The Wednesday Roundup: January 10, 2024

AI stock picks for the week (Mid Cap S&P 400 and Small Cap S&P 600)

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers (Covered on Thursday)

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

(Based on a three month forward looking window)

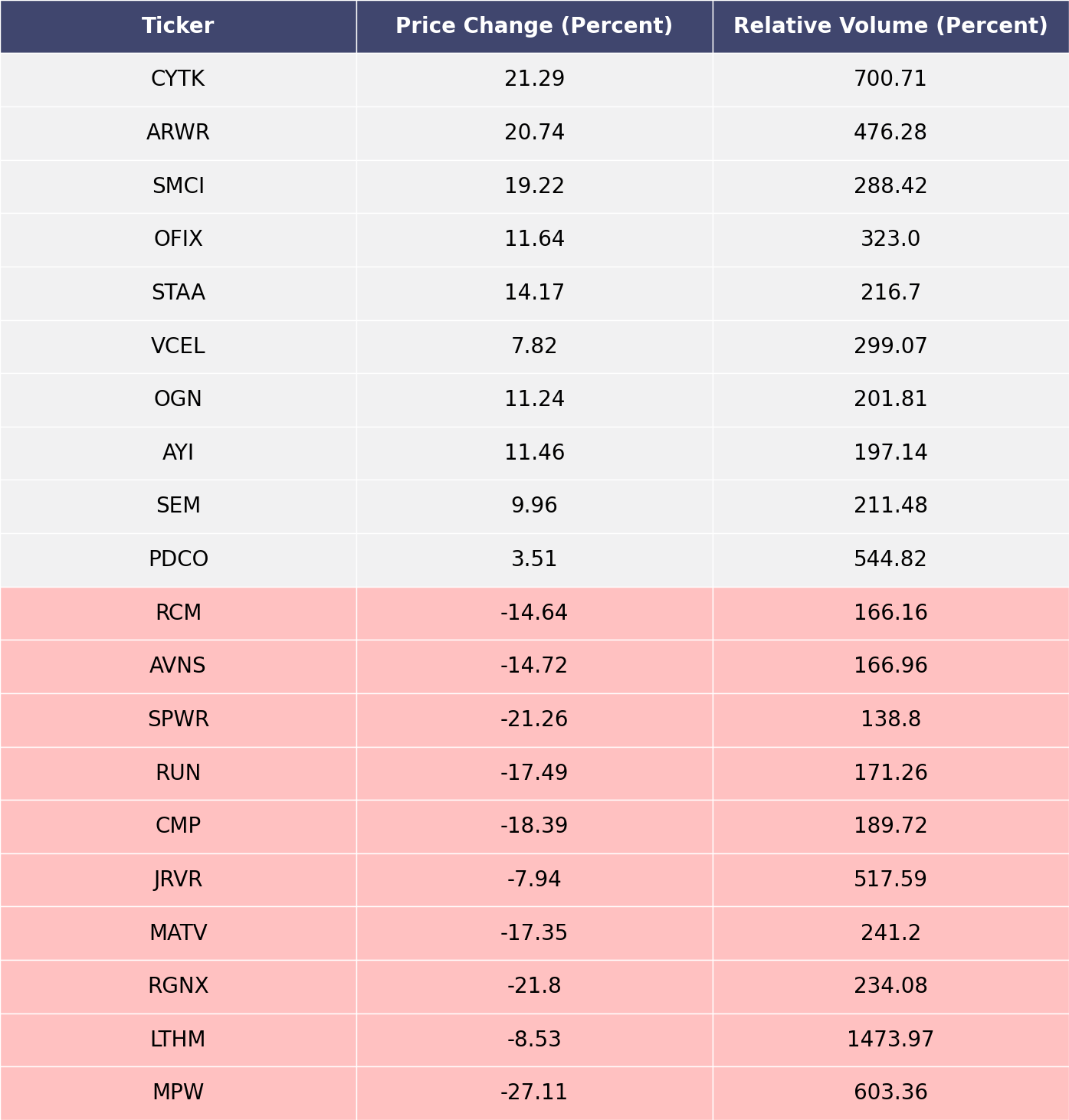

The biggest movers over the last week on price and volume (Mid Cap S&P 400 and Small Cap S&P 600)

