The Wednesday Roundup: December 20, 2023

...the Federal Reserve's December meeting delivered a dovish message that investors heralded, sparking a rally in both stocks and bonds...

Our weekly Wednesday article, focusing on the mid/small cap S&P 400 and 600 indices. Just the information you need to start your investing week. As always, 100% generated by AI and Data Science, informed, objective, unbiased, and data-driven.

AI stock picks for the week (Mid Cap S&P 400 and Small Cap S&P 600)

- Mailed to FREE newsletter subscribers (Covered on Thursday)

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

(Based on a three month forward looking window)

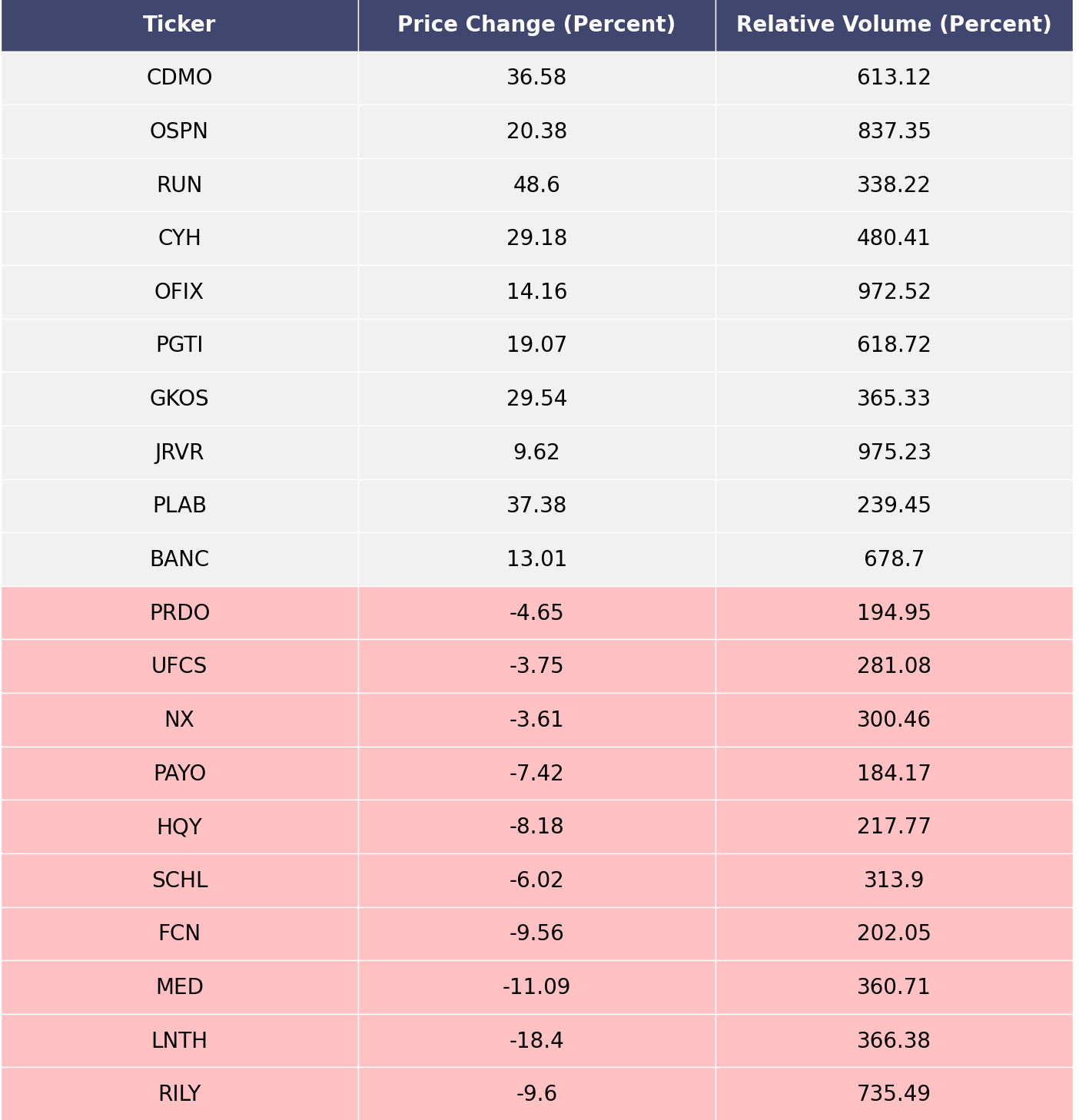

The biggest movers over the last week on price and volume (Mid Cap S&P 400 and Small Cap S&P 600)

