The Monday Charge: December 18, 2023

The Federal Reserve's latest meeting minutes have provided a glimmer of hope for investors, signaling a potential slowdown in the aggressive rate hike cycle that has defined much of 2023.

AI stock picks for the week (Large Cap S&P 500)

- Mailed to FREE newsletter subscribers (Covered on Tuesday)

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

(Based on a three month forward looking window)

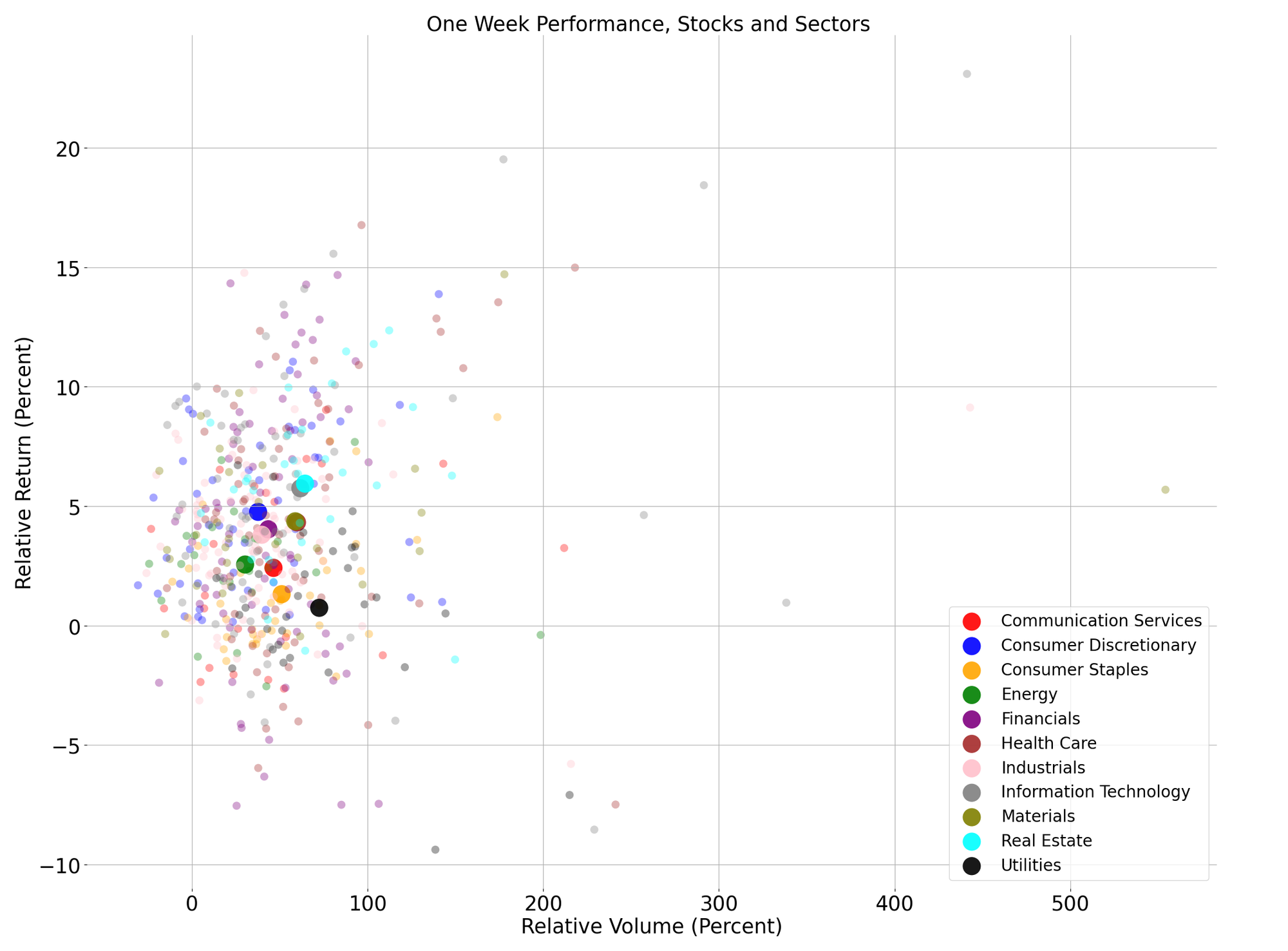

The biggest movers last week on price and volume (Large Cap S&P 500)

