Victoria's Secret & Co. (VSCO), Mid/Small Cap AI Study of the Week

April 18, 2024

Weekly AI Pick from the S&P 400 or S&P 600

Company Overview

Victoria's Secret & Co. (VSCO), known for its women's intimate apparel, beauty products, and other apparel, operates under the Victoria's Secret, PINK, and Adore Me brands. The company has a significant retail presence with approximately 910 stores in the U.S., Canada, and China, and over 460 international stores operated through franchise, license, and wholesale arrangements. The recent acquisition of Adore Me enhances their digital-first strategy, which is increasingly important as digital sales accounted for 33% of the company's 2023 revenue. Since separating from L Brands in 2021, VSCO has become an independent company listed on the NYSE.

The company generates revenue through royalties from franchise and license sales and recognizes wholesale revenues upon title transfer to partners. With a focus on product innovation, Victoria's Secret & Co. regularly introduces new products emphasizing quality and design, supported by a global supply chain that emphasizes speed and efficiency. Their advertising campaigns are inclusive, engaging diverse cultural elements across various media platforms.

Victoria's Secret & Co. is deeply committed to Diversity, Equity, and Inclusion (DEI), with initiatives aimed at workforce diversity, enhancing customer experiences, and supporting minority-owned suppliers. The company focuses on associate well-being, offering competitive benefits and equal compensation opportunities. They maintain strict compliance protocols, particularly concerning interactions with models and the overall safety of their workforce and customers.

The leadership team at Victoria's Secret & Co., led by CEO Martin Waters and CFO Timothy Johnson, brings a wealth of experience from the retail and technology sectors. The company is transparent with its financial and shareholder information, complying with SEC regulations and providing access to this data through their investor relations page and the SEC's website.

By the Numbers

Net sales (Annual): Decreased by $162 million, or 3%, to $6.182 billion in 2023.

- Direct sales (Annual): Increased by 9%.

- International sales (Annual): Increased by 16%.

- North American store sales (Annual): Decreased by 11%.

- Operating income (Annual): Decreased from $478 million in 2022 to $246 million in 2023.

- Operating income rate (Annual): Dropped from 7.5% to 4.0% of net sales.

- Adjusted operating income (Annual): Decreased from $566 million in 2022 to $327 million in 2023.

- Sales per average selling square foot and per store (Annual): Decreased by 11%.

- Total store count (Annual): Increased from 1,358 to 1,370.

- Gross profit (Annual): Decreased by $16 million to $2.242 billion.

- Gross profit rate (Annual): Improved to 36.3% from 35.6%.

- Operating expenses (Annual): Rose by 12% to $1.996 billion.

- Net cash provided by operating activities (Annual): Decreased from $437 million in 2022 to $389 million in 2023.

- Capital expenditures (Annual): $256 million in 2023, with an expected $230 million in 2024.

- Net cash outflow from financing activities (Annual): $291 million in 2023.

- Share repurchases (Annual): 3.7 million shares at an average price of $34.22 per share.

- Debt-to-capitalization ratio (Annual): Improved from 77% in 2023 to 73% in 2024.

Quarterly Report (Q3 2023):

- Operating loss (Quarterly): $67 million compared to an operating income of $43 million in the same quarter of the previous year.

- Net sales (Quarterly): Declined by 4% to $1.265 billion.

- Comparable sales (Quarterly): Decreased by 7%.

- North American store sales (Quarterly): Dropped by $90 million.

- Direct channel sales (Quarterly): Increased by 12%.

- Pre-tax charges (Quarterly): $29 million for restructuring and $22 million related to a legal matter.

- Gross profit (Quarterly): Decreased by $30 million.

- Operating expenses (Quarterly): Increased by 19%.

- Operating loss (Year-to-date): $13 million compared to an operating income of $234 million in the previous year.

- Net sales (Year-to-date): Down 5% to $4.099 billion.

- Gross profit (Year-to-date): Fell by $98 million to $1.416 billion.

- Operating expenses (Year-to-date): Increased by 12% to $1.429 billion.

- Interest expenses (Year-to-date): Increased due to higher debt levels and borrowing rates.

- Working capital (As of October 28, 2023): $268 million.

- Total capitalization (As of October 28, 2023): $1,750 million.

- Net decrease in cash from operating activities (Year-to-date): $(200) million.

- Capital expenditures (Year-to-date): $224 million.

