Inc. (MRK)

Company Overview

Merck & Co., Inc. is a leading global healthcare company that operates mainly through its Pharmaceutical and Animal Health segments. The company focuses on producing prescription medicines, vaccines, and animal health products. In 2022, Merck generated a total of $59,283 million in sales, with the vast majority coming from its Pharmaceutical division. Key therapeutic areas include neuroscience, with products like Belsomra for insomnia; immunology, with Simponi and Remicade for inflammatory diseases in certain regions; and diabetes, with Januvia and Janumet. The Animal Health segment serves both livestock and pets, offering products such as Nuflor and Bravecto.

In recent developments, Merck has seen several product approvals, including Keytruda for various cancers, Lynparza for certain cancers, and Lagevrio for COVID-19 treatment. Despite these advances, the company faces intense competition, patent expirations, and pressures from cost containment measures by governments and third parties, which have impacted pricing and market access. The company's performance is also vulnerable to changes in healthcare legislation, particularly in the U.S. with Medicare and Medicaid, and global consolidation among healthcare providers.

Merck's global operations are significant in Europe, Japan, China, and emerging markets, with the company's growth dependent on favorable trade conditions and the absence of barriers for innovative pharmaceuticals. The company anticipates new revenue streams from innovative products addressing unmet medical needs and expansion in fast-growing markets like China. However, it must navigate pricing pressures, health technology assessments in the EU, and cost-containment globally. Merck is subject to stringent regulations by various agencies, including the FDA in the U.S. and corresponding bodies in the EU. Despite these challenges, Merck is committed to making its products accessible and affordable and engages in philanthropic efforts to improve healthcare access.

By the Numbers

Annual 10-K Report Summary:

- Total sales: $59.3 billion (22% increase from the previous year)

- GAAP Net income: $14,519 million (18% increase)

- Non-GAAP net income: $19,005 million (40% increase)

- COVID-19 treatment Lagevrio sales: $5.7 billion

- Keytruda sales: Not specified, but continued strong performance

- Gardasil/Gardasil 9 sales: 22% increase

- Pneumovax 23 sales: 33% decline

- Vaxneuvance sales: $170 million

- Januvia and Janumet sales: 15% decline

- Dividend increase: From $0.69 to $0.73 per share

- Total dividends returned in 2022: $7.0 billion

Quarterly 10-Q Report Summary:

- Worldwide sales Q3 2023: $16 billion (7% increase)

- Keytruda sales Q3: $6.338 billion (17% YoY increase)

- Keytruda sales 9 months: $18.403 billion (19% increase)

- Lynparza sales Q3: $299 million (5% increase)

- Lenvima sales Q3: $260 million (29% increase)

- Welireg sales Q3: 43% increase

- Reblozyl sales Q3: 35% increase

- Gardasil franchise Q3: 13% increase

- Gardasil franchise 9 months: 29% increase

- Prevymis sales Q3: 38% increase

- Pneumovax 23 sales Q3: Decline (specific percentage not provided)

- Isentress/Isentress HD sales Q3: Decline (specific percentage not provided)

- Januvia and Janumet sales Q3: Decline (specific percentage not provided)

- Livestock product sales Q3: Modest growth (specific percentage not provided)

- Companion animal product sales Q3: Slight decrease (specific percentage not provided)

- Cost of Sales Q3: 8% increase

- Cost of Sales 9 months: 10% decrease

- R&D expenses Q3: 25% decrease

- R&D expenses 9 months: $20.9 billion (significant increase due to acquisitions)

- Anticipated restructuring costs by end of 2023: $4.0 billion

- Restructuring charges recorded for the full year: $650 million

- Pharmaceutical segment growth Q3: 9%

- Animal Health segment decline Q3: 18%

These figures highlight Merck's financial performance, growth in key product areas, and the impact of strategic investments and market challenges.

