The Wednesday Roundup: February 14, 2024

In a remarkable display of market resilience, the S&P 500 Index has soared past the 5,000 mark, setting a new record and signaling the enduring strength of U.S. large-cap stocks...

Our weekly Wednesday article, focusing on the mid/small cap S&P 400 and 600 indices. Just the information you need to start your investing week. As always, 100% generated by AI and Data Science, informed, objective, unbiased, and data-driven.

First off, check out our new Sector AI content, updated weekly, here!

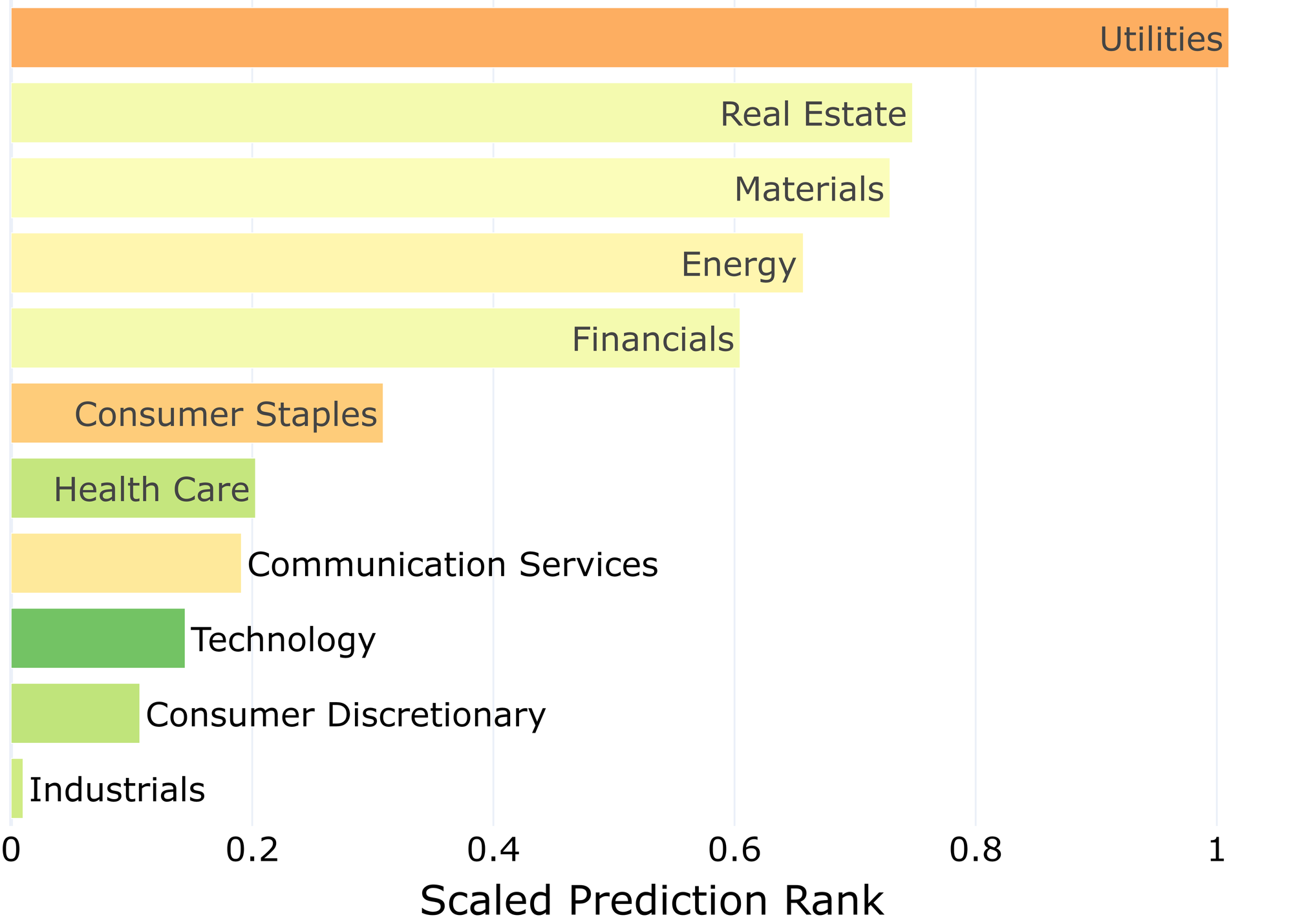

AI stock picks for the week (Mid/Small Cap S&P 400 and S&P 600)