- Share repurchases (Year-to-date): 3.652 million shares at an average price of $34.22, totaling $125 million.

- Total long-term debt (As of October 28, 2023): $1,530 million, net of the current portion.

- Transition from LIBOR to Term SOFR for interest calculations on debt.

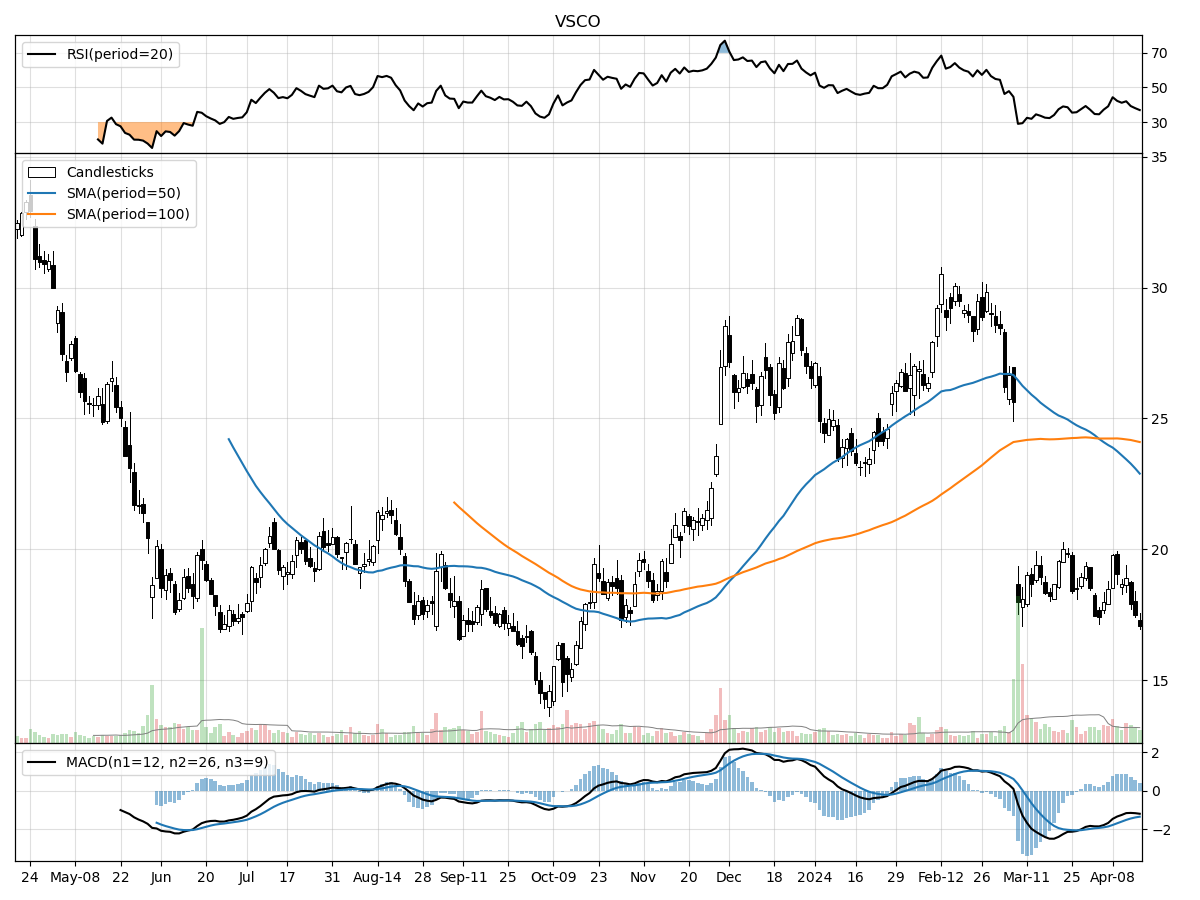

Stock Performance and Technical Analysis\

Based on the technical data provided, the stock appears to be experiencing a downward trend. The current stock price is 48% below its 52-week high, indicating that the stock has significantly retreated from its peak value over the past year. However, it's worth noting that the stock is still 19% above its 52-week low, suggesting that while the stock has been declining, it hasn't reached its lowest point in the past year, providing a potential cushion or support level.