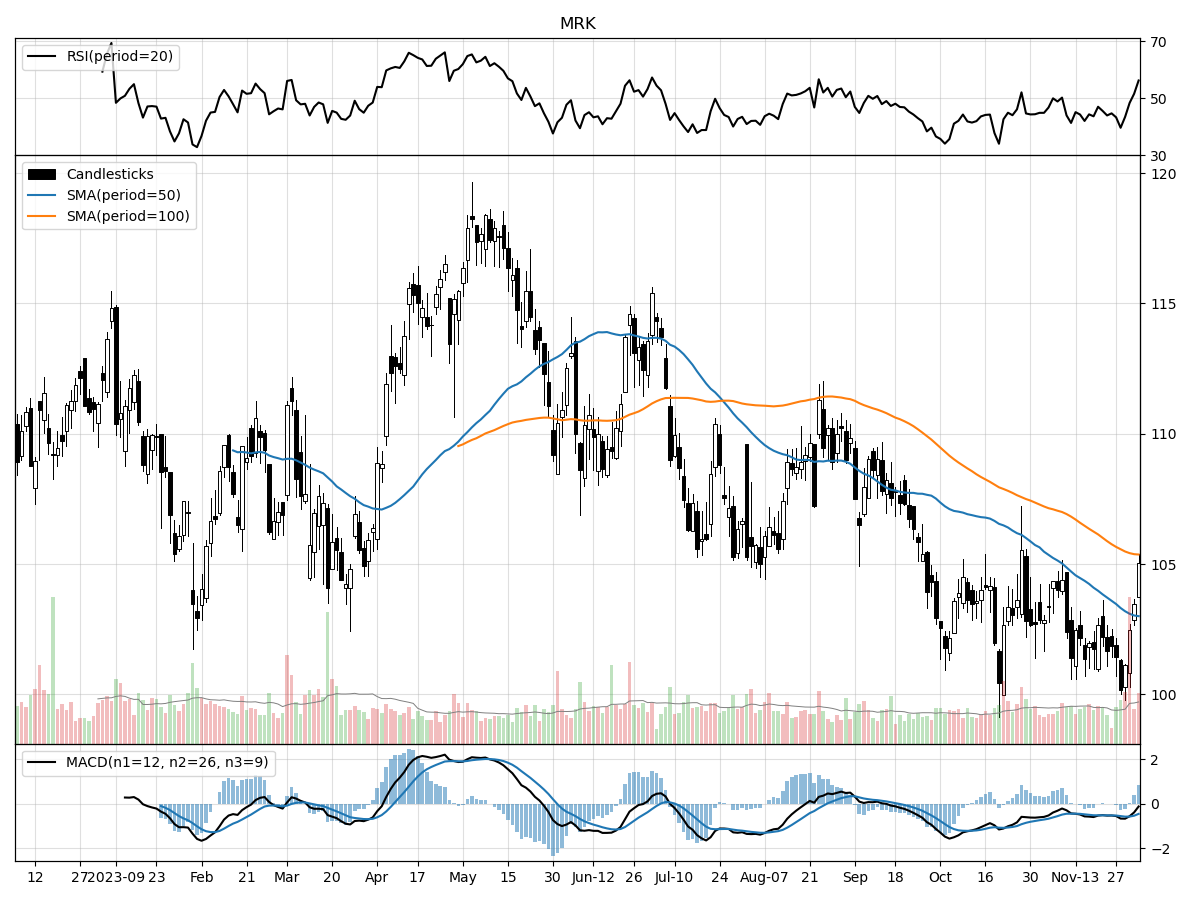

Stock Performance and Technical Analysis

The technical analysis of the stock presents a nuanced picture, with both bullish and bearish signals at play. The stock is currently trading at $105.06, which is 4% above its 52-week low and 11% below its 52-week high, suggesting that it is nearer to the lower end of its yearly range. This could be seen as an opportunity for investors who believe in the fundamental strength of the company to buy at a relatively lower price. However, caution is warranted as the stock has shown a decline of about 0.69% in the last month and 3.26% over the last three months, indicating a short-term downtrend.

Volume analysis shows recent daily trading volume is higher than the longer-term average, which could signal increased investor interest or volatility. The Money Flow indicators suggest that the stock is under heavy buying pressure and is being accumulated, which typically points to a bullish sentiment among investors. However, the Relative Strength Index (RSI) indicates that the stock is modestly overbought, suggesting that it might be nearing a point where a correction could occur as some traders may consider taking profits, leading to a short-term pullback.