(Scroll to the bottom now)

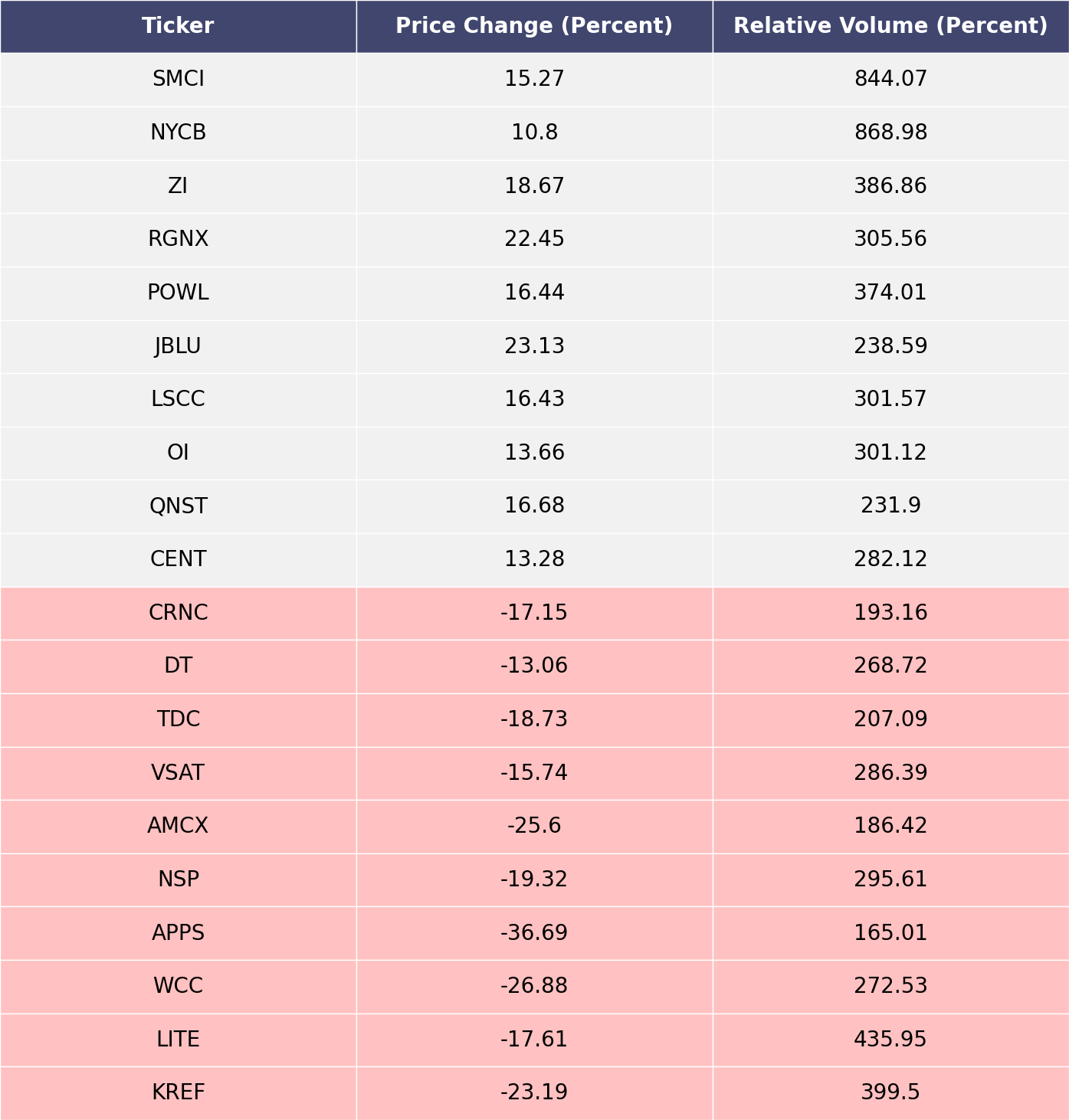

The biggest movers over the last week on price and volume (Mid Cap S&P 400 and Small Cap S&P 600)

