The Monday Charge: February 5, 2024

...The Fed, under Chairman Jerome Powell's guidance, signaled a willingness to maintain current interest rates while closely monitoring inflation trends, suggesting that rate cuts are on the horizon

This is our Monday article, focusing on the large cap S&P 500 index. Just the information you need to start your investing week. As always, 100% generated by AI and Data Science, informed, objective, unbiased, and data-driven.

AI stock picks for the week (Large Cap S&P 500)

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers (Covered on Tuesday)

- Mailed to FREE newsletter subscribers

(Based on a three month forward looking window)

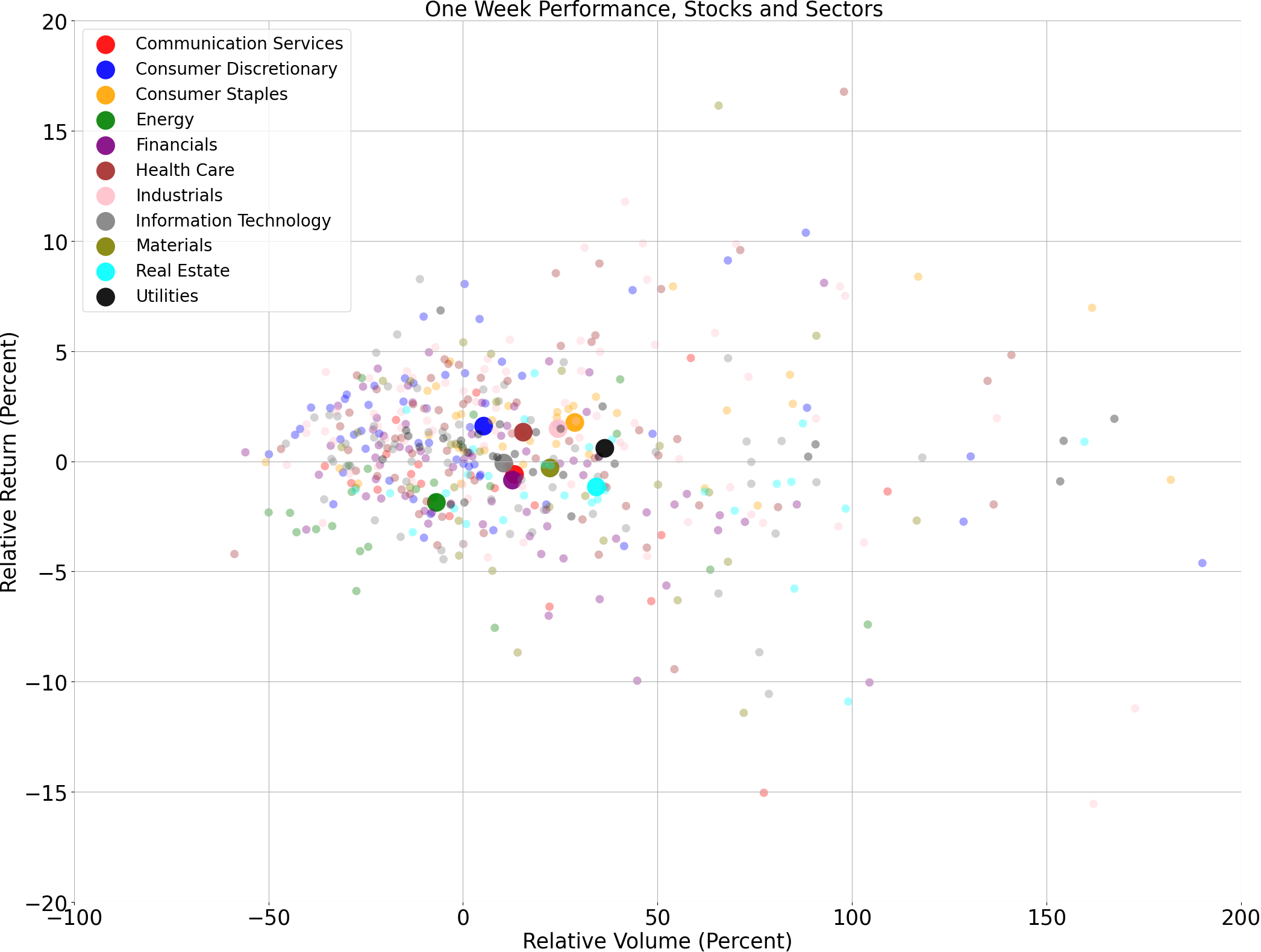

The biggest movers last week on price and volume (Large Cap S&P 500)

Price and volume moves last week for every stock and sector (Large Cap S&P 500)