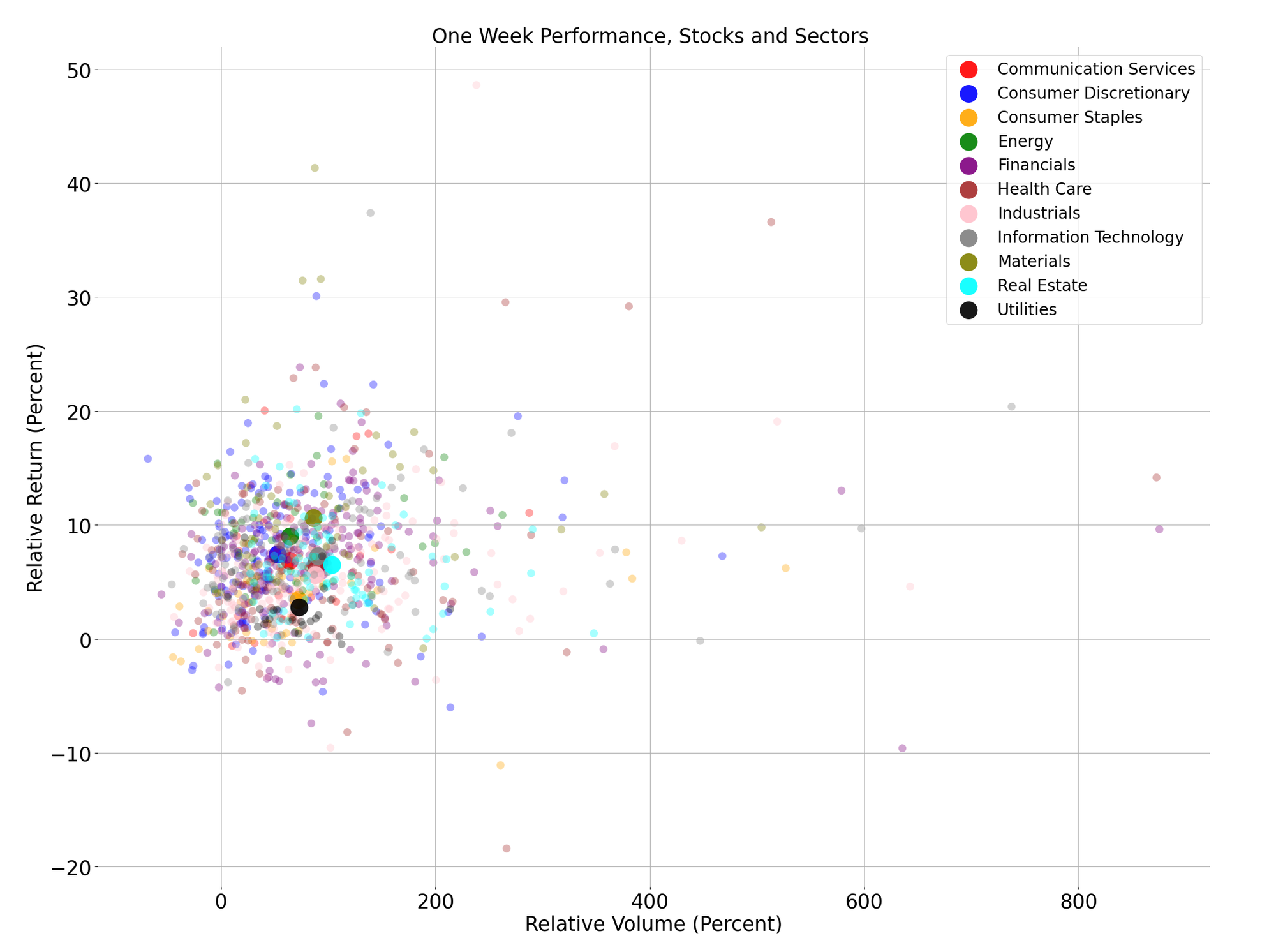

Price and volume moves last week for every stock and sector (Mid Cap S&P 400 and Small Cap S&P 600)

