Patterson Companies, Inc. (PDCO), Mid/Small Cap AI Study of the Week

January 4, 2024

Weekly AI Pick from the S&P 400 or S&P 600

Patterson Companies, Inc. (PDCO)

Company Overview

Patterson Companies, Inc. (PDCO) operates as a distributor in the dental and animal health supply markets in North America and the UK through two main segments: Patterson Dental and Patterson Animal Health. The company has been in the dental supply business since 1877 and has grown to become one of North America's largest distributors, providing a range of products and services to dental practices. Patterson Dental's sales are mainly from consumables and equipment, with a focus on enhancing dental practice efficiency. Patterson Animal Health serves a diverse customer base in the animal health market, offering products such as pharmaceuticals and equipment, with consumables making up the majority of sales. PDCO competes by offering premium customer service, a skilled salesforce, strategic logistics, and competitive pricing.

PDCO's business strategy includes growth through internal expansion, acquisitions, and technology, with online platforms playing a significant role in order placement and customer service. The company uses direct marketing tools, including loyalty programs and social media, to reach customers and emphasizes rapid delivery from fulfillment centers. Patterson faced challenges during the COVID-19 pandemic, including supply chain disruptions and margin impacts due to PPE pricing volatility. Seasonal patterns and regulatory changes can affect quarterly results, and the company must comply with various regulations regarding pharmaceutical and medical device distribution.

The regulatory environment for PDCO is complex, with animal-health pharmaceuticals requiring FDA approval in the U.S. and veterinary biologics overseen by the USDA. Controlled substances are strictly regulated by the DEA, and the FTC monitors advertising practices for animal-health products. Internationally, Brexit has led to distinct regulations in the U.K., and the U.S. has federal laws like the FDC Act and Controlled Substances Act that govern pharmaceutical and medical device regulations. Changes such as the DSCSA are being implemented to improve pharmaceutical supply chain tracking. Compliance with these regulations is crucial for PDCO to avoid sanctions and legal consequences.

By the Numbers

Annual 10-K Report Summary:

- Net sales: $6,471.5 million (0.4% decrease from the previous year)

- Dental segment sales: Decreased by 1.0%

- Animal Health segment sales: Decreased by 0.5%

- Gross profit margin: Improved to 21.2%

- Operating income: Increased to 4.3% of net sales

- Net income: Rose to $207.6 million ($2.12 per diluted share) from $203.2 million ($2.06 per diluted share)

- Net cash used in operating activities: $754.9 million

- Cash provided by investing activities: $901.6 million

- Cash used in financing activities: $126.5 million

- Debt load: $298.5 million under a term loan and $45.0 million under a revolving credit facility

- Share repurchase program: Authorized up to $500 million (with $409.5 million still available)

- Cash and cash equivalents: $159.7 million

- Total contractual obligations: $708.9 million (due over the next five years)

- Gross liabilities for uncertain tax positions: $9.9 million

- Days sales outstanding (DSO): Slight improvement

- Inventory turnover: Marginal decrease

Quarterly 10-Q Report Summary:

- Net sales for the quarter: $1,652.8 million (1.6% increase)

- Animal Health segment sales growth: 2.2%

- Dental segment sales decline: 0.4%

- Operating income for the quarter: $56.9 million (3.4% of net sales, down from 3.7%)

- Gross profit margin for the quarter: Improved to 20.5%

- Effective tax rate for the quarter: Increased slightly to 25.3%

- Net income for the quarter: Decreased to $40.0 million ($0.42 per diluted share) from $54.1 million ($0.55 per diluted share)

- Net sales over six months: Increased by 2.5% to $3,229.5 million

- Gross profit margin rate over six months: Improved slightly to 20.4%

- Operating expenses over six months: Grew by 3.2%

- Dental segment operating income over six months: Decreased by $3.9 million to $93.9 million

- Animal Health segment operating income over six months: Increased by $5.9 million to $56.0 million

- Corporate segment losses over six months: Expanded to $54.9 million

- Net income attributable to PDCO over six months: Fell to $71.2 million (earnings per share decreased from $0.81 to $0.74)

- Cash used in operating activities over six months: $485.3 million

- Outstanding amounts on credit facilities: Significant, with extended maturity to October 2027

These figures highlight the company's financial performance, liquidity position, and capital management over the reported periods.