The recent trading volume is slightly above the longer-term average, with about 275,088 shares traded daily compared to the longer-term average of 2,535,018 shares. This increased volume could be a sign of heightened investor interest or concern, potentially due to company-specific news or broader market conditions. However, the presence of moderate selling pressure and distribution, as indicated by the money flow indicators, suggests that more investors are selling their shares than buying, which can drive the price down.

The Moving Average Convergence Divergence (MACD) is a trend-following momentum indicator that shows the relationship between two moving averages of a stock’s price. A bearish MACD value of -1.34 indicates that the short-term momentum is declining at a faster rate than the long-term momentum, signaling bearish sentiment and that the stock price could continue to decline. This, combined with the recent price drops of 8.5% in the last month and 30.3% in the last three months, suggests that investors are not optimistic about the stock's immediate future.

In summary, the technical analysis paints a bearish outlook for the stock in the near term. Investors should be cautious and consider other factors, such as company fundamentals and market conditions, before making a decision to invest. It may also be prudent to watch for any potential changes in the indicators, such as a shift in the MACD to a more bullish signal or a reversal in selling pressure that could indicate a potential turnaround for the stock.

The ‘Bull’ Perspective

Invest in Victoria's Secret & Co. (VSCO): A Strategic Opportunity Amidst Market Volatility

Summary:

- Resilient Brand Presence: VSCO's brand equity, with a significant market share in the lingerie industry, is a testament to its enduring appeal, boasting millions in annual sales despite recent downturns.

- Strategic Restructuring and Acquisitions: The acquisition of Adore Me and strategic restructuring efforts are poised to streamline operations and bolster direct-to-consumer (DTC) sales.

- Digital and International Expansion: VSCO's 12% increase in DTC sales, coupled with a 13% rise in international revenue, signals robust growth potential in key markets.

- Aggressive Share Repurchase Program: The repurchase of 3.652 million shares at an average price of $34.22 reflects management's confidence in the company's intrinsic value.

- Adaptation to Market Trends and Consumer Behavior: With a focus on digital innovation and shifting consumer preferences, VSCO is adapting to the new retail landscape.

Elaboration:

- Resilient Brand Presence:

Victoria's Secret & Co. has long been a dominant player in the lingerie market, with a brand that resonates with consumers globally. Despite the recent $67 million operating loss, the company's net sales remain substantial at $1.265 billion. The brand's resilience is further exemplified by its ability to maintain a significant market share and customer loyalty in a highly competitive industry. This speaks to the strength of VSCO's brand equity and its potential for recovery, especially considering the overall retail sector's volatility and the impact of the COVID-19 pandemic on consumer behavior. - Strategic Restructuring and Acquisitions:

VSCO's proactive approach to restructuring, including a $29 million pre-tax charge for Q2 2022, demonstrates a commitment to operational efficiency and long-term profitability. The acquisition of Adore Me, a digitally native lingerie brand, is a strategic move that enhances VSCO's DTC channel, which has already seen a 12% increase in sales. This acquisition also diversifies the company's portfolio and targets a younger demographic, which is crucial for future growth. With these strategic initiatives, VSCO is well-positioned to capitalize on evolving retail dynamics and enhance shareholder value. - Digital and International Expansion:

The company's digital sales channel's growth, along with a 13% increase in international sales, underscores the success of VSCO's expansion strategy. The digital segment's growth is particularly noteworthy, as it reflects a successful pivot in a retail environment increasingly shifting online. This digital proficiency, combined with international market penetration, positions VSCO to capture a larger share of the global lingerie market, which is expected to continue its upward trajectory. - Aggressive Share Repurchase Program:

VSCO's share repurchase program, which saw the company buy back shares at an average price of $34.22, signals a strong belief by management in the company's undervalued stock. This repurchase program not only provides immediate returns to shareholders but also indicates potential for stock price appreciation. It's a vote of confidence that the company's strategic initiatives will lead to improved financial performance and, consequently, a higher market valuation. - Adaptation to Market Trends and Consumer Behavior:

VSCO's keen focus on aligning with market trends and evolving consumer preferences is evident in its strategic decisions. The company is adapting to a retail environment where convenience, personalization, and digital engagement are paramount. By investing in technology, enhancing its online presence, and adjusting its product offerings to meet consumer demand, VSCO is positioning itself to thrive in the post-pandemic retail landscape. Moreover, the company's efforts to manage costs and navigate through inflationary pressures and supply chain challenges demonstrate a robust strategic response to current market conditions.

