Dynatrace, Inc. (DT), Mid/Small Cap AI Study of the Week

March April 4, 2024

Weekly AI Pick from the S&P 400 or S&P 600

Company Overview

Dynatrace, Inc. (DT) is a technology company that offers a comprehensive observability and security platform tailored for dynamic, hybrid, and multicloud environments. Their platform is designed to address the complexities of modern cloud-native setups, aiding organizations in their digital transformation journeys. Dynatrace's offerings include application and microservices monitoring, infrastructure monitoring, digital experience monitoring (DEM), and cloud automation, all of which are powered by their AI engine Davis and enabled by their single-agent technology, OneAgent, and data lakehouse architecture, Grail.

The company also provides advanced application security solutions, including runtime vulnerability detection and real-time threat blocking, catering to cloud-native applications. Their log management and analytics capabilities enable collaboration across IT, security, and business teams. Dynatrace's digital experience monitoring tools help improve user interactions through real user monitoring, synthetic monitoring, and session replay. Additionally, the company's digital business analytics link service performance with business outcomes, and their cloud automation services support DevOps and SRE teams in automating CI/CD processes.

Dynatrace leverages digital channels, customer training, and events for customer retention and expansion, and has a robust partner network with global system integrators, major cloud providers, resellers, and technology alliances. The company also offers professional services and education through Dynatrace University, along with innovative support services via Dynatrace ONE. Intellectual property protection is a priority, with 115 issued patents and numerous trademarks.

Competing in a market with rivals like Cisco, New Relic, and Datadog, Dynatrace emphasizes environmental, social, and governance (ESG) initiatives and values its global workforce of approximately 4,180 employees as of March 31, 2023. The company is recognized as a top employer and is committed to diversity, equity, inclusion, and belonging (DEIB), flexible work arrangements, and employee development. Dynatrace offers competitive compensation and benefits, promotes community service, and has a strong track record of employee relations without work stoppages. The company's corporate information and intellectual property are detailed, noting that website content is not part of the Annual Report.

By the Numbers

Annual Report (Fiscal Year 2023):

- Annual Recurring Revenue (ARR): $1,247 million (25% year-over-year increase)

- Total Revenue: $1,158.5 million (25% increase from the previous year)

- Subscription Revenue: Up by 24%

- Service Revenue: Up by 27%

- Net Income: $107.9 million (up from $52.4 million the previous year)

- Cash and Equivalents: Approximately $555 million

- Long-term Debt: $0

- Customer Base: Expanded from 3,300 to over 3,600

- Operating Expenses:

- Research and Development: Up by 40%

- Sales and Marketing: Up by 24%

- General and Administrative: Up by 18%

- Cash Provided by Operating Activities: $354.9 million

- Cash Used in Investing Activities: $21.5 million

- Cash Used in Financing Activities: $232.3 million

- Dollar-based Net Retention Rate: 119% or above (excluding perpetual license ARR)

Quarterly Report (Q3 2024):

- Annual Recurring Revenue (ARR): $1,425 million (23% increase from the previous year)

- Total Revenue for the Quarter: $365 million

- Subscription Revenue for the Quarter: $348 million

- Operating Margin: 10%

- Dollar-based Net Retention Rate: 113% (down from 119% year-over-year)

- Gross Margin: 81%

- Net Income for the Quarter: $42.7 million (up from $15 million the previous year)

- Total Revenue for Nine Months: $1,049.7 million (24% increase)

- Subscription Revenue for Nine Months: Up by 26%

- Cost of Subscription Revenue for Nine Months: Up by 28%

- Operating Expenses for Nine Months: Up by 23%

- Net Income for Nine Months: $116.7 million (more than fourfold increase)

- Available Credit Facility: $387.9 million

- Net Increase in Cash and Cash Equivalents for Nine Months: $227.3 million

- Cash Provided by Operating Activities for Nine Months: $246.4 million

- Cash Used in Investing Activities for Nine Months: $53.6 million

- Cash Added by Financing Activities for Nine Months: $43.7 million

These key figures highlight Dynatrace's financial performance, growth in revenue, profitability, and cash flow, as well as its strong position in terms of liquidity and absence of long-term debt. The decrease in the dollar-based net retention rate in the quarterly report may warrant further analysis to understand the underlying reasons.