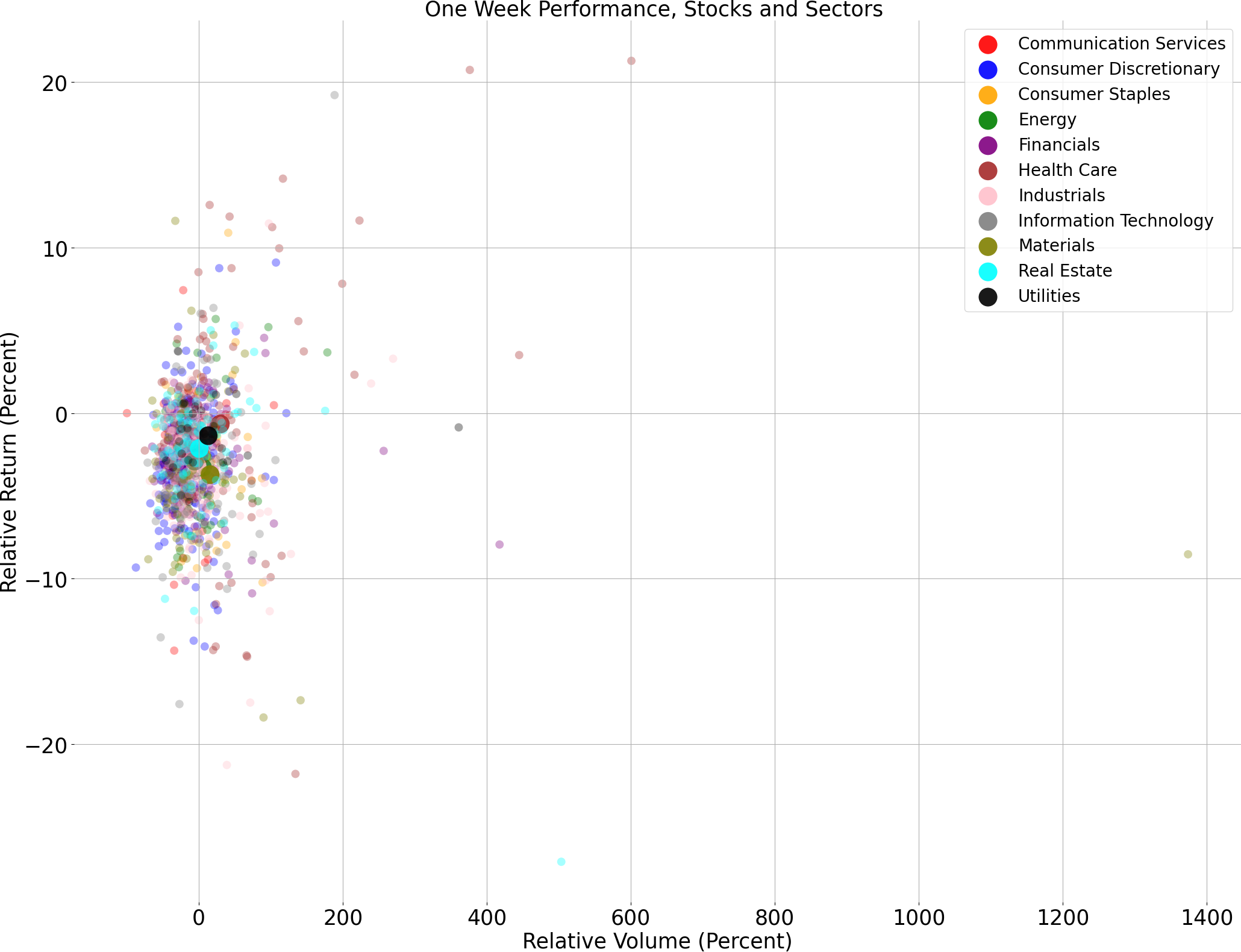

Price and volume moves last week for every stock and sector (Mid Cap S&P 400 and Small Cap S&P 600)