Price and volume moves last week for every stock and sector (Large Cap S&P 500)

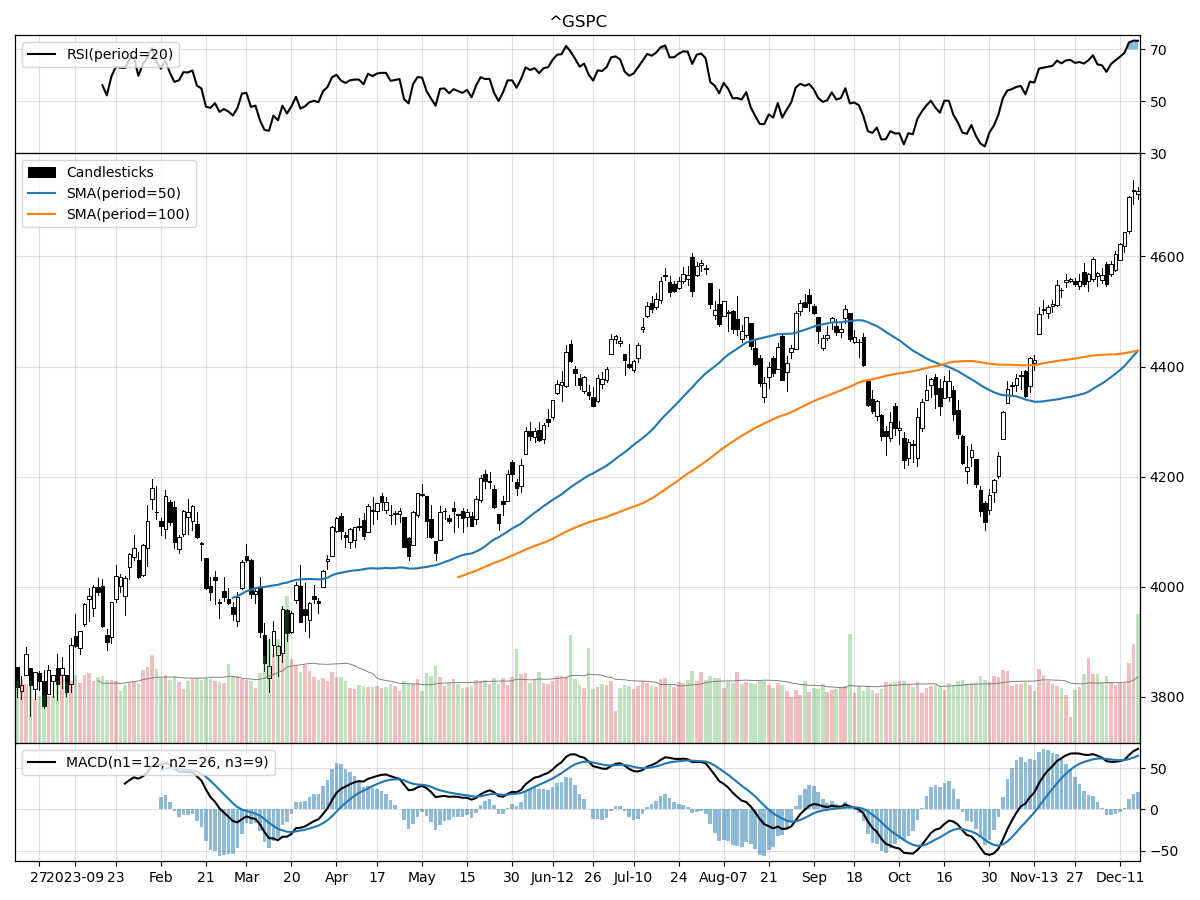

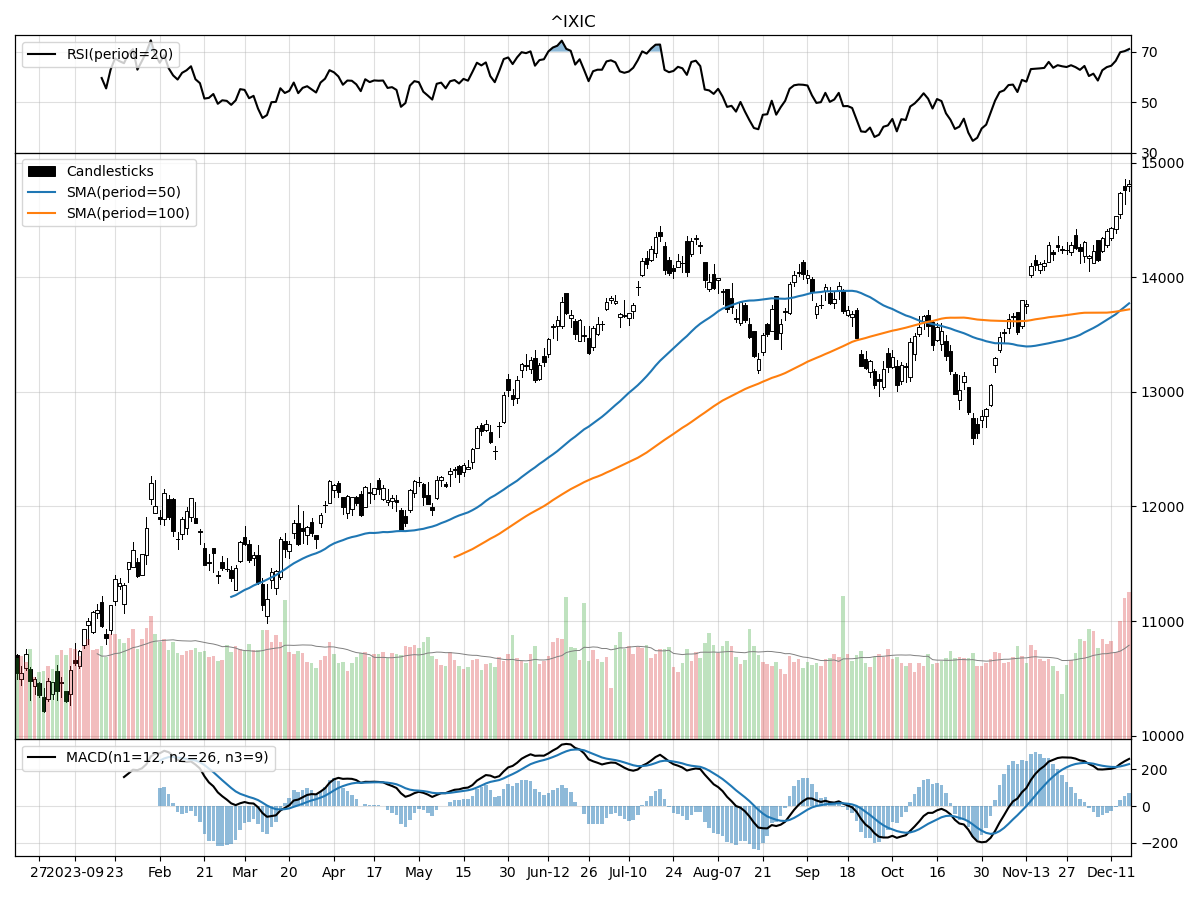

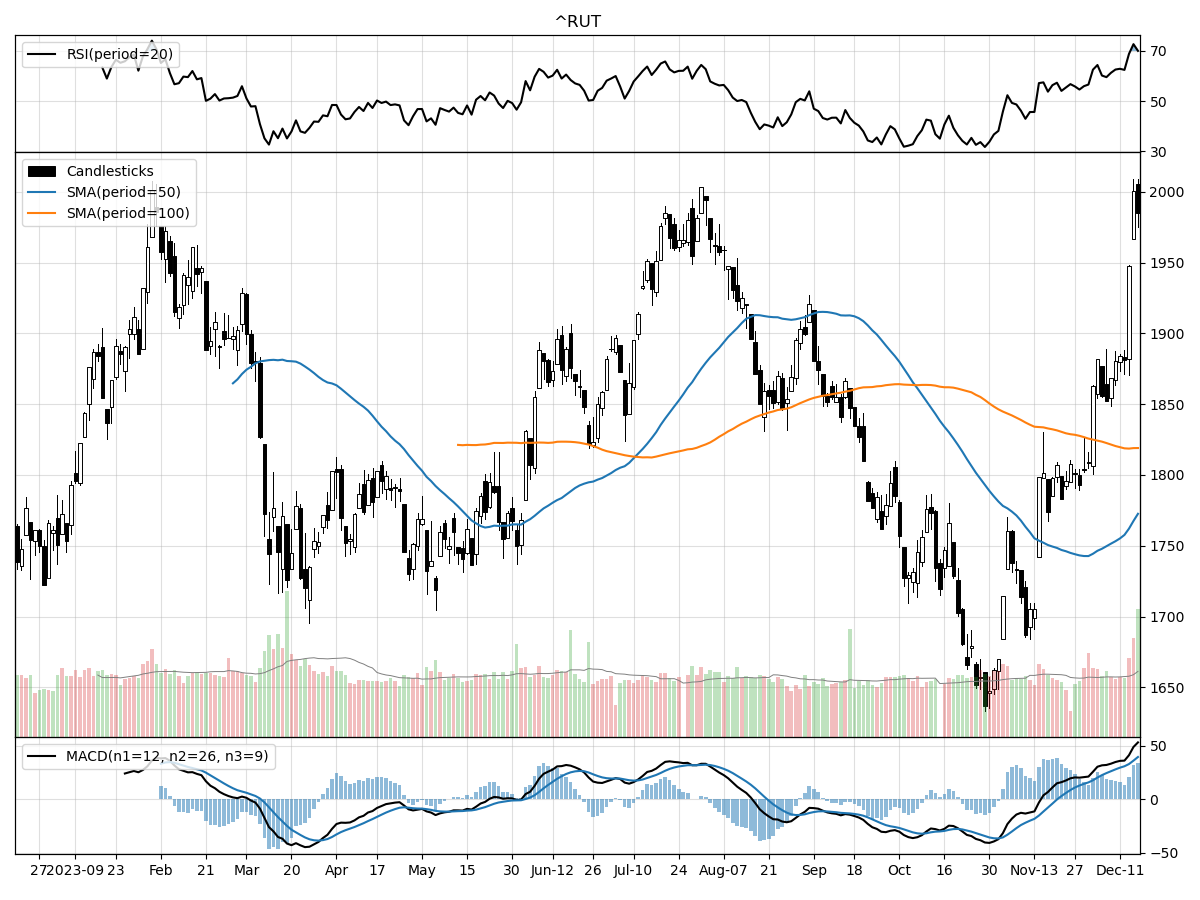

A technical analysis across indices

S&P500

Nasdaq

Russell 2000

The S&P 500, Nasdaq, and Russell 2000 Small Cap indices are all exhibiting strong technical performance with each index having risen considerably over the past three months, indicating a bullish trend in the broader market. The S&P 500 has seen a 9.24% increase, while the Nasdaq has jumped 12.13%, and the Russell 2000 has climbed 11.74%. These gains suggest investor confidence and a potential recovery from any previous dips or market corrections. The Nasdaq's notable outperformance may reflect a stronger appetite for technology and growth stocks, which typically have a larger representation in this index. Conversely, the Russell 2000's significant rise could signal a growing interest in small-cap stocks, which may benefit from a domestic economic recovery and are often viewed as more sensitive to changes in the economic outlook.