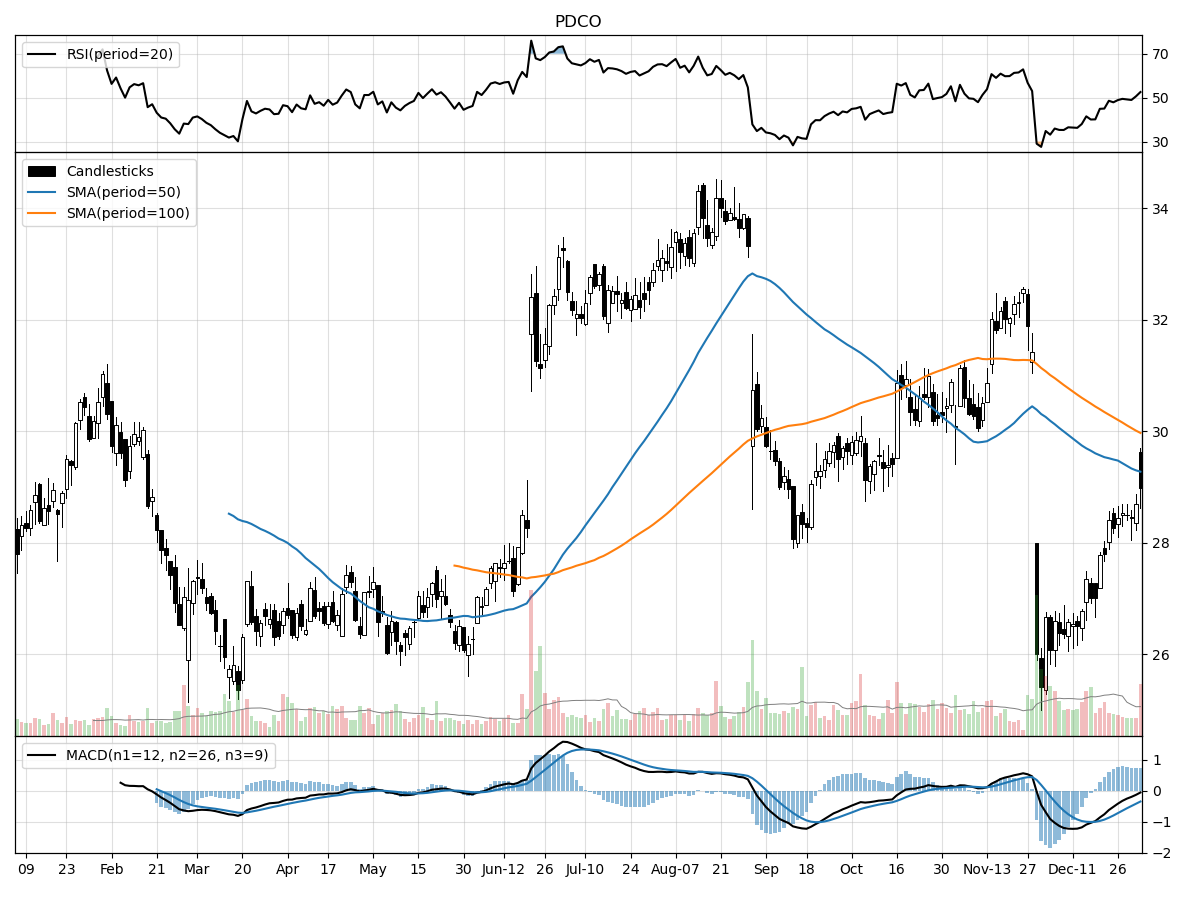

Stock Performance and Technical Analysis

Given the technical factors at play, it appears that there is a complex narrative surrounding the stock in question. The current stock price of $28.99 is positioned in a relatively moderate zone within its 52-week range, sitting 14% above its low and 15% below its high. This suggests that while the stock has seen better days, it hasn't sunk too close to its lowest valuation over the past year, indicating that there may still be investor confidence or at least a floor of support.

The recent rise in price by 9% over the past month signifies a positive short-term momentum, which could be reflective of improving company fundamentals, market sentiment, or other external factors driving interest in the stock. However, this upward trend isn't reflected over the last three months, where the price has shown stability rather than growth. This stability in the face of recent gains suggests that the stock may be consolidating at this price level before making a more definitive move in either direction.