The Moving Average Convergence Divergence (MACD) is bearish with a reading of -0.45, which could be interpreted as a signal that the stock's recent downward momentum is likely to continue in the near term. This bearish signal from the MACD should be considered especially when it contradicts the positive signals from the Money Flow indicators, as it may suggest underlying weakness.

In conclusion, the stock presents a mixed technical perspective. While Money Flow and volume data indicate bullish sentiment and potential accumulation, the modestly overbought condition and bearish MACD imply that there might be near-term downside risks. As a stock analyst, it would be prudent to also examine the stock's fundamentals, including earnings, growth prospects, and industry conditions, before making an investment decision. Investors should also consider their risk tolerance and investment horizon, as those with a longer-term view may be less concerned with short-term technical signals.

The ‘Bull’ Perspective

Upfront Summary:

- Strong Financial Performance: Merck's Q3 2023 worldwide sales increased by 7% to $16 billion, with Keytruda sales up 17% year-over-year.

- Strategic Acquisitions and Partnerships: The company has fortified its pipeline through strategic acquisitions, including Prometheus Biosciences ($11 billion) and collaborations like the one with Daiichi Sankyo ($4 billion upfront).

- Resilience Amid Patent Expirations: Despite the upcoming patent expiration of Januvia, Merck has a secured market exclusivity in the U.S. until May 2026, and a robust pipeline to mitigate risks.

- Global Economic and Regulatory Risks: While global economic instability and regulatory challenges pose risks, Merck's diversified portfolio and international market penetration can weather these storms.

- Pipeline and R&D Focus: With a significant increase in R&D spending ($20.9 billion over nine months), Merck is investing heavily in future growth, despite the uncertainties of research and development.

Elaboration on Key Points:

- Strong Financial Performance:

The financial health of Merck & Co. is robust, as evidenced by its impressive Q3 2023 worldwide sales growth of 7%, totaling $16 billion. This growth is not trivial; it's a testament to the company's strong product offerings, particularly Keytruda, its flagship oncology drug, which alone saw a 17% increase in sales year-over-year, reaching $6.338 billion in Q3. Over the first nine months of 2023, Keytruda's sales ballooned by 19% to $18.403 billion. This is a clear indicator that Merck's revenue streams are not only resilient but also expanding, even in the face of global economic headwinds and competitive markets. - Strategic Acquisitions and Partnerships:

Merck's proactive strategy in expanding its portfolio through acquisitions and partnerships is a forward-thinking move that secures its future market position. The $11 billion acquisition of Prometheus Biosciences and the $4 billion agreement with Daiichi Sankyo demonstrate Merck's commitment to innovation and growth. These deals are not just financial transactions; they are strategic investments in the company's future pipeline, which will bear fruit in terms of new products and market expansion. The upfront costs may be substantial, but they are investments in long-term assets that will drive future revenues. - Resilience Amid Patent Expirations:

The pharmaceutical industry is no stranger to the challenges of patent cliffs. Merck, however, has shown resilience with its market exclusivity for Januvia in the U.S. secured until May 2026. This gives the company a significant runway to manage the transition and mitigate the impact of generic competition. Furthermore, Merck's robust pipeline, which includes promising drugs and vaccines, is a strategic buffer against the revenue decline that typically accompanies patent expirations. This foresight in managing its product lifecycle ensures that Merck remains a step ahead in maintaining its revenue streams. - Global Economic and Regulatory Risks:

In an era marked by economic uncertainty and regulatory complexities, Merck's diversified portfolio positions it to navigate these challenges effectively. While the FBI's push for surveillance powers, Moody's credit outlook cut for China, and Apple's warning against India's charger rules highlight a volatile global landscape, Merck's international footprint and product diversification serve as a hedge against regional instabilities. The company's experience in managing global risks, coupled with its strategic market presence, allows it to adapt and thrive even when faced with external pressures. - Pipeline and R&D Focus:

Merck's substantial increase in R&D expenditure, totaling $20.9 billion over nine months, underscores its dedication to future growth. This investment is crucial in the pharmaceutical industry, where the development of new drugs is both costly and fraught with uncertainties. Despite these inherent risks, Merck's focus on R&D is an investment in innovation that has the potential to yield high returns. The company's pipeline is rich with potential blockbusters that can drive future revenues and offset the risks associated with R&D.