Volume trends across all three indices show recent daily volumes are higher than their respective longer-term averages, with the Nasdaq experiencing the most significant increase in trading activity. This could indicate a heightened level of investor engagement and potentially more liquidity in the market. Higher volumes in conjunction with price increases may also reinforce the current uptrend's strength.

Despite these positive trends, the Relative Strength Index (RSI) readings suggest that all three indices are currently overbought. This could foreshadow a potential pullback or consolidation period as investors may take profits after the recent run-ups. Additionally, while the Money Flow indicators point to moderate to heavy buying pressure and accumulation across the indices, this buying momentum might slow down if the markets reach a point of saturation or if investors become cautious at these higher price levels. The Moving Average Convergence Divergence (MACD) being bullish for all three indices corroborates the current upward momentum, but investors should remain vigilant for any signs of a trend reversal, especially given the overbought conditions.

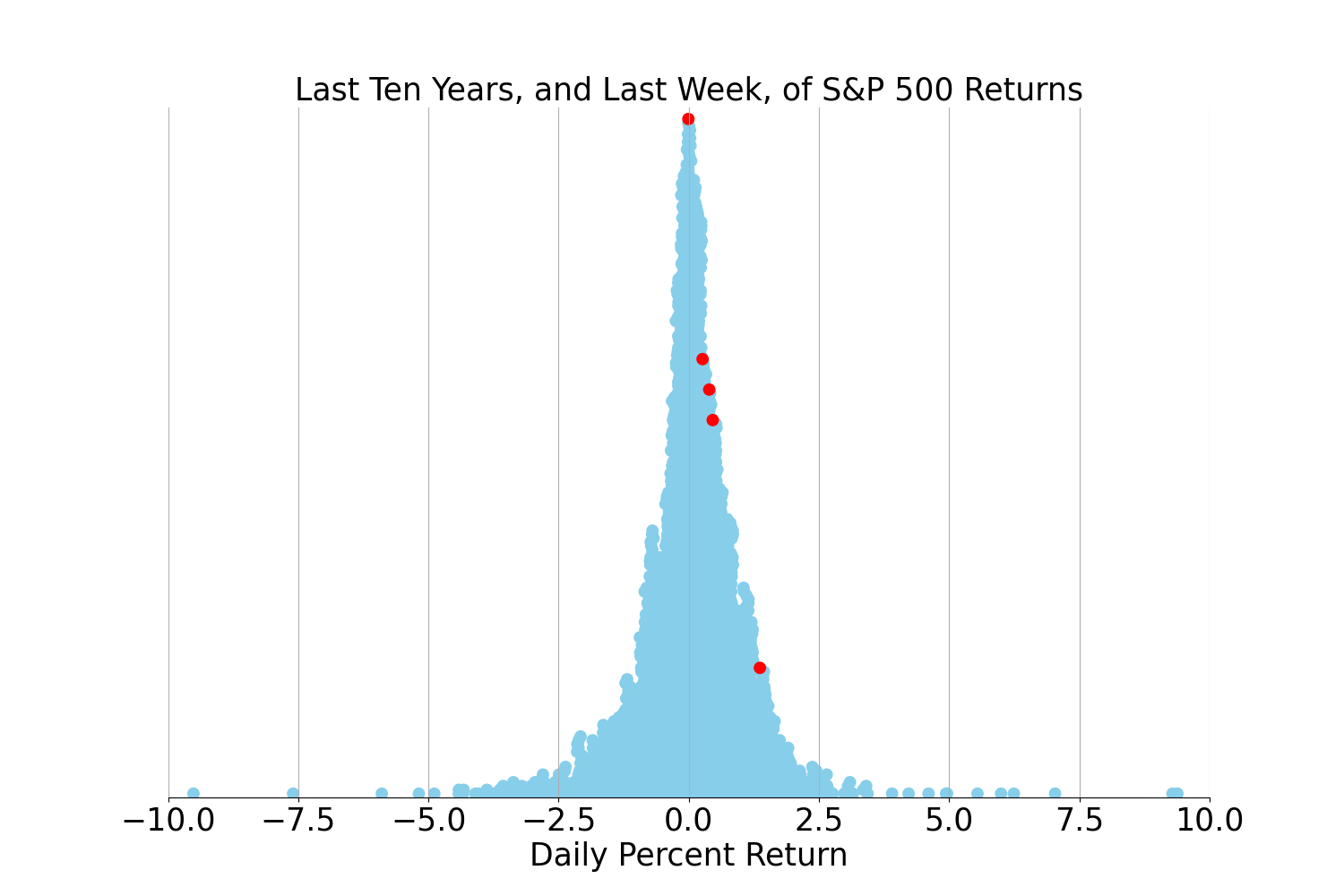

Last week vs. history (Large Cap S&P 500)

Market Commentary

Title: Market Momentum Meets Monetary Policy: Shifting Winds in the Financial Landscape

As we approach the final stretch of the fiscal year, the financial markets have been riding a wave of cautious optimism, fueled by recent developments in monetary policy and economic indicators. The Federal Reserve's latest meeting minutes have provided a glimmer of hope for investors, signaling a potential slowdown in the aggressive rate hike cycle that has defined much of 2023. This dovish tilt has sent ripples through the stock market, with the S&P 500 responding positively, climbing over 2% in the aftermath.

The Fed's shift in stance comes on the back of easing inflationary pressures, as recent data suggests a cooling in the once red-hot consumer price index. This deceleration has granted policymakers the latitude to consider a more measured approach to interest rates, a move that has been met with a collective sigh of relief from Wall Street to Main Street. The prospect of a less restrictive monetary environment has rekindled investor interest in equities, particularly in sectors sensitive to interest rate fluctuations such as real estate and technology.