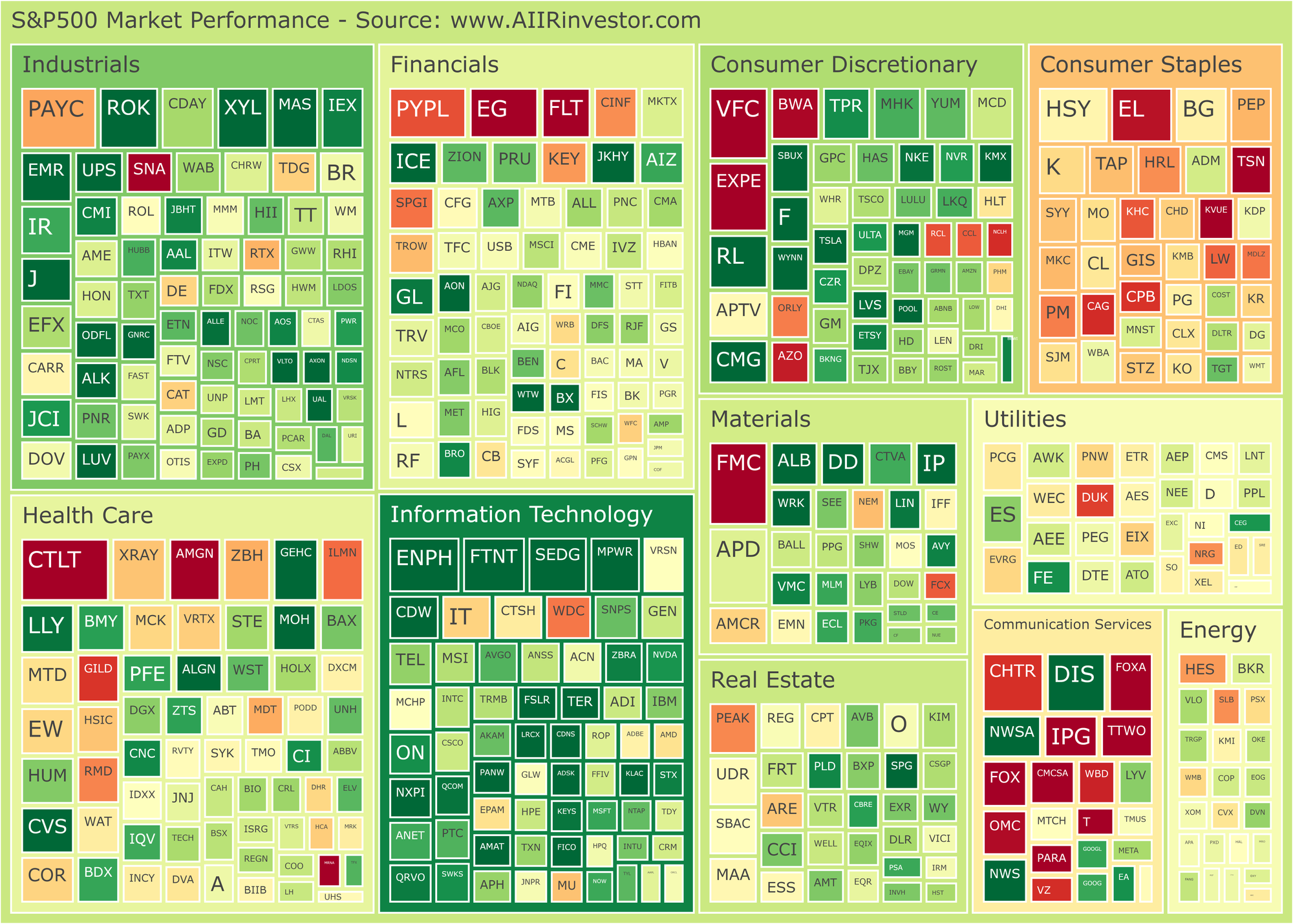

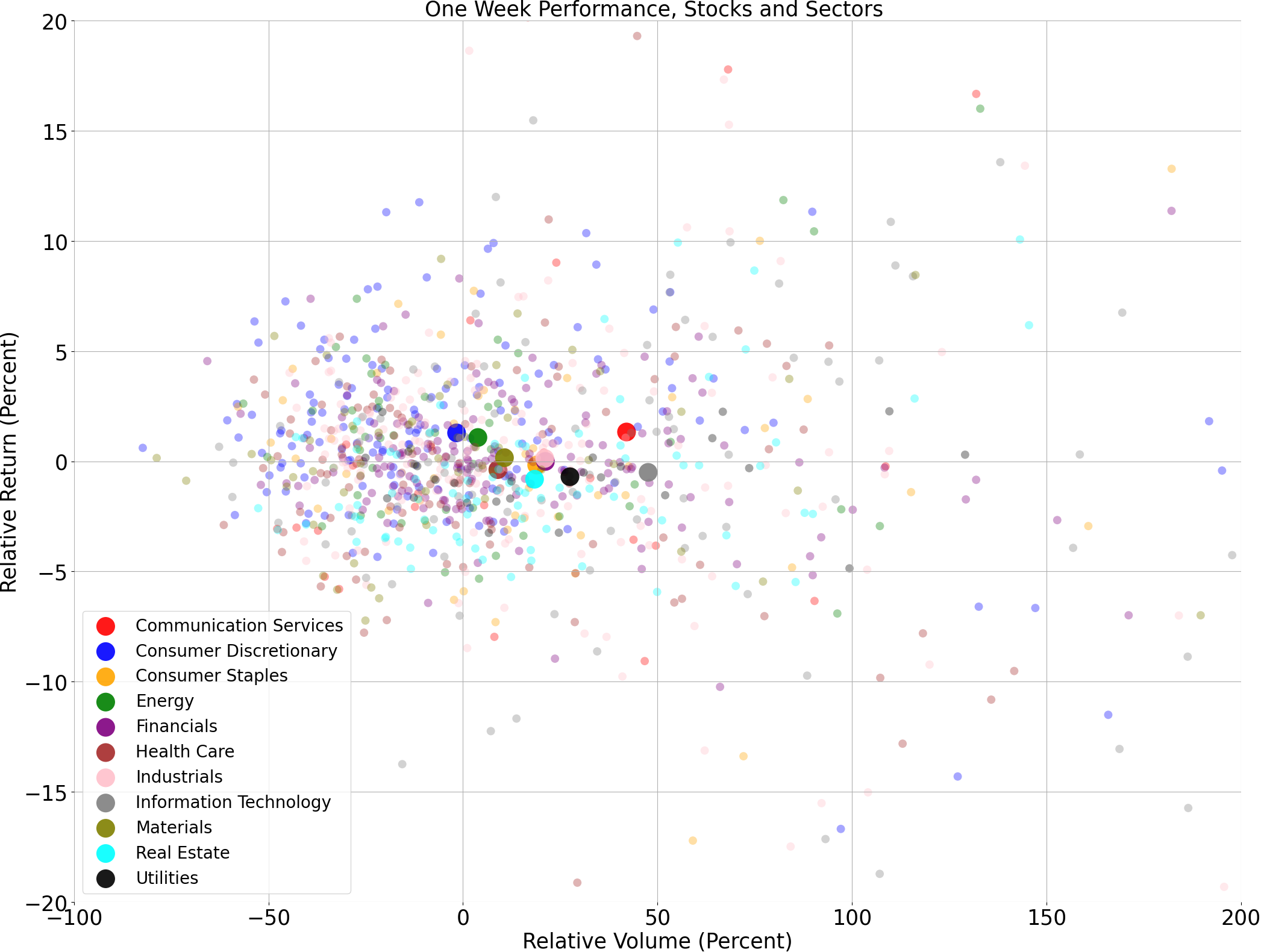