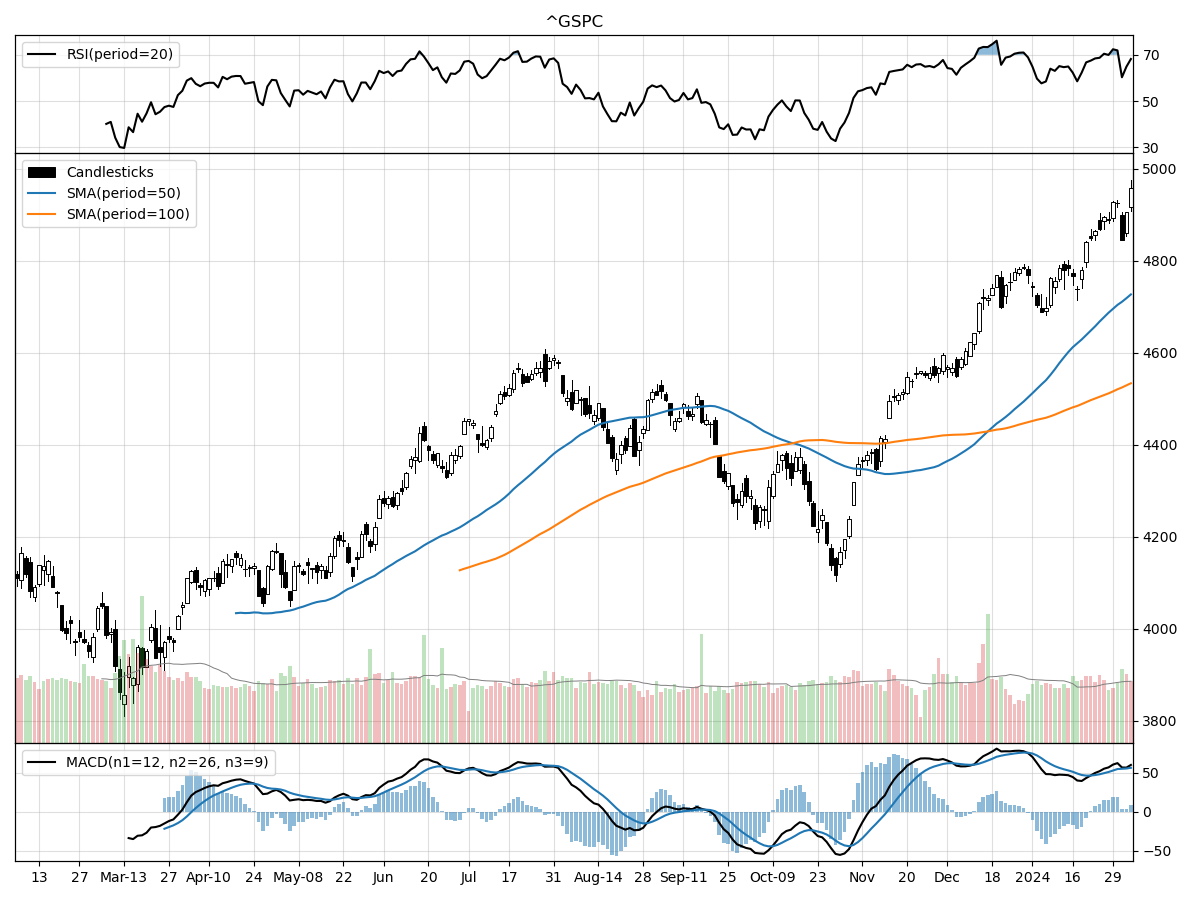

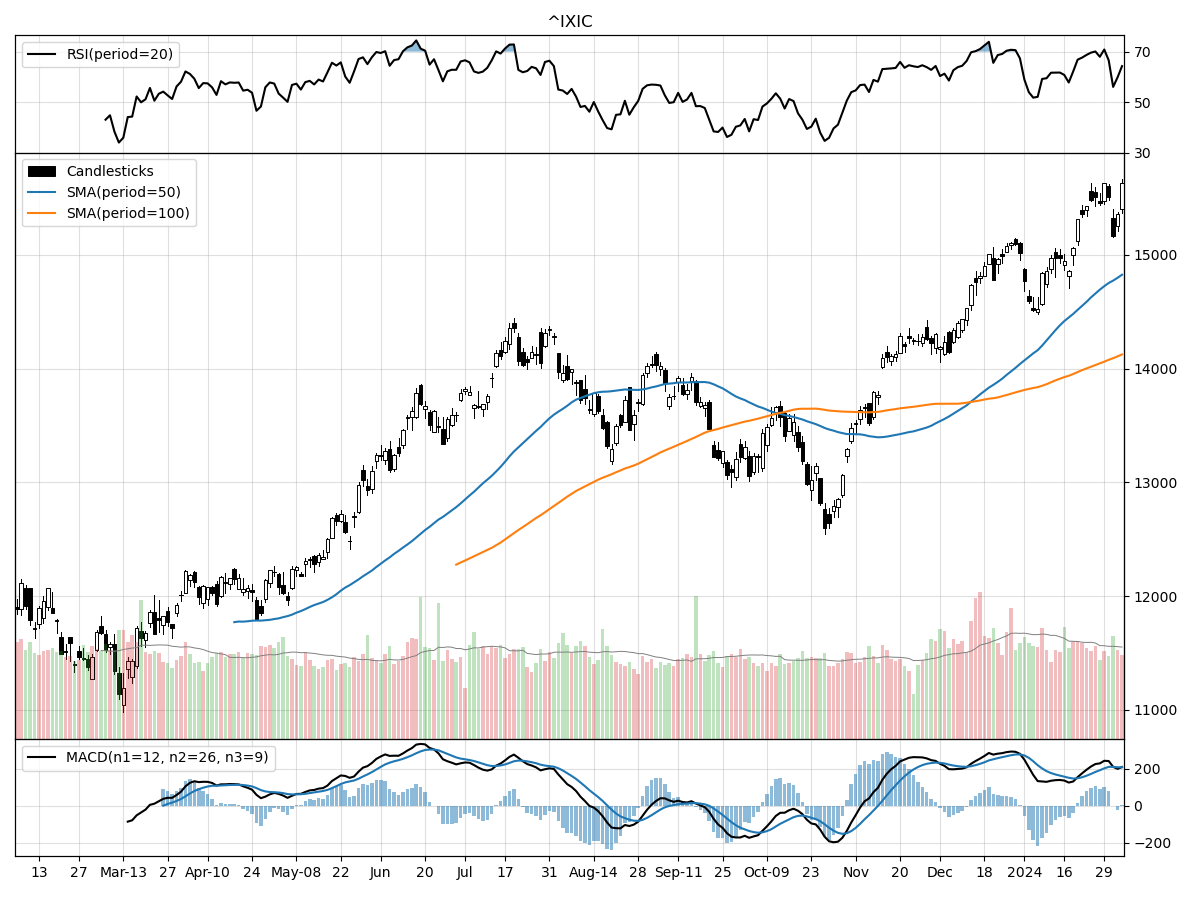

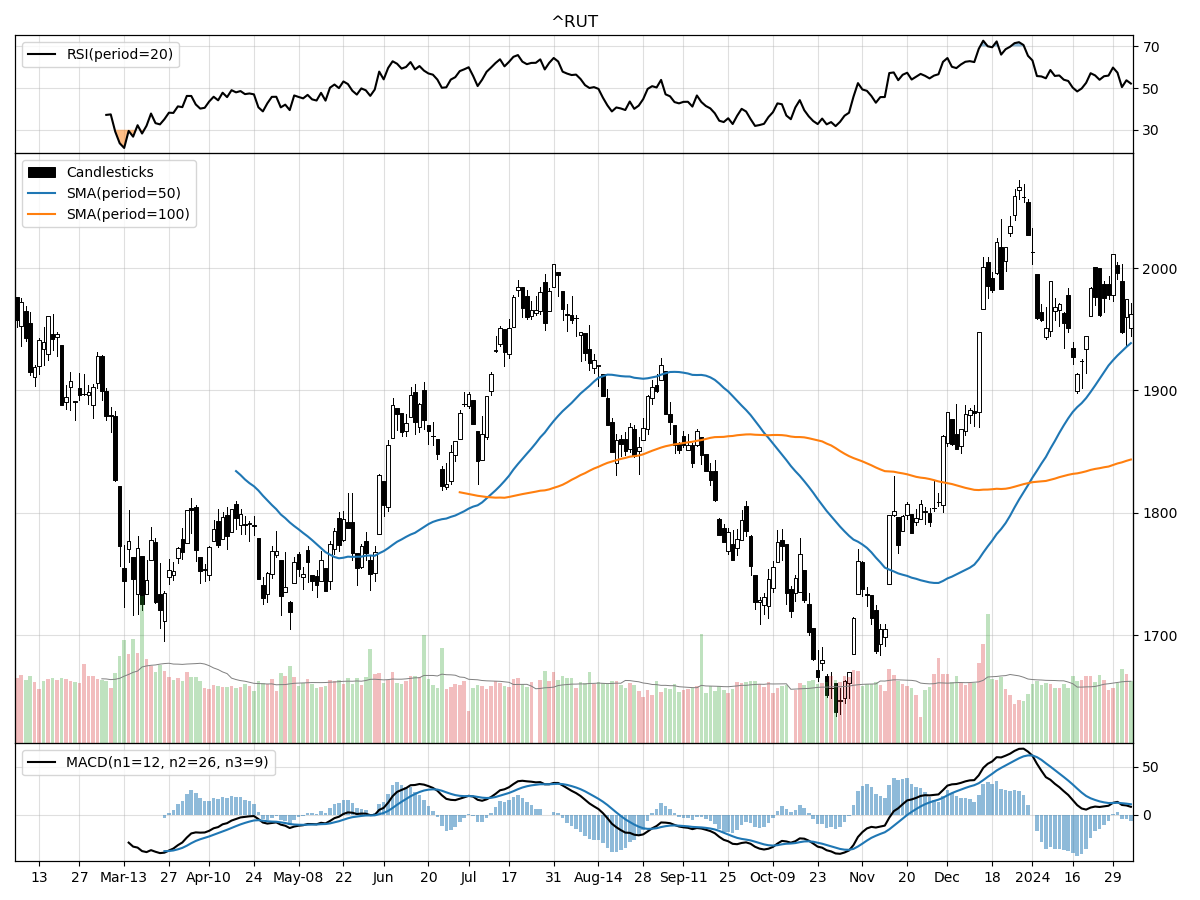

A technical analysis across indices

S&P500

Nasdaq

Russell 2000

The technical performance of the S&P 500, Nasdaq, and Russell 2000 indices show varied momentum and buying pressure, as observed by their respective price movements and technical indicators. The S&P 500 is trading just below its 52-week high, indicating strong bullish momentum, and has seen a significant rise of over 5% in the last month and over 13% in the last three months, suggesting a robust short-to-medium-term uptrend. The heavy buying pressure and accumulation, as evidenced by money flow indicators, coupled with the modestly overbought condition on the RSI and a bullish MACD, indicate that the S&P 500 may have limited upside potential in the short term before facing potential resistance or a pullback.

