Mosaic Company (MOS), Large Cap AI Study of the Week

The Mosaic Company is a prominent global producer and marketer of concentrated phosphate and potash crop nutrients, with operations spread across approximately 40 countries.

February 13 , 2024

Weekly AI Pick from the S&P 500

Company Overview

The Mosaic Company is a prominent global producer and marketer of concentrated phosphate and potash crop nutrients, with operations spread across approximately 40 countries. It holds a significant position in the agricultural sectors of major nutrient-consuming nations such as China, India, the U.S., and Brazil. Mosaic's business is structured into three segments: Phosphates, Potash, and Mosaic Fertilizantes, and it also engages in other operations. The company's phosphate segment is a major player, with the capacity to produce 4.5 million tonnes of phosphoric acid annually, which represents about 7% of the global market and 60% of the North American market. Its principal phosphate products include Diammonium Phosphate (DAP), Monoammonium Phosphate (MAP), and MicroEssentials®. In 2022, Mosaic produced approximately 10.5 million tonnes of phosphate rock in Florida and has plans to sustain these production levels through further development.

Mosaic is also a key player in the potash industry, with mining and processing operations in Canada and the U.S., and a significant market share in North America and globally. The company's potash products cater to various uses including crop nutrients, industrial applications, de-icing, and water softening. Despite decommissioning older shafts, Mosaic's North American potash operational capacity remains substantial. In Brazil, Mosaic is the largest phosphate producer with 2.8 million tonnes of phosphate fertilizers and 4.0 million tonnes of phosphate rock produced in 2022. It also operates the only potash mine in Brazil, further cementing its position in the market.

In terms of financial activities, Mosaic repurchased shares, increased dividends, and sold the Streamsong Resort for $160 million in 2022. The company strategically acquires inputs such as ammonia and sulfur, essential for their production processes, through various sources including internal production and long-term supply agreements. Mosaic's distribution network is extensive, with owned and leased facilities across North America, and it operates distribution businesses in India and China, with sales teams in the United States and Canada. Despite potential challenges such as the termination of a supply agreement with CF Industries Inc. for ammonia, Mosaic continues to be a dominant force in the agricultural nutrient industry.

By the Numbers

- Net sales declined by 34% for the quarter and 28% for the nine-month period.

- Net loss of $4.2 million, or $0.01 per diluted share for the quarter.

- Net income for the same period last year was $841.7 million, or $2.42 per diluted share.

- Foreign currency transaction loss increased year-over-year.

- Phosphate segment sales volumes increased; lower raw material costs.

- Potash segment experienced strong fall demand in North America.

- Approximately 4 million shares repurchased.

- Litigation related to phosphate fertilizer imports ongoing.

- Sale of Streamsong Resort resulted in a $57 million gain.

- $598 million worth of common stock repurchased.

- Special dividend paid of $0.25 per share.

- Phosphate segment's net sales decreased by 25% for the nine-month period.

- Phosphate segment's gross margin dropped from 23% to 9% year-over-year.

- Mosaic Fertilizantes' net sales for the quarter were $1.7 billion.

- Mosaic Fertilizantes' gross margin for the quarter was $106.1 million.

- Selling, general, and administrative expenses decreased by $4.6 million for the quarter.

- Selling, general, and administrative expenses increased by $12.4 million for the nine-month period.

- Other operating expenses decreased significantly year-over-year.

- Net interest expense decreased for both the three and nine-month periods.

- Foreign currency transaction loss for the quarter but a gain for the nine-month period.

- Cash and equivalents at $591.0 million.

- $606.0 million returned to shareholders through share repurchases.

- $286.5 million paid in cash dividends.

- $1.0 billion invested in capital expenditures over the nine months.