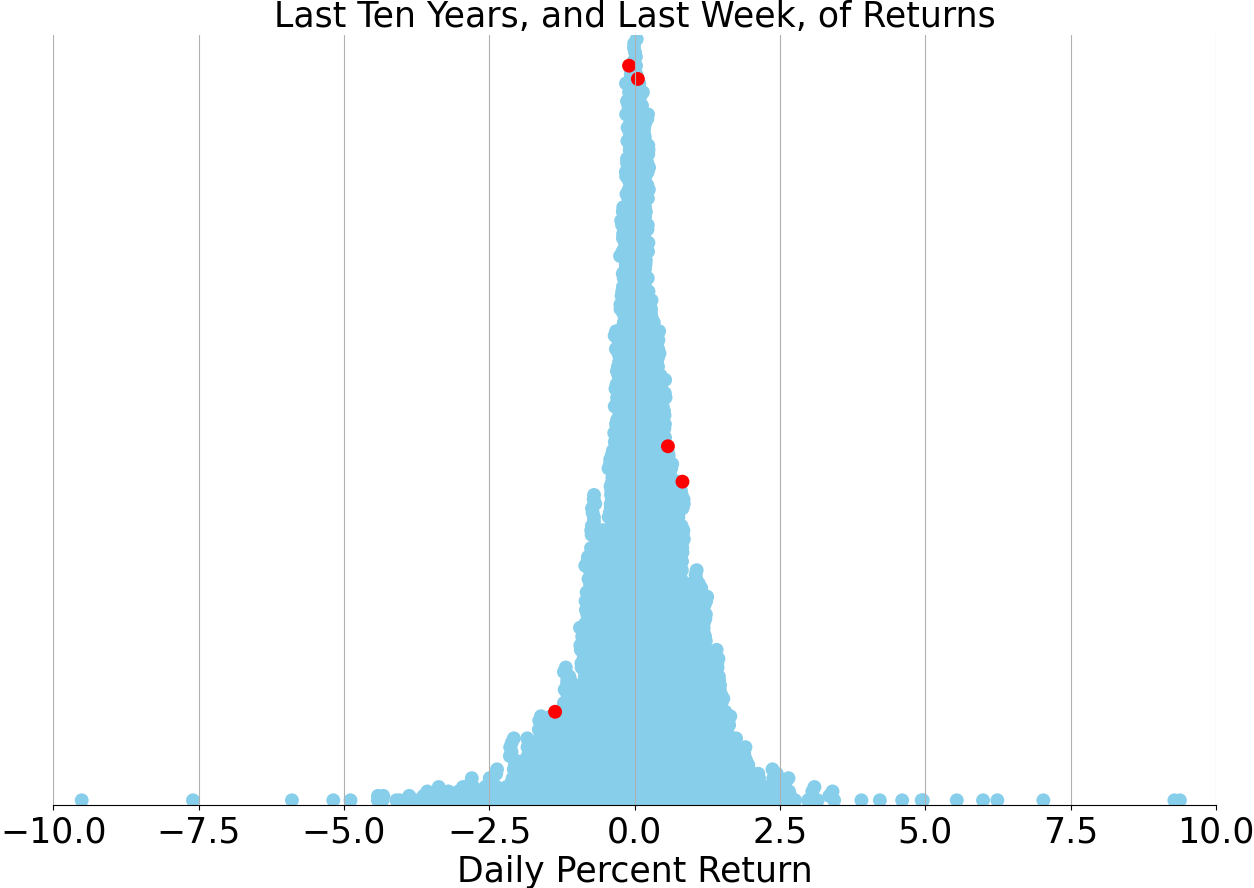

Price and volume moves last week for every stock and sector (Mid Cap S&P 400 and Small Cap S&P 600)