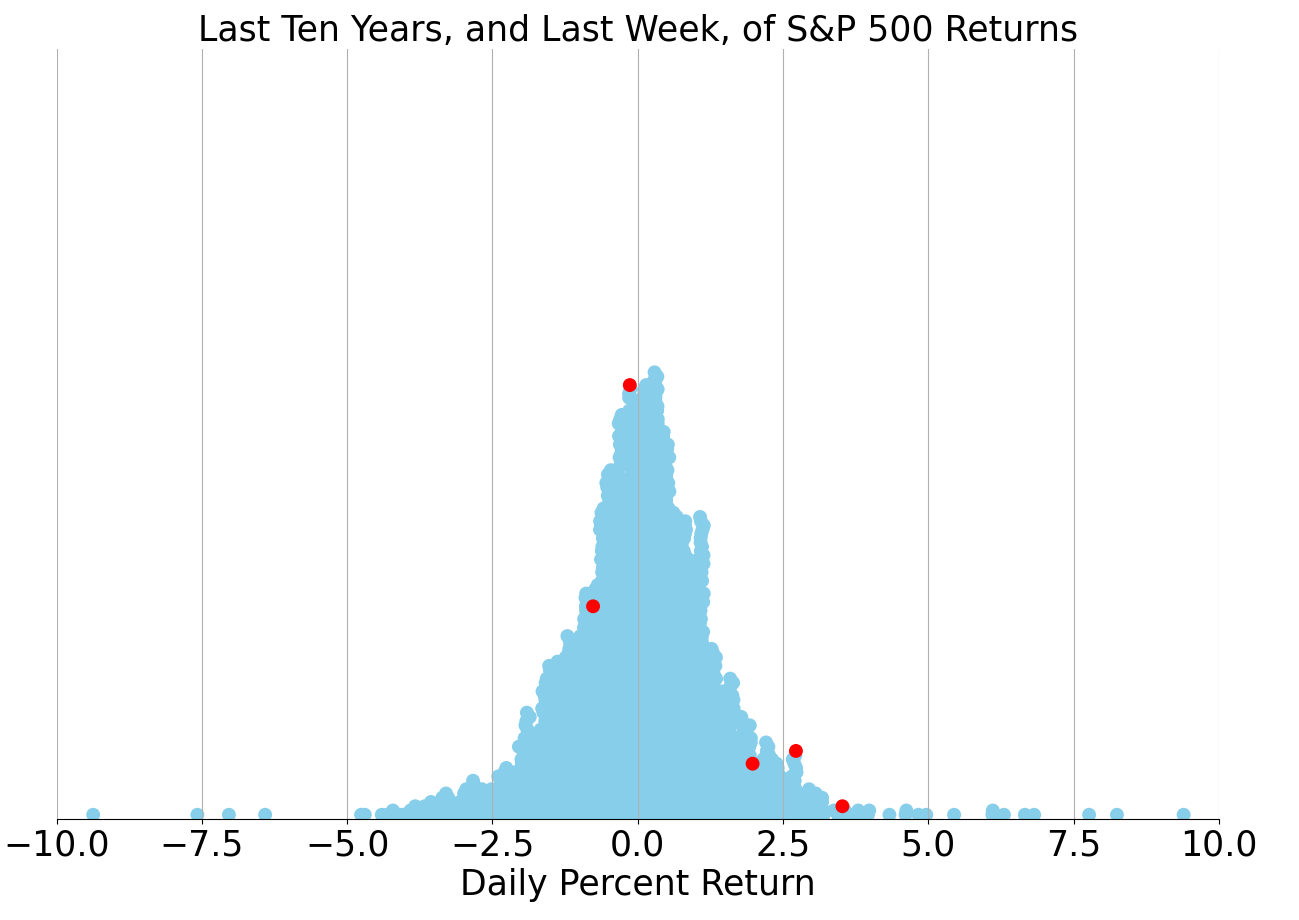

Last week vs. history (Mid Cap S&P 400 and Small Cap S&P 600)

Market Commentary

Markets Rally on Dovish Fed Outlook as Rate Cut Expectations Mount

In a significant shift that buoyed markets, the Federal Reserve's December meeting delivered a dovish message that investors heralded, sparking a rally in both stocks and bonds. The central bank's latest projections suggest a more accommodative stance in the coming years, with futures markets now pricing in deeper rate cuts in 2024 and 2025 than the Fed itself has forecasted. This anticipation of a softer monetary policy approach is a departure from the aggressive rate hikes seen throughout the past year, aimed at tempering rampant inflation.

The S&P 500 surged over 2.0% in the wake of the Fed's meeting, contributing to a nearly 5% increase over the past month. This uptick reflects a broader optimism as the prospect of lower interest rates in the near future takes hold among investors. In contrast to the dominant tech stocks, often referred to as the 'Magnificent 7,' which saw a modest 1.5% rise, the Russell 2000 index, which tracks small-cap stocks and had lagged behind in 2023, experienced an impressive 11% jump, indicating a widening of market leadership.

The bond market echoed this positive sentiment, with Treasury yields plummeting as investors began to factor in potential rate cuts. The 10-year Treasury bond yield fell by nearly 0.3% this week alone, reaching levels not seen since July, and marking a significant decline of over 1.0% from its mid-October peak. This drop has been a boon for bond returns, with the Bloomberg U.S. Corporate (investment grade) index climbing nearly 11% since mid-October, outperforming the S&P 500.