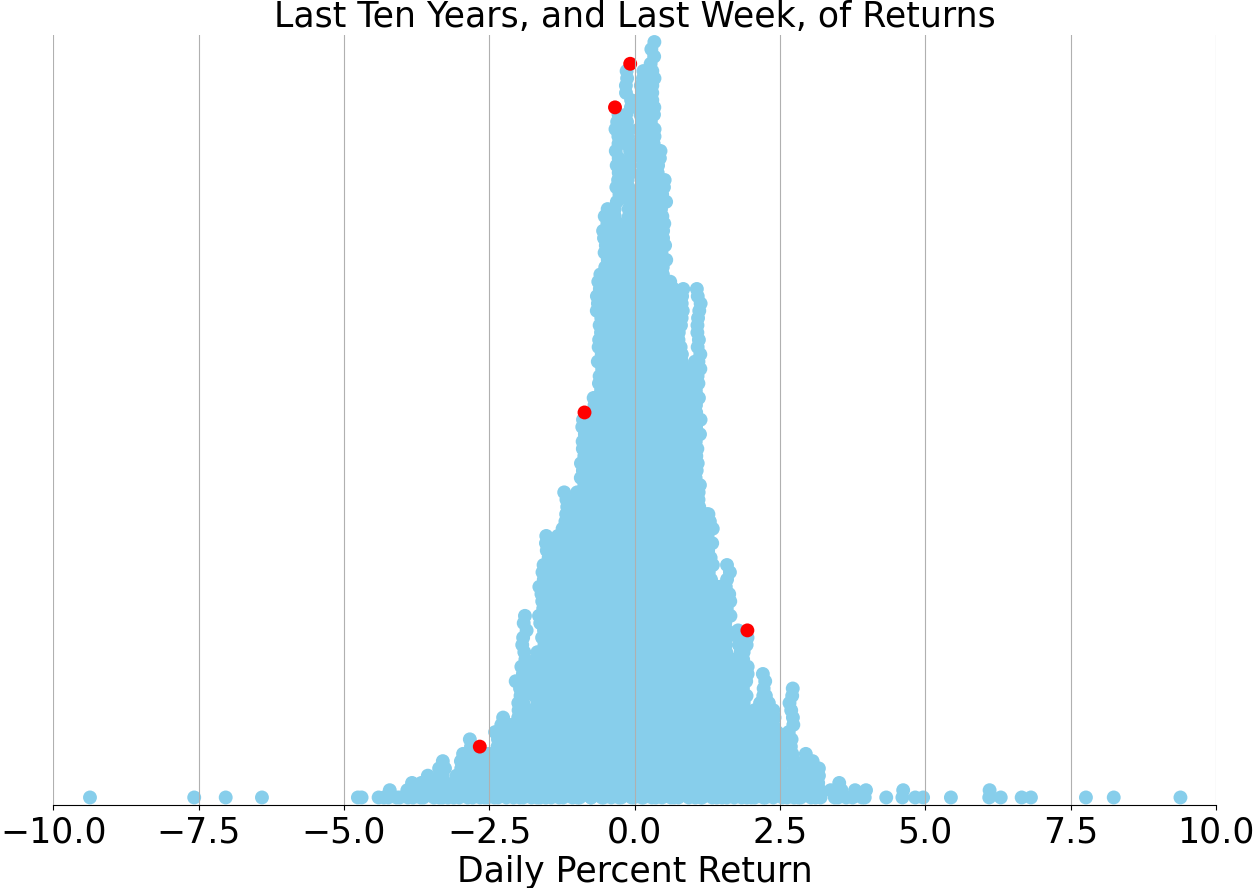

Last week vs. history (Mid Cap S&P 400 and Small Cap S&P 600)

Market Commentary

Navigating the Financial Landscape: A 2023 Retrospective and the Road Ahead for 2024

As the year 2023 drew to a close, the financial markets delivered a narrative of resilience and recovery, defying the initial gloom of recessionary fears that had clouded the horizon at the outset. Investors witnessed a remarkable turnaround, with most asset classes across the diversified portfolio spectrum registering commendable performance. This upswing was underpinned by several factors, including the softening of inflationary pressures, a gradual end to the Federal Reserve's tightening cycle, and burgeoning optimism around the potential of artificial intelligence (AI). These tailwinds served as a testament to the enduring value of a disciplined investment strategy amidst the unpredictability of market dynamics.

The easing of inflation emerged as a pivotal driver of positive market outcomes in 2023. With the Consumer Price Index (CPI) retreating significantly from its mid-2022 peak, the economy found much-needed reprieve. The decline in energy costs played a role, but the broader deceleration in price increases across various sectors was more indicative of a systemic disinflationary trend. This trend was further reinforced by the normalization of supply chains, which had been previously disrupted by the pandemic, leading to a reduction in goods prices.

In March, the spotlight momentarily shifted from inflation to financial stability, as the collapse of several regional banks, including Silicon Valley Bank and Signature Bank, rattled confidence in the banking system. Unlike the 2008 crisis, which was precipitated by excessive risk-taking and the bursting of the housing bubble, the 2023 banking sector's woes were largely attributed to the rapid interest rate hikes by the Fed, which eroded the value of bond securities held by banks. The subsequent bank runs highlighted vulnerabilities within the financial system, prompting decisive interventions by the Fed, Treasury, and FDIC to stabilize the situation.

Despite these challenges, the labor market and consumer spending delivered an unexpected boon, with the anticipated recession failing to materialize. While manufacturing and housing sectors experienced downturns, robust consumer spending, particularly on services, buoyed economic growth. The labor market remained tight, with unemployment rates hitting historic lows and job openings outnumbering the unemployed. This consumer-driven resilience underscored the economy's ability to withstand the headwinds of rising interest rates, albeit with the recognition that the impact of such rates would eventually wane.

The Federal Reserve's policy trajectory was a dominant influence on market behavior throughout the year. After multiple rate hikes in 2022 and 2023, the policy rate reached a 22-year peak. However, towards the end of the year, the Fed signaled a significant shift, indicating the end of the tightening cycle and the onset of rate cuts projected for 2024. This dovish pivot acknowledged the progress made in curbing inflation and was seen as a positive development for the markets, despite the potential for volatility arising from the disparity between market expectations and Fed projections.

Market leadership in 2023 was notably narrow, with a handful of mega-cap technology companies, particularly those involved in AI, driving the S&P 500's gains. This concentration of market performance highlighted the disproportionate influence of these "Magnificent 7" companies, even as the broader market experienced a more muted trajectory. As the year concluded, however, the rally began to broaden, suggesting opportunities for investors to capitalize on more favorable valuations in overlooked market segments.

As the financial community bids farewell to 2023 and looks ahead to 2024, there is cautious optimism. The backdrop of moderating inflation, potential interest rate cuts, and rebounding corporate earnings sets a promising stage for the new year. While the markets will undoubtedly encounter new challenges and uncertainties, the lessons of the past year reinforce the importance of strategic investment and the potential for growth in a dynamic economic landscape. As always, investors are reminded to consider their unique objectives and financial situations when navigating the evolving market conditions.

Comments ()