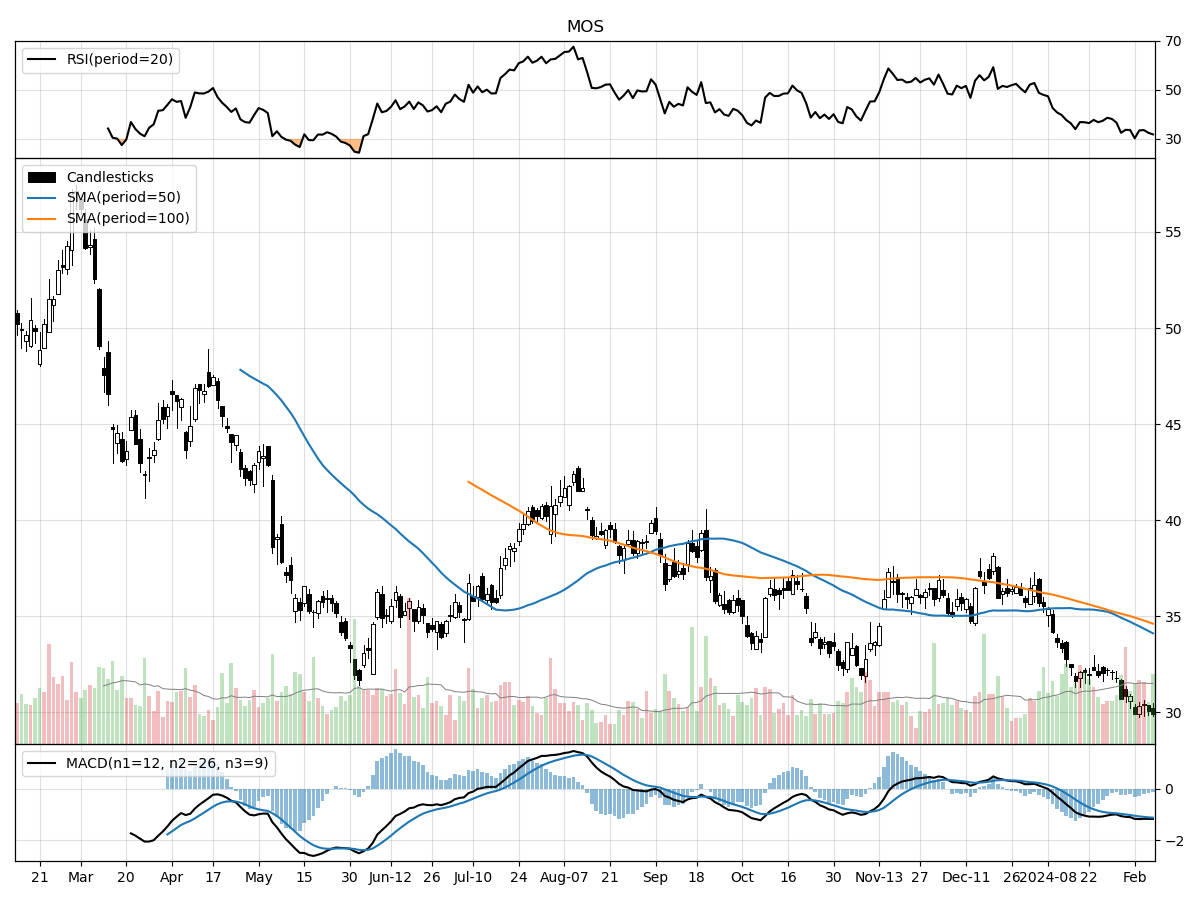

Stock Performance and Technical Analysis

The current technical analysis for the stock in question presents several red flags that may concern potential investors. Starting with the price action, the stock is trading at $29.92, which is at the same level as its 52-week low and 47% below its 52-week high. This suggests that the stock has been under significant selling pressure, potentially indicating negative sentiment or underperformance relative to the market or its sector. The recent price decline of 8.72% in the last month and 16.68% in the last three months further confirms the bearish trend that has been established over the short to medium term.

Volume is another crucial indicator in technical analysis as it can validate the price movements. The recent daily volume is higher than the longer-term average (5,072,795 shares/day vs. 4,128,416.4 shares/day), which may imply that more investors are participating in the selling, thus potentially reinforcing the current downtrend. This could be seen as a confirmation of the bearish sentiment that is driving the price lower.

Money Flow indicators provide insight into the buying and selling pressure behind price movements. In this case, the indicators signal that the stock is under moderate selling pressure and is experiencing distribution, meaning that the stock is being sold by a larger number of investors than those willing to buy. This could suggest that investors are losing confidence in the company's prospects or that there are better opportunities elsewhere.

Lastly, the Moving Average Convergence Divergence (MACD) is a momentum indicator that shows the relationship between two moving averages of a stock's price. The MACD being bearish at -1.11 indicates that the short-term momentum is lower than the long-term momentum and that the stock could continue its downtrend. This is often interpreted as a sell signal by traders.