The Nasdaq index, similar to the S&P 500, is also at its 52-week high and has experienced a notable increase of over 7% in the last month, outperforming the S&P 500 on a month-to-month basis. Over the last three months, it has seen a rise of over 14%, showing a slightly stronger bullish trend than the S&P 500. The Nasdaq's volume is higher than its longer-term average, and with moderate buying pressure and accumulation, the index's momentum is strong. The bullish MACD value is significantly higher than the S&P 500's, suggesting that the Nasdaq may have a stronger bullish sentiment among investors. However, the modestly overbought RSI warns of a potential near-term correction or consolidation.

In contrast, the Russell 2000 Small Cap index shows a more modest performance. It is currently 5% below its 52-week high, indicating that it has not kept pace with the larger-cap indices. The price has remained relatively stable over the last month, but it has seen a comparable rise to the S&P 500 over the last three months. Its daily volume is closely in line with its longer-term average, and the index is under moderate selling pressure, which contrasts with the buying pressure seen in the other indices. The Russell 2000's RSI indicates a neutral position, not overbought or oversold, which may suggest there is room for growth or decline without the immediate pressure of technical correction. The bullish MACD indicates that there is still underlying bullish sentiment, although it is less pronounced than in the S&P 500 and Nasdaq.

Overall, the S&P 500 and Nasdaq indices demonstrate stronger bullish trends and investor sentiment compared to the Russell 2000, with the Nasdaq showing the greatest momentum recently. The Russell 2000's more subdued performance and neutral RSI could offer a different risk-reward profile for investors seeking diversification away from large-cap stocks. Each index's unique technical outlook would attract different types of investors depending on their investment strategy, risk tolerance, and market outlook.

