The Wednesday Roundup: January 31, 2024

the U.S. economy has been demonstrating As we delve into the economic landscape of 2024, the U.S. economy has been demonstrating robust growth, defying earlier apprehensions of a slowdown. Recent data indicates that the economy is not only expanding but doing so with a renewed dynamism...

Our weekly Wednesday article, focusing on the mid/small cap S&P 400 and 600 indices. Just the information you need to start your investing week. As always, 100% generated by AI and Data Science, informed, objective, unbiased, and data-driven.

AI stock picks for the week (Mid Cap S&P 400 and Small Cap S&P 600)

- Mailed to FREE newsletter subscribers (Covered on Thursday)

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

(Based on a three month forward looking window)

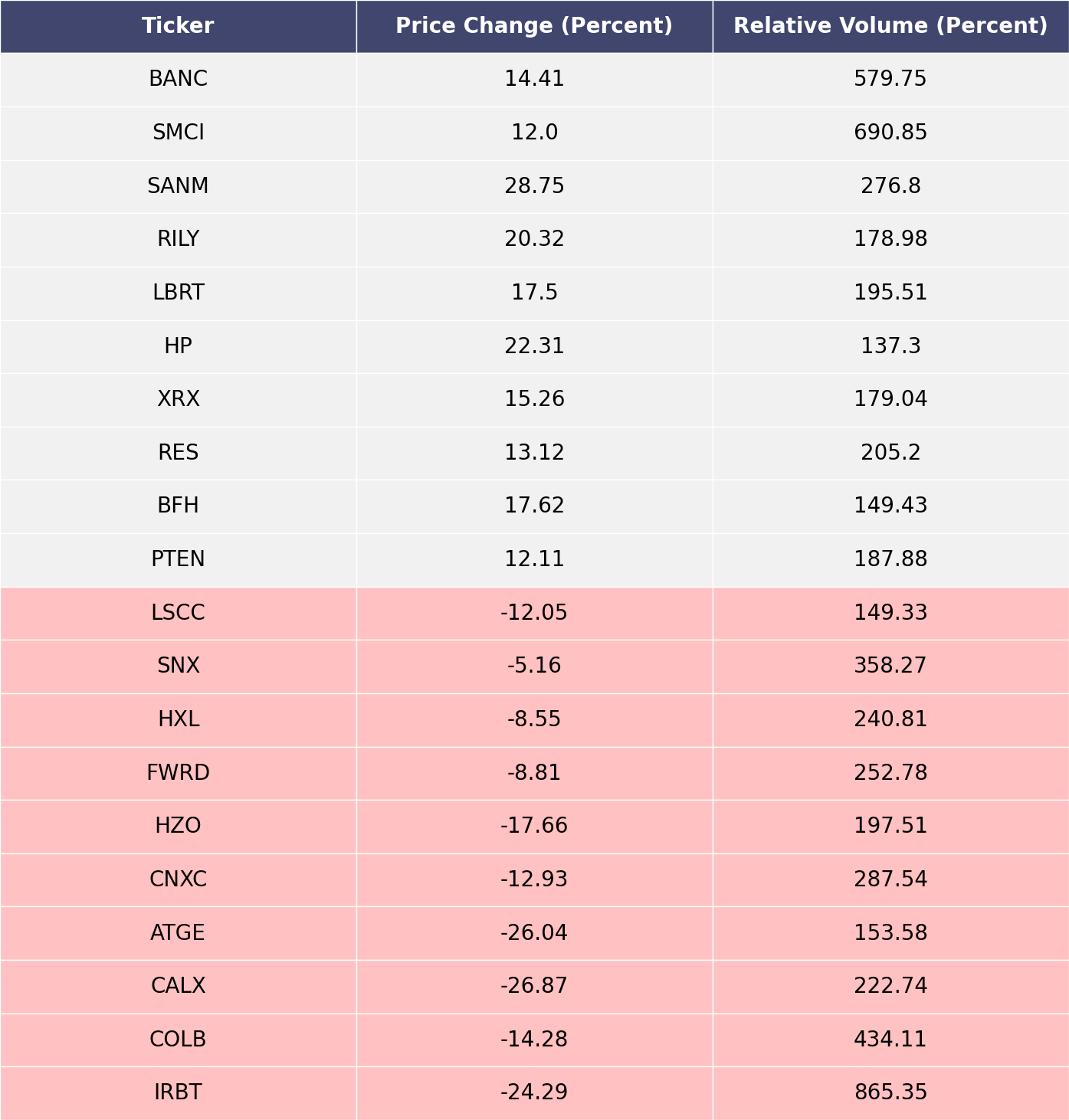

The biggest movers over the last week on price and volume (Mid Cap S&P 400 and Small Cap S&P 600)