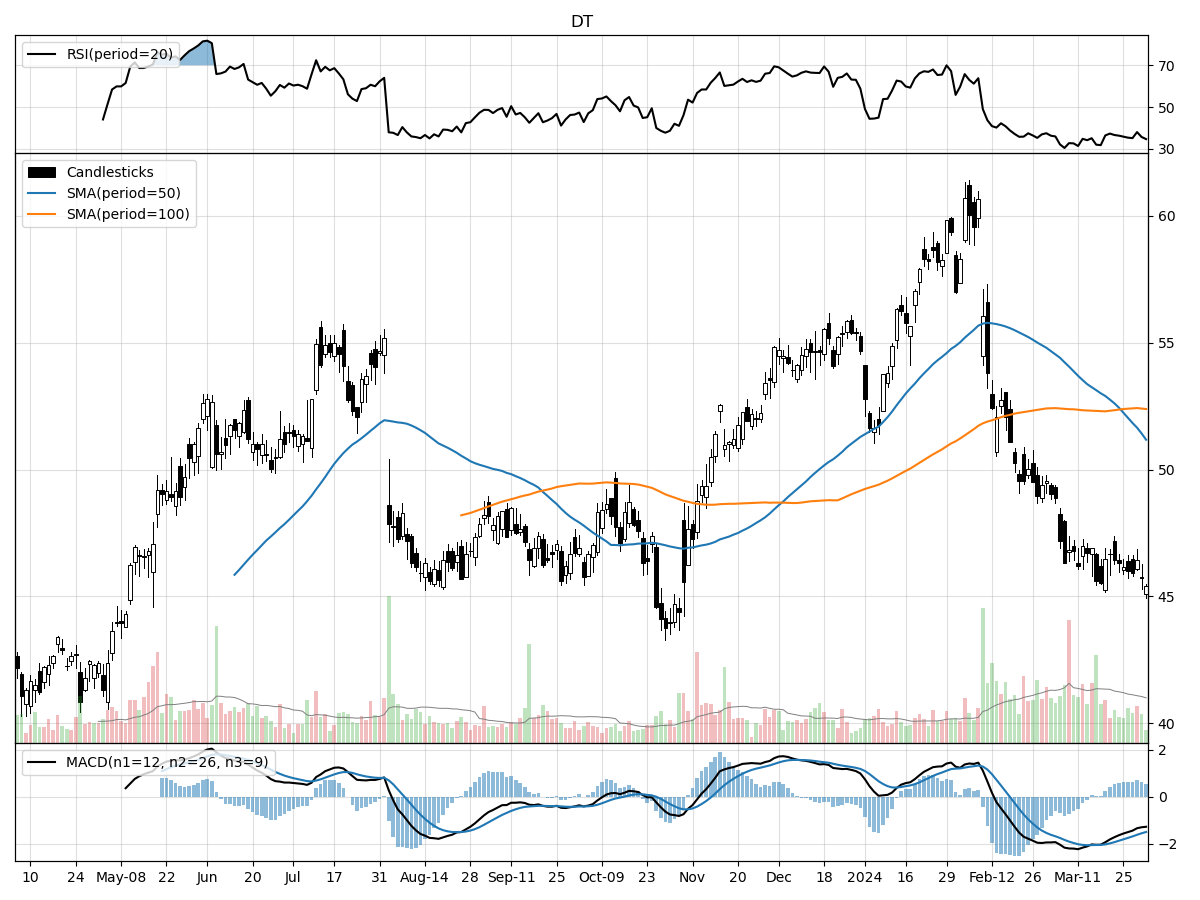

Stock Performance and Technical Analysis

Based on the current technical analysis, there are several indicators that suggest a cautious approach to investing in this stock. The stock’s price is 11 percent above its 52-week low and 25 percent below its 52-week high, indicating that the stock has experienced significant volatility over the past year. The fact that the current price is closer to the 52-week low than the high could suggest that the stock may have some upside potential if the market sentiment shifts positively. However, the price stability over the last month, coupled with a 12.22 percent decline over the last three months, reflects a lack of positive momentum that could be concerning for short-term investors.

Volume analysis shows that recent daily volume is higher than the longer-term average, indicating increased trading activity. However, the Money Flow indicators suggest that the stock is under moderate selling pressure and undergoing distribution, which means that more investors are selling the stock than buying it, potentially leading to a downward price trend.