In conclusion, the technical analysis suggests that this may not be the most opportune time to initiate a long position in the stock. Investors looking for bullish signals would typically seek a reversal in the negative trends indicated by the price action, volume, money flow, and MACD. It's always recommended to consider both technical and fundamental analysis before making investment decisions, as technical indicators alone do not provide a complete picture of a company's potential for future performance.

The ‘Bull’ Perspective

Upfront Summary:

- Robust Demand in Agriculture: The global demand for food is projected to increase by 70% by 2050, ensuring a long-term demand for fertilizers, a primary product of Mosaic.

- Strategic International Presence: Mosaic's strategic international ventures, particularly in high-growth regions like Brazil and Saudi Arabia, position it to capitalize on global agricultural needs.

- Innovative and Sustainable Practices: Mosaic is a leader in sustainable mining and fertilizer production, which is increasingly important as environmental regulations tighten.

- Financial Resilience: Despite recent setbacks, Mosaic maintains a strong balance sheet with a cash position of $591.0 million and a commitment to shareholder returns.

- Market Recovery Potential: The recent downturn in Mosaic's stock price presents a potential upside as the agricultural sector recovers and the company's strategic initiatives take effect.

Elaboration on Key Points:

- Robust Demand in Agriculture:

The world's population is growing, and with it, the demand for food is surging. By 2050, the Food and Agriculture Organization (FAO) estimates a 70% increase in food demand. As one of the leading producers of phosphate and potash fertilizers, Mosaic Co. (MOS) is well-positioned to meet this burgeoning need. Fertilizers are crucial for crop yield enhancement, and with the global trend towards higher protein diets and biofuel use, the demand for MOS's products is expected to remain robust. Despite recent price volatility, the long-term outlook for MOS is underpinned by the essential nature of its offerings in the agricultural supply chain. - Strategic International Presence:

Mosaic's international ventures, such as the Ma'aden Wa'ad Al Shamal Phosphate Company (MWSPC) in Saudi Arabia and its substantial operations in Brazil, are strategic moves to tap into high-growth markets. Brazil is one of the world's largest agricultural exporters, and with Mosaic Fertilizantes, MOS has a crucial foothold in this market. The MWSPC joint venture leverages the region's resources and provides a cost-competitive supply of phosphate fertilizers. While international operations carry risks — such as the recent social conflicts in Peru impacting supply chains — Mosaic's diversified global presence helps mitigate the impact of regional instabilities and trade policy fluctuations. - Innovative and Sustainable Practices:

Sustainability is becoming a non-negotiable aspect of modern agriculture, and MOS is at the forefront of this movement. The company's commitment to environmental stewardship is evident in its water conservation efforts and development of lower-impact mining technologies. Mosaic's ESG (Environmental, Social, and Governance) initiatives are not only ethically sound but also position the company favorably as governments worldwide impose stricter environmental regulations. This focus on sustainability can lead to operational efficiencies, cost savings, and a stronger brand reputation, all of which contribute to long-term shareholder value. - Financial Resilience:

Despite the recent downturn in its financial performance, Mosaic's balance sheet remains robust. With $591.0 million in cash and cash equivalents, MOS is in a strong position to weather market volatility. Moreover, the company's commitment to returning value to shareholders is evident through its share repurchase program and special dividends. While the company faces risks such as increased costs for raw materials and potential supply chain disruptions, its financial prudence and strategic investments in cost-effective production and distribution capabilities provide a buffer against these challenges. - Market Recovery Potential:

The recent decline in Mosaic's stock price may be seen as a buying opportunity for long-term investors. As the agricultural sector navigates through current headwinds, Mosaic's strategic initiatives — including expanding its market reach and improving operational efficiency — are expected to yield results. The company's focus on innovation and sustainability, coupled with the essential nature of its products, suggests that MOS is poised for a recovery as market conditions stabilize. Additionally, the potential for easing trade tensions and the normalization of supply chains could serve as catalysts for growth in the company's stock value.

Conclusion:

Mosaic Co. (MOS) presents a compelling investment case, combining essential products with a strategic global presence and a commitment to innovation and sustainability. While the company faces headwinds from market volatility and risks inherent to its industry, its strong financial foundation and long-term growth prospects in the face of an ever-growing demand for agricultural products make MOS a stock to consider for investors with a long-term horizon. As with any investment, it is essential to consider the company's potential risks alongside its opportunities; however, for those with a bullish outlook on the agricultural sector, Mosaic offers a resilient option.