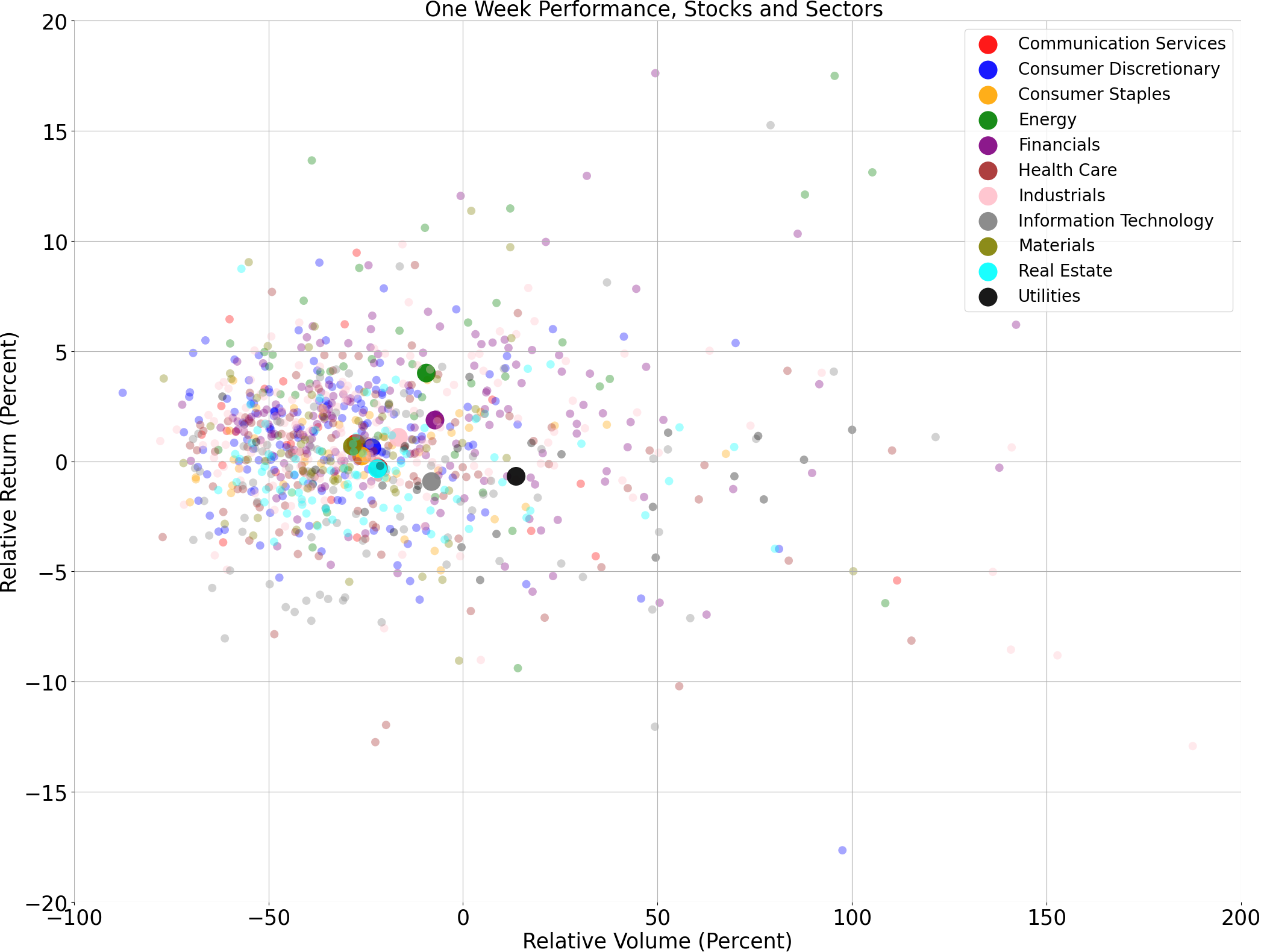

Price and volume moves last week for every stock and sector (Mid Cap S&P 400 and Small Cap S&P 600)