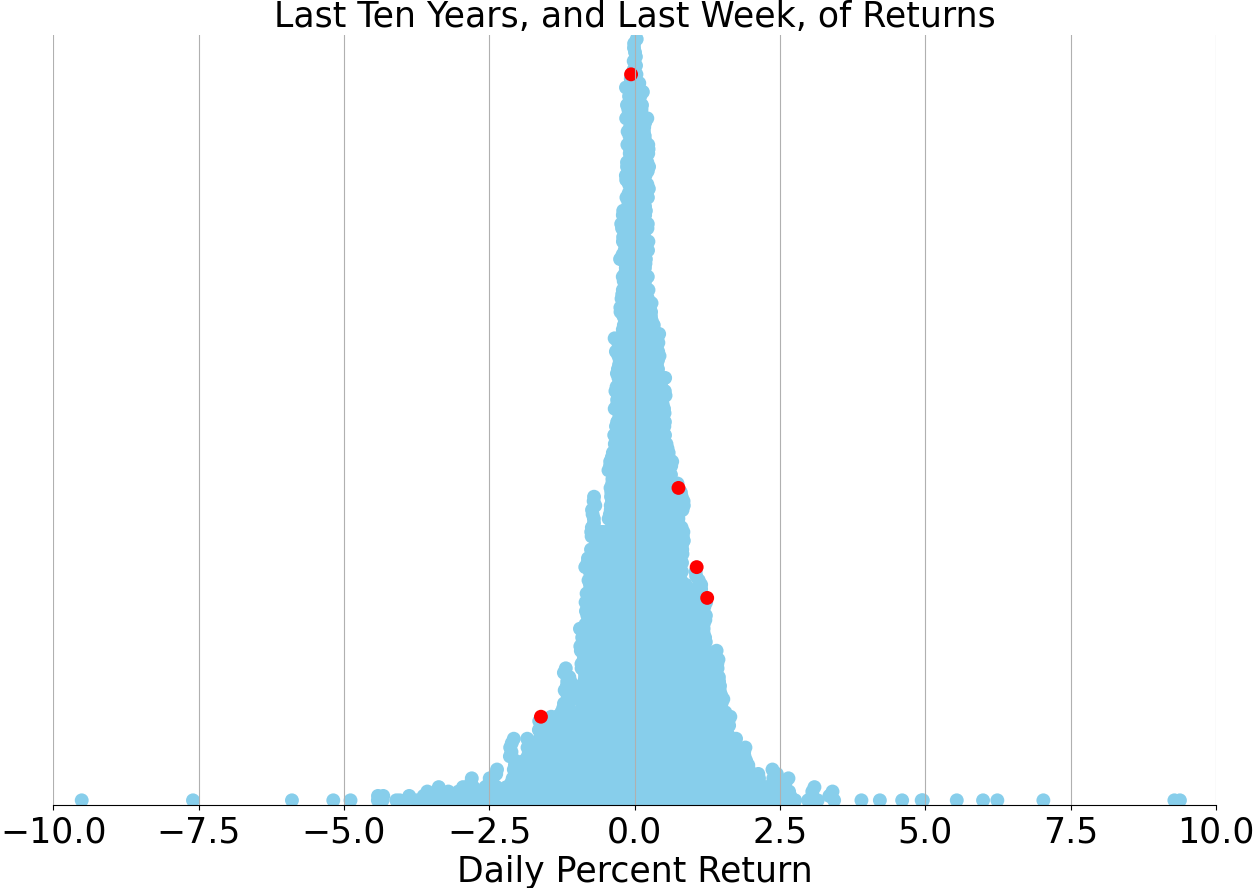

Last week vs. history (Large Cap S&P 500)

Market Commentary

The financial markets experienced a week of dramatic swings, ultimately culminating in a modest uptick, with the S&P 500 reaching new heights. Investors were particularly focused on the Federal Reserve's latest policy meeting. The Fed, under Chairman Jerome Powell's guidance, signaled a willingness to maintain current interest rates while closely monitoring inflation trends, suggesting that rate cuts are on the horizon, but their timing remains contingent on further economic data.

The labor market proved to be a bastion of strength, with the January jobs report revealing an addition of 353,000 nonfarm payrolls, significantly surpassing expectations. This robust figure, the strongest monthly gain in over a year, suggests enduring economic resilience. Despite this surge in job creation, the unemployment rate held steady at 3.7%, just marginally above a 50-year low. The stability in unemployment, despite significant job growth, can be attributed to an expanding labor force.

Wage growth, however, presented a more complex narrative, accelerating in January to a 4.5% year-over-year increase. This uptick in wages could potentially complicate the Fed's inflation outlook, as rising wages can contribute to inflationary pressures. Nonetheless, the Fed's current stance appears to be one of cautious observation, as it balances the dual objectives of controlling inflation and supporting economic growth.

On the productivity front, there are encouraging signs that increased labor productivity could help moderate inflation while sustaining economic output. This development, if sustained, could provide the Fed with more leeway to navigate the delicate process of adjusting monetary policy without derailing the economy's momentum.

Investors should brace for potential market turbulence as the Fed gears up for a policy shift. Historical trends suggest that initial rate cuts by the Fed can be accompanied by market pullbacks, which, in retrospect, have often presented buying opportunities. However, these periods of volatility are not guaranteed to follow past patterns, and investors should remain vigilant and prepared for a range of outcomes.

The performance of regional banks has come under scrutiny, with some underperforming compared to their larger counterparts. This divergence highlights the nuanced impacts of economic developments and Fed policy on different segments of the financial sector. Investors would do well to monitor these trends, as they may signal broader shifts in the market landscape.

In conclusion, the latest economic data and Fed communications paint a picture of a robust labor market and a central bank that is carefully calibrating its approach to monetary policy. While the prospect of rate cuts looms, their timing and impact remain uncertain. Investors should stay informed and agile, ready to navigate the complexities of an evolving economic environment. As always, a prudent approach that considers both the opportunities and risks in the current market is advisable.

Comments ()