The ‘Bear’ Perspective

Upfront Summary:

- Declining Sales and Earnings: Mosaic Co. reported a significant 34% decline in net sales for the quarter and a net loss of $4.2 million, a stark contrast to the prior year's net income of $841.7 million.

- Challenges in Phosphate and Potash Segments: The Phosphate segment's net sales decreased by 25%, with a drop in gross margin from 23% to 9%, while the Potash segment faced lower average selling prices and increased operational costs.

- International Risks and Operational Hurdles: International market factors, trade policies, and operational risks such as increased transportation costs and inflation present ongoing challenges for Mosaic Co.

- Regulatory and Environmental Pressures: Mosaic Co. is subject to stringent environmental regulations, with risks of legal action and the need for capital improvements, which could further strain financial resources.

- Market Volatility and Interest Rate Risks: The company's risk management strategies may not effectively mitigate exposure to price fluctuations, and interest rate risks could impact profitability.

Elaboration on Points:

- Declining Sales and Earnings:

The most recent financials from Mosaic Co. paint a concerning picture for potential investors. The 34% plummet in net sales for the quarter is a red flag, indicating a severe downturn in the company's core business. The transition from a robust net income of $841.7 million to a net loss of $4.2 million year-over-year is not a mere hiccup but a significant reversal of fortune. This drastic shift could be indicative of systemic issues within the company or sector, and the $0.01 loss per diluted share signals potential troubles ahead. With the agricultural sector's notorious volatility, investors should be wary of assuming a quick recovery without substantive evidence. - Challenges in Phosphate and Potash Segments:

The numbers within Mosaic Co.'s Phosphate and Potash segments are particularly concerning. A 25% decrease in net sales for the Phosphate segment, coupled with a gross margin collapse from 23% to 9%, suggests a severe pricing pressure that is not fully offset by the reduction in the cost of goods sold. Meanwhile, the Potash segment is not faring much better, grappling with its own set of challenges, including lower average selling prices and increased costs due to idle plant and maintenance. These segments are critical to Mosaic's overall performance, and their struggles could be indicative of deeper issues within the company or the industry at large. - International Risks and Operational Hurdles:

Mosaic Co.'s international exposure adds layers of complexity to its operations. U.S. trade policies and countervailing duties against phosphate fertilizer imports directly impact the company's bottom line. Moreover, operational risks such as rising transportation costs and inflationary pressures can compress margins further. With a substantial portion of its business hinging on international markets, currency fluctuations, and global economic stability, the company's financial health remains at the mercy of factors beyond its control. For example, social conflicts in regions like Peru could disrupt supply chains, while the Russia-Ukraine conflict has already heightened energy cost volatility. - Regulatory and Environmental Pressures:

Environmental compliance is a significant concern for Mosaic Co., as non-compliance could lead to costly legal action and demands for new capital investments. Regulatory initiatives aimed at reducing greenhouse gas emissions could also increase operating costs. The need to navigate and adapt to these regulations requires significant resources, and any missteps could result in punitive damages that would further stress the company's financials. In an era where environmental stewardship is becoming increasingly critical, the potential for these pressures to intensify is high. - Market Volatility and Interest Rate Risks:

The agricultural sector is inherently subject to market volatility, and Mosaic Co.'s risk management strategies may not be sufficient to mitigate such exposure. Price fluctuations in key commodities like natural gas, ammonia, sulfur, and energy pose a risk to profitability. Additionally, the company's financial instruments are vulnerable to interest rate risks, which could impact earnings and cash flows. With the Federal Reserve's recent aggressive rate hikes, the financial landscape is changing rapidly, and companies like Mosaic Co. must navigate these waters with caution to avoid adverse impacts on their balance sheets.

In conclusion, while Mosaic Co. has demonstrated resilience in the past, the confluence of declining sales, segment challenges, international risks, regulatory pressures, and market volatility create a precarious situation for the company. Investors should carefully consider these factors and exercise due diligence before making any investment decisions regarding Mosaic Co. As we look ahead, it is prudent to adopt a bearish stance until the company shows tangible signs of overcoming these hurdles and returning to a path of sustainable growth and profitability.

Comments ()