The Moving Average Convergence Divergence (MACD) is a trend-following momentum indicator that shows the relationship between two moving averages of a stock's price. The MACD being bearish at -1.50 indicates that the short-term momentum is lower than the long-term momentum, suggesting that the stock could be in a downtrend. This is corroborated by other indicators and could be a signal for investors to wait for more bullish signals before considering an entry point.

Considering all of the above, an investor would need to evaluate their risk tolerance and investment horizon before deciding to invest in this stock. The technical indicators suggest caution, and it would be prudent to look for additional fundamental analysis or potential catalysts that could drive the stock’s price upward before making an investment decision. It's also important to monitor any changes in the technical patterns that might indicate a shift in market sentiment or stock momentum.

The ‘Bull’ Perspective

Investing in Dynatrace: A Forward-Thinking Move in the Digital Transformation Era

Upfront Summary:

- Robust Annual Recurring Revenue Growth: Dynatrace's ARR has surged to $1,425 million, marking a 23% increase year-over-year, signaling strong customer retention and product demand.

- Impressive Market Position: With a dollar-based net retention rate of 113%, Dynatrace demonstrates a solid grip on its existing customer base, despite a slight decrease from the previous year.

- Strategic R&D Investment: A 47% increase in R&D expenses indicates Dynatrace's commitment to innovation, ensuring its solutions remain competitive in a rapidly evolving market.

- Financial Resilience: The company's strategic financial adjustments and a significant increase in net income to $42.7 million for the quarter showcase a robust financial standing.

- Opportune Market Conditions: Considering the current economic backdrop and potential for a Fed rate cut, Dynatrace's business model is poised to thrive in an environment where digital transformation is key.

1. Robust Annual Recurring Revenue Growth

Dynatrace's impressive ARR growth to $1,425 million is a testament to the company's strong business model and the increasing demand for its digital performance solutions. This 23% year-over-year increase is not just a number—it reflects the company's ability to secure new customers and expand its footprint within existing accounts. In the context of the broader market trends, with businesses accelerating their digital transformation initiatives, Dynatrace's recurring revenue model provides predictable and stable cash flows, a crucial factor for investors looking for long-term growth and resilience.

2. Impressive Market Position

The company's dollar-based net retention rate, although slightly down to 113% from 119%, remains well above the 100% threshold, indicating that customers continue to spend more on Dynatrace's platform year after year. This figure is particularly significant in light of the potential economic headwinds and suggests that Dynatrace's offerings are seen as essential tools by its users. The slight dip in retention rate can be viewed in the context of broader market dynamics, where businesses are more cautious with their spending. However, Dynatrace's strong position in the market suggests it is well-equipped to navigate these challenges.

3. Strategic R&D Investment

The company's decision to ramp up R&D spending by 47% underscores its commitment to staying at the forefront of innovation. This strategic investment is critical for maintaining a competitive edge, especially considering the rapid pace of technological change in the observability and security space. With this increased R&D budget, Dynatrace is positioned to continue delivering cutting-edge solutions that meet the evolving needs of its customers, which is essential for sustaining growth in a market that's becoming increasingly crowded with competitors.

4. Financial Resilience

Dynatrace's financial health is robust, as evidenced by its significant increase in net income to $42.7 million for the quarter. This financial resilience is crucial in the current economic climate, where companies must be prepared for unexpected shifts. Dynatrace's ability to pivot strategically, as seen with the reallocation of depreciation expenses in fiscal 2023, and its strong cash flow generation, positions the company to weather potential market volatility and capitalize on growth opportunities.

5. Opportune Market Conditions

The potential for a Fed rate cut could mirror the economic conditions of the mid-'90s, which saw a historic rally in stocks. Dynatrace, operating in a sector that's integral to digital transformation, stands to benefit from such a scenario. As businesses continue to prioritize digital initiatives, Dynatrace's solutions become increasingly relevant. The company's focus on AI-driven IT operations and continuous runtime application security is particularly pertinent as organizations look to optimize their operations and protect against cyber threats in a more digital world.

Conclusion

In conclusion, Dynatrace presents a compelling investment opportunity. The company's strong ARR growth, solid market position, strategic R&D investments, financial resilience, and favorable market conditions paint a picture of a company that's not just prepared for the future but is actively shaping it. For investors seeking a dynamic player in the digital transformation space, Dynatrace is a stock to consider. With its eyes set on innovation and a clear strategy to navigate the complexities of the current economic landscape, Dynatrace is well-positioned for continued success.