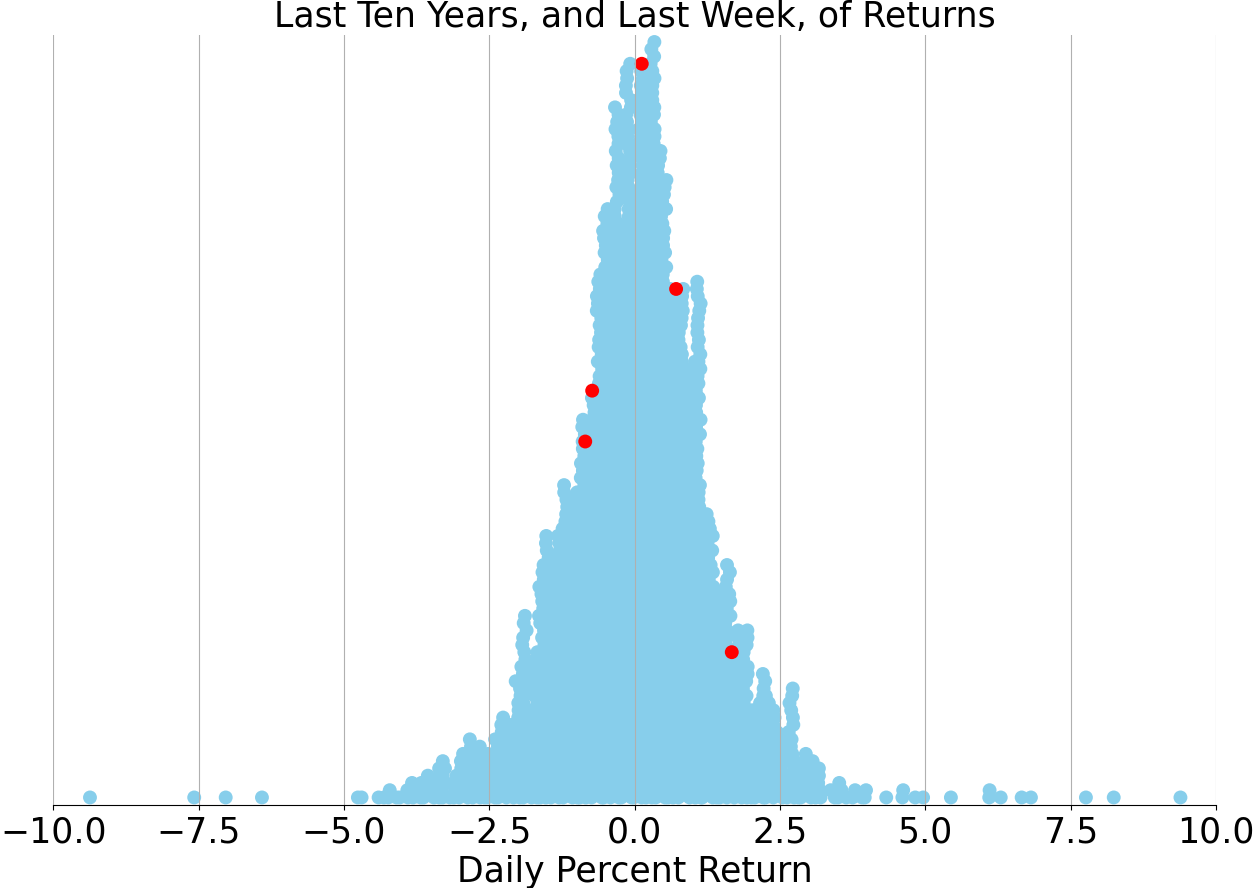

Last week vs. history (Mid Cap S&P 400 and Small Cap S&P 600)

Market Commentary

Title: U.S. Economy Exhibits Vigor Amid Moderating Inflation, Markets Eye Fed's Next Moves

As we delve into the economic landscape of 2024, the U.S. economy has been demonstrating robust growth, defying earlier apprehensions of a slowdown. Recent data indicates that the economy is not only expanding but doing so with a renewed dynamism that has not been observed since late 2022. The S&P manufacturing PMI, a bellwether of industrial health, soared to a reading of 50.3 in January, marking the highest point since the preceding October. This resurgence is mirrored in the real GDP and personal consumption figures, which have shown quarter-over-quarter annualized growth. However, projections suggest a moderation in this growth trajectory before a potential rebound later in the year, a pattern that is not uncommon in economic cycles.

Inflation, the bane of the economy in previous years, appears to be relenting, as evidenced by the prices-charged index within the PMI report, which has plummeted to levels unseen since May 2020. This drop is a significant retreat from the peak observed in April 2022. The core PCE inflation, a measure closely watched by the Federal Reserve, has also dipped below expectations for December, registering a 2.9% year-over-year increase—its first sub-3% reading since 2021. This softening of inflationary pressures, juxtaposed with strong economic growth, injects a dose of optimism into the market, raising hopes for an imminent shift in the Federal Reserve's policy stance.

Investor attention is now fixated on the upcoming Federal Reserve meeting on January 31, with widespread expectations for interest rates to remain anchored at 5.25% - 5.5%. The recent favorable inflation data underscores the possibility that the current restrictive monetary policy may relax sooner rather than later. While market participants are pricing in multiple rate cuts in 2024, the Fed's own projections from December are more conservative, hinting at fewer adjustments to the policy rate.