Looking at the volume, the daily trading volume is higher than the longer-term average, suggesting increased investor interest and potentially liquidity in the market for this stock. The Money Flow indicators point to heavy buying pressure, complemented by the stock being under accumulation, which typically indicates that investors are accumulating shares and could be a bullish signal. However, the Moving Average Convergence Divergence (MACD) is bearish, with a value of -0.34, which implies that the stock could be losing momentum or that a bearish reversal could be imminent. This divergence between the Money Flow and MACD could suggest that investors should proceed with caution, as the market is receiving mixed signals. The Relative Strength Index (RSI) indicates that the stock is neither overbought nor oversold, which provides little guidance on whether the stock is currently undervalued or overvalued based on recent trading.

In conclusion, the technical analysis presents a stock that is in a potential accumulation phase with positive short-term momentum but also shows signs of caution with a bearish MACD signal. Investors would benefit from closely monitoring upcoming financial results, news, and broader market conditions before making an investment decision, as these factors could significantly impact the stock's future price movements.

The ‘Bull’ Perspective

Title: Patterson Companies, Inc. (PDCO): A Strong Buy Amidst a Resilient Market

Summary:

- Robust Financial Performance: PDCO demonstrated a solid increase in net sales with a 1.6% rise to $1,652.8 million in the latest quarter, signaling strong operational execution.

- Strategic Position in Growing Markets: The Animal Health segment showed a 2.2% growth, indicating PDCO's strong position in a market with expanding demand.

- Proactive Inflation and Interest Rate Management: The company has effectively navigated cost inflation and rising interest rates, maintaining financial flexibility and adjusting prices to offset increased costs.

- Diversified Business Segments Mitigate Risk: PDCO's diversified portfolio across Dental and Animal Health segments reduces dependency on a single market, providing stability against sector-specific downturns.

- Positive Economic Tailwinds: With 2023 ending on a high note across asset classes and the easing of inflation, PDCO is well-positioned to benefit from the broader economic recovery.

Elaboration:

- Robust Financial Performance:

Patterson Companies, Inc. has proven its ability to generate revenue growth in a challenging economic environment. The latest quarterly report shows a 1.6% increase in net sales, amounting to $1,652.8 million. This growth is particularly commendable considering the broader economic headwinds, including the highest borrowing costs in more than two decades. PDCO's gross profit margin improvement to 20.5% is a testament to its pricing power and operational efficiency, which are crucial in an inflationary period. Despite a slight decrease in net income attributable to PDCO, the company's ability to maintain a positive trajectory in sales is a bullish indicator for investors. - Strategic Position in Growing Markets:

The Animal Health segment of PDCO is experiencing robust growth, with a 2.2% increase in sales. This segment caters to a market with a consistent demand trajectory, as pet ownership and livestock management remain critical components of consumer spending and the agricultural economy. The growth in this segment suggests that PDCO is well-positioned to capture the expanding opportunities in the animal health market, which is less sensitive to economic fluctuations compared to other sectors. - Proactive Inflation and Interest Rate Management:

PDCO's management has taken proactive steps to combat the challenges posed by inflation and rising interest rates, which have been significant concerns for investors. By implementing price increases and maintaining financial flexibility through credit facilities, PDCO has shown resilience in preserving its bottom line. The Receivables Securitization Program with MUFG provides additional liquidity, ensuring that the company can navigate the financial landscape effectively. - Diversified Business Segments Mitigate Risk:

Diversification is a key strength for PDCO, with its presence in both the Dental and Animal Health markets. This strategic positioning allows the company to mitigate risks associated with any single market, providing a buffer against sector-specific downturns. For instance, while the Dental segment saw a minor decline of 0.4%, the Animal Health segment's growth helped offset this, showcasing the benefits of a diversified business model. - Positive Economic Tailwinds:

As 2023 ended with strong performance across most investment asset classes and a trend of disinflation, PDCO stands to gain from the positive economic tailwinds. The easing of inflation, particularly with the CPI cutting by two-thirds since its peak, suggests a more favorable environment for consumer spending. With the end of Fed tightening and excitement around AI, sectors like Animal Health, which can benefit from technological advancements, are poised for growth. PDCO's diversified offerings align well with these trends, potentially driving further growth and profitability.

Conclusion:

In summary, Patterson Companies, Inc. presents a compelling investment opportunity. Its financial resilience, strategic market positioning, proactive management of economic pressures, diversified business operations, and alignment with positive economic trends underscore its potential for continued success. As we look ahead, PDCO is poised to leverage these strengths, making it a strong buy for investors seeking a robust and forward-looking addition to their portfolios.