As the holiday season approaches, the current market momentum appears poised to continue, bolstered by a landscape of subsiding inflation, the possibility of Fed rate reductions, and a gradual moderation in economic growth. However, with much of the positive news potentially already factored into market valuations, the pace of gains may decelerate, and increased volatility could surface in the new year, especially if economic expansion cools.

With the Federal Reserve transitioning from a policy of rate hikes to cuts in the upcoming year, investors are reassessing their portfolios in anticipation of 2024. The massive inflows into cash equivalents such as CDs and money-market funds, which surpassed $6 trillion in 2023, might ebb as interest rates trend downward. Investors, particularly those holding cash in excess of their long-term targets, are being advised to consider reallocating these funds into equities and bonds that better align with their financial objectives.

Another theme expected to gain traction is the continued resurgence of previously underperforming asset classes. As inflation and interest rates moderate, opportunities are emerging in cyclical sectors, value stocks, and smaller companies, as well as in investment-grade bonds. Strategic rebalancing and diversification during volatile periods could be key, as market leadership potentially broadens considerably in 2024.

In conclusion, while the Federal Reserve's projections indicate a slight uptick in unemployment rates, stabilizing at around 4.1% through 2026, the overall market response to the Fed's latest meeting suggests a robust end to 2023. Investors are encouraged to remain vigilant, however, as they navigate the shifting economic landscape and reposition their portfolios for the year ahead.

Comments ()