The Federal Reserve, in its January assembly, is likely to recognize the progress on growth and inflation fronts but could temper market expectations for aggressive rate reductions. A measured approach, with three to four rate cuts envisaged for 2024, seems plausible, starting perhaps around mid-year as core inflation continues its downward trajectory. The Fed's strategy is expected to be cautious and gradual, to ensure that inflationary pressures do not resurface unexpectedly.

Historically, the commencement of a rate-cutting cycle by the Fed, in the absence of a recession, has been a harbinger of positive market performance. Since 1990, such periods have yielded an average 12-month return of around 7.6% on the S&P 500, a stark contrast to the meager 0.5% return during recessionary rate cuts. With the current economic data signaling a potential 'soft landing,' the stage is set for a favorable market environment as the Fed pivots towards easing.

The previous year's market rally, with the S&P 500 climbing 24%, was fueled by a combination of AI enthusiasm and a resilient economy, despite the Fed's aggressive rate hikes. However, market leadership was concentrated in a select few stocks and sectors. Looking ahead, a broader spectrum of equities and investment-grade bonds is expected to drive market returns as the Fed begins to cut rates. Volatility may present itself as the markets adjust, but it is also an opportunity to reposition for the anticipated broad-based market leadership.

In summary, the U.S. economy is on a robust path, with inflation showing signs of moderation. The Federal Reserve's upcoming meeting and policy decisions will be critical in shaping the economic outlook for 2024. Investors may well witness a soft landing scenario, which historically has been favorable for the markets. Caution and vigilance remain the watchwords as the Fed treads the fine line between fostering economic growth and keeping inflation in check.

Comments ()