The ‘Bear’ Perspective

The Case for Caution: Why Investors Should Steer Clear of Dynatrace, Inc.

Upfront Summary:

- Revenue Growth Sustainability in Question: Despite a 23% increase in annual recurring revenue, Dynatrace's declining net retention rate from 119% to 113% raises concerns about the company's ability to sustain its revenue growth.

- Economic Headwinds and Market Conditions: The current macroeconomic environment, with potential interest rate cuts, could lead to a tightening of corporate spending, adversely affecting Dynatrace's sales cycle and customer acquisition.

- Rising Operating Expenses: The 26% increase in operating expenses, particularly the 47% hike in R&D, may not translate into proportional revenue growth, impacting profitability.

- Competitive and Technological Risks: Intense competition and the need for continuous innovation in the tech sector could lead to market share erosion and pricing pressures for Dynatrace.

- Dependency on Strategic Partnerships: Dynatrace's reliance on partnerships for sales and marketing could be detrimental if these partnerships fail to deliver expected results or if partners favor competitors’ offerings.

Elaboration on Key Points:

- Revenue Growth Sustainability in Question:

Dynatrace reported a commendable 23% increase in ARR, reaching $1,425 million, with subscription revenue up by 25%. However, investors should be cautious as the company's dollar-based net retention rate has slipped from 119% to 113%. This indicates a potential weakening in the expansion of existing customer accounts, which could signal a plateau in the growth trajectory. The decline suggests that existing customers are either spending less or defecting at a higher rate than before, which could be a red flag for future revenue sustainability. Given that subscription models rely heavily on customer retention and expansion for long-term success, this metric's decline cannot be overlooked. - Economic Headwinds and Market Conditions:

The broader economic landscape, with central banks considering interest rate cuts, presents a mixed bag for companies like Dynatrace. While easier financial conditions could benefit the market as a whole, they may also lead to more cautious spending by enterprises. If corporate budgets tighten in response to economic uncertainty, Dynatrace may face extended sales cycles and challenges in acquiring new customers. This scenario is particularly relevant given the company's focus on large enterprises, which may be more sensitive to macroeconomic shifts. Furthermore, the potential for speculative bubbles, as suggested by elevated S&P 500 valuations, adds another layer of risk for investors. - Rising Operating Expenses:

Dynatrace's operating expenses have surged by 26%, with a significant 47% increase in R&D investment. While investing in innovation is critical, there is no guaranteed return on these investments, and they may not immediately result in revenue growth. Shareholders must question whether these increased expenses will lead to products that successfully capture market demand. Moreover, the need to maintain high levels of investment to stay competitive could strain future profit margins, especially if revenue growth does not keep pace with rising costs. - Competitive and Technological Risks:

The technology sector is fiercely competitive, and Dynatrace operates in a market that requires constant innovation to stay relevant. With larger companies and customer in-house solutions posing serious threats, Dynatrace could face pricing pressures and market share loss if it doesn't continuously evolve its offerings. The company's solutions must remain compatible with a rapidly changing technological landscape, and any failure to do so could lead to a significant loss of business. These risks are compounded by the company's need to control costs and successfully integrate acquisitions, which is not always a smooth process. - Dependency on Strategic Partnerships:

Dynatrace's growth strategy heavily relies on partnerships with Global System Integrators (GSIs), hyperscalers, and Independent Software Vendors (ISVs). While these relationships can be advantageous for distribution and sales, they also introduce a level of unpredictability. If these partnerships are not effectively managed or if partners choose to prioritize competitor products, Dynatrace's market presence and revenue could suffer. Additionally, the non-exclusive nature of these agreements means that there is always a risk of partners shifting their focus away from Dynatrace's offerings, which could impede the company's ability to grow its customer base and expand its market reach.

Conclusion:

Investors considering Dynatrace, Inc. must weigh the potential of the company's current performance against the backdrop of a shifting economic landscape, rising expenses, competitive pressures, and partnership dependencies. While the company has demonstrated strong revenue growth, the sustainability of this trajectory is not guaranteed. Prudent investors should be wary of the risks and consider whether Dynatrace's stock aligns with their risk tolerance and investment strategy.

Comments ()