However, the road ahead is not without its potholes. The unemployment rate, while still hovering near historic lows, is projected by the Fed to tick upwards to 4.1% by 2024. This anticipated uptick serves as a reminder of the delicate balance the central bank must maintain between curbing inflation and fostering employment. The job market's resilience will be a critical factor in determining the trajectory of economic growth and, by extension, stock market performance.

Amidst this backdrop, bond markets have also seen a noteworthy shift. The benchmark 10-year Treasury yield has retreated significantly from its mid-October peak, dipping below the psychological threshold of 4%. This decline in yields points to a recalibration of investor expectations, with many now anticipating rate cuts rather than hikes in the not-too-distant future. The bond market's movements are often a harbinger for equities, suggesting that the appetite for risk may be on the rise as investors search for yield.

The performance of the markets has also underscored a broadening of leadership, with small-cap stocks outshining their large-cap counterparts in recent weeks. The Russell 2000 index, a barometer for small-cap performance, has surged nearly 11% over the past month, eclipsing the gains of the tech-heavy Nasdaq and the blue-chip Dow Jones Industrial Average. This shift suggests a growing confidence in the economic underpinnings of smaller companies, which are typically more sensitive to domestic economic shifts.

Looking ahead, investors are bracing for a suite of economic data releases, including the Personal Consumption Expenditures (PCE) index, a preferred gauge of inflation for the Fed, and home sales figures. These data points will offer further clarity on the state of the economy and could either fuel the current market rally or dampen the spirits of investors banking on a soft landing.

In conclusion, the financial markets are at a crossroads, with the specter of rate cuts looming on the horizon. While the recent rally in stocks and bonds may continue as we head into the holiday season, investors would be wise to remain vigilant. The potential for volatility persists, particularly as we navigate the uncertainty of a shifting monetary landscape and the ongoing recalibration of the global economy. As always, a prudent approach to investment, one that balances risk and reward, will be paramount as we chart a course through these turbulent financial waters.

Comments ()