In conclusion, Merck & Co., Inc. presents a compelling investment opportunity, even in the face of global economic and regulatory challenges. The company's strong financial performance, strategic acquisitions, resilience amid patent expirations, ability to navigate global risks, and commitment to R&D and pipeline development are indicative of a forward-looking organization poised for continued success. Investors seeking a resilient and growth-oriented pharmaceutical stock need look no further than MRK.

The ‘Bear’ Perspective

Before diving into the details, let's summarize the key reasons why investors might want to avoid Merck & Co.:

- Overreliance on Key Products: Merck's financial health is heavily dependent on a few key products, such as Keytruda, which could face significant risks post-patent expiry.

- Colossal R&D Costs with Uncertain Outcomes: Recent acquisitions and collaborations have led to unprecedented R&D expenditures with uncertain returns on these investments.

- Regulatory and Pricing Pressures: Global healthcare reforms and pricing pressures are threatening to erode profit margins.

- Exposure to Global Market Risks: Geopolitical tensions and the ongoing pandemic effects could further impact Merck's operations and financial performance.

- Patent Expiry and Generic Competition: The imminent loss of patent protection for major drugs could lead to a substantial drop in revenue.

1. Overreliance on Key Products

Merck's financial success is disproportionally tied to the performance of its blockbuster drug Keytruda, which accounted for approximately 39% of its Q3 2023 sales. While Keytruda's sales have been impressive, with a 17% year-over-year increase in Q3, such heavy reliance on a single product is risky. The drug's patent is projected to expire in 2028, and Merck has yet to identify a successor with equal revenue-generating potential. Additionally, the company's vaccine franchise, namely Gardasil, experienced a 13% increase in Q3, but its growth is not sufficient to offset the potential future losses from Keytruda.

2. Colossal R&D Costs with Uncertain Outcomes

Merck has embarked on a spending spree, with R&D expenses soaring to $20.9 billion over the first nine months of 2023, largely due to its acquisitions and collaborations. While investing in R&D is essential for pharmaceutical companies, the high costs and uncertain outcomes of these investments could strain the company's finances if they do not yield profitable products. Moreover, the $4 billion upfront payment to Daiichi Sankyo and the $11 billion acquisition of Prometheus Biosciences are gambles that may not pay off, especially considering the historically low success rates of clinical drug development.

3. Regulatory and Pricing Pressures

Healthcare reforms around the world, particularly in major markets such as the EU, Japan, and China, are increasing pricing pressures on pharmaceutical companies. For instance, China's healthcare reforms have already pressured Merck's pricing power, and similar reforms could spread to other regions. In the U.S., the potential for new regulations to limit drug prices poses a significant risk to Merck's profitability, as rebates and discounts can heavily reduce gross sales.

4. Exposure to Global Market Risks

Merck's global operations expose it to various geopolitical and economic risks. The ongoing COVID-19 pandemic effects continues to affect the company's supply chains and operations. Additionally, the Russia-Ukraine conflict poses financial and operational risks, while global financial instability, particularly in emerging markets, could disrupt Merck's performance. Currency fluctuations and interest rate volatility add to these risks, with hedging strategies offering limited protection.

5. Patent Expiry and Generic Competition

The looming expiry of patents for drugs like Januvia and Janumet in the U.S. and EU is a ticking time bomb for Merck's revenue. Once these patents expire, generic competition will likely flood the market, causing a steep decline in sales. Although market exclusivity for these drugs is secure until May 2026, the anticipated loss of revenue is a clear threat on the horizon, and Merck's current pipeline may not be sufficient to fill the gap.

In conclusion, while Merck & Co., Inc. has shown growth in certain areas, the risks associated with overreliance on key products, massive R&D expenditures, regulatory and pricing pressures, global market instabilities, and patent expirations present a concerning picture for the future. Investors should carefully weigh these risks against the potential for future growth before making investment decisions in MRK.

Comments ()