Conclusion:

Victoria's Secret & Co. finds itself at a pivotal juncture, where market headwinds and internal challenges have led to a temporary setback. However, the company's strong brand presence, strategic restructuring, digital and international expansion, aggressive share repurchase program, and adaptation to consumer trends present a compelling case for investment. For investors with a keen eye on long-term growth and value creation, VSCO represents a strategic opportunity to invest in a resilient brand with a clear vision for the future. With a prudent approach to navigating risks and leveraging its strengths, Victoria's Secret & Co. is poised for a vibrant rebound in the evolving retail landscape.

The ‘Bear’ Perspective

Victoria's Secret & Co.: Navigating Through a Labyrinth of Risks

Summary:

- Financial Strain: Operating loss of $67 million in Q3 2023 and a 5% year-to-date net sales decline signal financial distress.

- Consumer Behavior Shifts: A 7% decrease in comparable sales and a 10-15% drop in U.S. store sales reflect changing consumer preferences.

- Debt Burden: With long-term debt at $1,530 million, financial flexibility is compromised, affecting growth and innovation potential.

- Market Volatility: Share price volatility, evidenced by recent stock market dips, could lead to investor wariness and reduced capital inflows.

- Competitive Pressures: Intense competition and the need to adapt to fast-changing retail trends could outpace VSCO's strategic initiatives.

1. Financial Strain

Victoria's Secret & Co.'s recent operating loss of $67 million in the third quarter of 2023, coupled with a 5% net sales decline year-to-date, paints a picture of a company in financial distress. The stark contrast to the $43 million operating income from the previous year's same quarter is alarming. When a company's operating losses widen, and sales trends are downward, it indicates significant headwinds in revenue generation and cost management. Considering the increased expenses by 19% due to marketing investments and integration costs of Adore Me, the company's ability to turn a profit seems increasingly challenging. These numbers are telltale signs that investors should be cautious, as the company's financial health is evidently under strain.

2. Consumer Behavior Shifts

The reported 7% decrease in comparable sales and a significant 10-15% decline in U.S. store sales suggest that Victoria's Secret & Co. is struggling to maintain its appeal among consumers. In an era where consumer preferences are rapidly evolving, a company's inability to keep pace can be detrimental. The $90 million drop in North American store sales due to lower traffic and conversion rates cannot be overlooked. The modest 12% increase in direct channel sales, though positive, does not offset the losses experienced at physical locations. These statistics highlight the urgent need for the company to revamp its marketing and product strategies to recapture market share and consumer interest.

3. Debt Burden

The company's reported long-term debt of $1,530 million, net of the current portion, is a heavy burden that could stifle its ability to invest in growth and innovation. High levels of debt can lead to increased interest expenses, which are already on the rise due to higher debt levels and borrowing rates. This financial leverage may limit the company's operational flexibility, forcing it to focus on debt servicing rather than strategic expansion or technological advancements. The debt situation is a red flag for potential investors, as it could lead to solvency issues if not managed prudently.

4. Market Volatility

Recent stock market fluctuations, as indicated by the S&P 500's pullback in response to higher-than-expected inflation readings, have created an environment of uncertainty. For a company like Victoria's Secret & Co., which has already been experiencing share price volatility, this could lead to further investor wariness. Market sentiment plays a crucial role in capital inflows, and the company's stock may be perceived as a higher-risk investment during such volatile times. The potential for reduced investor confidence and capital inflows could hamper the company's ability to raise funds for debt repayment or strategic initiatives.

5. Competitive Pressures

The retail landscape is fiercely competitive, and Victoria's Secret & Co. faces the relentless challenge of keeping up with rapidly changing trends. Competitors with more resources or a quicker adaptation to market shifts could easily overshadow VSCO's efforts. The need for constant innovation in products, marketing, and customer experience is critical in retaining market position. However, with the company's current financial and operational challenges, there is a significant risk that it may not be able to compete effectively. This could lead to further erosion of market share and profitability, as competitors capitalize on VSCO's weaknesses.

In conclusion, Victoria's Secret & Co. is navigating through a labyrinth of risks that warrant a cautious approach from investors. The combination of financial strain, changing consumer behaviors, a heavy debt load, market volatility, and competitive pressures creates a challenging environment for the company. Without a clear and effective strategy to address these issues, the potential for long-term success remains uncertain. Investors should weigh these risks carefully when considering their investment decisions regarding VSCO.

Comments ()