The ‘Bear’ Perspective

Why Investors Should Steer Clear of Patterson Companies, Inc. (PDCO)

- Subpar Performance in Key Segments: PDCO's Dental segment, a significant portion of its business, showed a decline in operating income by $3.9 million, despite an increase in sales and gross profit margin.

- Rising Operating Expenses: The company's operating expenses have risen by 3.2%, outpacing sales growth and contributing to a lower operating income of $56.9 million, down from $60.1 million year over year.

- Vulnerability to Market and Economic Conditions: Given the recent regional bank crisis and heightened geopolitical uncertainty, PDCO's financial performance could be adversely affected by economic downturns, especially with its substantial amounts outstanding on credit facilities.

- Increased Competition and Technological Disruption: With the rise of e-commerce and direct manufacturer sales, PDCO faces significant competitive threats that can erode market share and margins.

- Regulatory and Cybersecurity Risks: Compliance with ever-changing regulations and the need to secure sensitive data against cyber threats add operational complexity and potential costs, impacting the bottom line.

Detailed Analysis:

- Subpar Performance in Key Segments

Patterson Companies, Inc. reported a disconcerting decrease in operating income for their Dental segment, which fell by $3.9 million to $93.9 million. This decline occurred despite a reported increase in sales and gross profit margin, suggesting that there are underlying inefficiencies or market pressures that are eroding profitability. With the Dental segment being a vital part of PDCO's business, accounting for a substantial part of its revenue, this downturn is a red flag for investors. The segment's vulnerability to economic cycles and consumer spending habits, particularly in elective dental procedures, casts doubt on its future performance, especially in an environment where discretionary healthcare spending is under pressure. - Rising Operating Expenses

Patterson Companies, Inc.'s operating expenses have been on an upward trajectory, increasing by 3.2% and contributing to a decrease in operating income. This rise in expenses, which includes costs related to sales, general administrative activities, and potentially increased shipping costs due to third-party distribution challenges, is a concern. When operating expenses grow faster than revenue, it squeezes margins and can signal inefficiencies within the company's operations. Given that the operating expense ratio has also seen a slight rise, investors should be cautious about the company's cost management and its impact on profitability. - Vulnerability to Market and Economic Conditions

The recent bank crisis, which saw the collapse of several regional banks, and the ongoing geopolitical tensions could have ripple effects on companies like PDCO. With significant amounts outstanding on both their term loan and revolving credit facility, PDCO could face increased financial strain if the economic environment worsens or if interest rates continue to rise. The company's financial flexibility is further constrained by restrictive covenants in its credit agreements, which could limit its ability to respond to adverse market conditions. Given the uncertain economic outlook for 2024, PDCO's financial health could be at risk, making it a less attractive option for investors. - Increased Competition and Technological Disruption

The competitive landscape for Patterson Companies is intensifying, with e-commerce platforms and direct sales by manufacturers threatening traditional distribution channels. This shift is particularly impactful in the dental and animal health markets, where customers are increasingly seeking cost-effective and convenient alternatives. PDCO's reliance on supplier rebates and incentives is also a concern, as it may not be sustainable in the long term. With the rapid pace of technological change, there is also the risk of product obsolescence, which could lead to inventory write-offs and a loss of competitive edge. These factors combined suggest that PDCO may struggle to maintain its market position and profitability. - Regulatory and Cybersecurity Risks

PDCO operates in an industry that is heavily regulated and subject to significant changes in law and policy. Compliance with these regulations is costly and time-consuming, and any failure to comply could result in substantial fines and damage to the company's reputation. Moreover, the threat of cyberattacks is ever-present, and a breach could have severe consequences, including financial loss, legal liability, and erosion of customer trust. With PDCO's acknowledgment of these risks in their reports, investors should be aware of the potential for unexpected costs and disruptions that could impact the company's financial results.

In conclusion, while Patterson Companies, Inc. has shown resilience in the face of economic challenges, the combination of declining segment performance, rising expenses, economic vulnerability, increased competition, and regulatory risks presents a compelling case for investors to exercise caution. Given the current market conditions and the company's specific challenges, it may be prudent to avoid buying PDCO shares, sell existing holdings, or hold off on shorting until the company demonstrates a more robust strategy for growth and risk management.

Comments ()