Last week vs. history (Mid Cap S&P 400 and Small Cap S&P 600)

Market Commentary

In a remarkable display of market resilience, the S&P 500 Index has soared past the 5,000 mark, setting a new record and signaling the enduring strength of U.S. large-cap stocks. This milestone, while largely symbolic, underscores the market's robust recovery from a period of heightened interest rate volatility. Only a year prior, the specter of recession loomed large, yet today, the public's interest in recession has waned, overshadowed by cultural phenomena like Taylor Swift, as indicated by Google search trends. This shift in focus mirrors the economic landscape's better-than-expected growth trajectory and easing inflation concerns, which have seen stocks rally by approximately 20% in the last quarter.

Consumer spending, a pillar of the U.S. economy, has remained vigorous despite the headwinds of high borrowing costs and last year's inflationary pressures. A surge in discretionary spending, including a significant uptick in performing arts expenditures, has contributed to this robustness. Factors such as pandemic-era savings, a tight labor market, and previously low mortgage rates have underpinned this strength. However, emerging signs of consumer strain, including a slowdown in consumer credit and rising card delinquencies, suggest a potential cooling off. Nevertheless, the overall health of household finances, bolstered by wage gains and appreciating assets, continues to support consumer confidence.

The Federal Reserve's aggressive rate hikes have left their mark, particularly on the housing and manufacturing sectors, which are sensitive to interest rate changes. After nine quarters of decline, housing's contribution to economic growth has turned positive, and manufacturing activity, as measured by the ISM Purchasing Managers Index (PMI), is showing signs of recovery. The recent easing of mortgage rates and improved homebuilder sentiment, coupled with a stabilization in housing supply, hint at a brighter outlook for these sectors.

As the Fed shifts towards a less restrictive policy stance, the risk of a hard landing or recession is diminishing. The latest Senior Loan Officer Opinion Survey (SLOOS) indicates a loosening in credit conditions, suggesting a potential rebound in various economic sectors later in the year. Additionally, a moderation in labor costs implies that the Fed may achieve its inflation objectives without necessitating a significant economic slowdown.

The market's performance has been heavily influenced by a select group of mega-cap technology stocks, driven by enthusiasm around artificial intelligence (AI). However, there are signs that market leadership is broadening, with sectors like industrials and homebuilders gaining momentum. This suggests the possibility of a shift in investor focus from mega-cap tech to cyclical and value-style investments, particularly if the Fed's rate cuts are motivated by positive developments rather than a growth slump.

Historically, the conclusion of a Fed tightening cycle has often heralded strong returns across both stocks and bonds, with equities typically outperforming. The performance of mid-cap stocks before and after the last Fed hike is particularly noteworthy, as they have demonstrated significant swings, making them an intriguing prospect in the current environment. Moreover, a recovery in manufacturing activity has historically favored small-cap stocks and cyclical sectors, suggesting potential investment opportunities as the PMI rebounds.

In the international arena, while certain markets like the German DAX and French CAC are reaching new heights, others, such as China's MSCI Index, are struggling amid ongoing housing issues. Despite the attractive valuations and dividend yields of international equities compared to their U.S. counterparts, investors are advised to maintain strategic allocations and remain mindful of the varying economic and growth dynamics across regions. The potential for international equities to catch up hinges on a resurgence in global growth, which remains to be seen.

AI stock picks for the week (Large Cap S&P 500)

Subscribe for AI stock picks (it's free!)