YETI Holdings, Inc. (YETI), Mid/Small Cap AI Study of the Week

March 26, 2024

Weekly AI Pick from the S&P 400 or S&P 600

Company Overview

YETI Holdings, Inc., based in Austin, Texas, specializes in high-quality outdoor products such as coolers, drinkware, bags, and apparel. The company, founded in 2006, is renowned for its durable hard coolers and has expanded its product range, with the majority of its 2023 net sales coming from Drinkware at 62%, followed by Coolers & Equipment at 36%, and Other at 2%. YETI sells its products through both wholesale and a robust direct-to-consumer (DTC) platform, with the latter accounting for a significant portion of its revenue.

The company targets outdoor enthusiasts and professionals, predominantly in North America, but is actively expanding its international footprint, particularly in Asia. YETI does not own manufacturing facilities but instead partners with specialized manufacturers globally, maintaining high standards for material quality and manufacturing processes. The brand is recognized for its innovative designs, which are protected by extensive intellectual property rights to combat counterfeit products.

YETI's sales peak in the fourth quarter due to seasonality and the company has a strong corporate culture with a commitment to innovation and community support. It employs around 1,050 people in eight countries, with most in the U.S., and has no union agreements or labor-related work stoppages. YETI is also dedicated to Diversity, Equity, and Inclusion (DE&I), with an internal council and initiatives aimed at creating an inclusive workplace. The company's operations are subject to global trade laws and regulations, which could significantly affect its business due to changes in tariffs or trade policies.

By the Numbers

Annual 10-K Report for Fiscal Year 2023:

- Net sales increased by 4% YOY, from $1,595.2 million in 2022 to $1,658.7 million in 2023.

- Gross profit rose by 24% to $943.2 million in 2023, up from $763.4 million in 2022.

- Gross margins improved by 900 basis points.

- Selling, general, and administrative (SG&A) expenses increased by 13%.

- Wholesale channel sales decreased by 2%.

- Direct-to-consumer (DTC) sales grew by 9%.

- SG&A expenses rose to $717.7 million in 2023.

- Net tax expense increased to $56.1 million.

- Cash flows from operating activities increased substantially to $285,942 thousand.

- Cash used in investing activities was $72,824 thousand.

- Cash used in financing activities decreased.

- A $300 million share repurchase program was announced.

- Anticipated capital expenditures for 2024 are around $60 million.

- A 10% variance in reserves for variable considerations could impact net sales by $1.2 million.

Quarterly 10-Q Report for Q3 2023:

- Net sales for Q3 2023 remained stable at $433.6 million.

- Gross profit for Q3 2023 increased by 13% to $251.3 million.

- Gross margin for Q3 2023 was 58%.

- SG&A expenses for Q3 2023 increased by 23%.

- Net income for Q3 2023 decreased slightly from $45.5 million in Q2 2022 to $42.7 million.

- Net sales for the nine-month period ending September 30, 2023, decreased by 1% to $1,138.9 million.

- DTC sales grew by 7% for the nine-month period.

- Wholesale sales fell by 10% for the nine-month period.

- Gross profit for the nine-month period increased by 5% to $627.9 million.

- SG&A expenses for the nine-month period rose by 17%.

- Cash balance as of September 30, 2023, was $281.4 million.

- Total outstanding debt was $83.3 million at a weighted average interest rate of 6.70%.

- Share repurchases amounted to $100.0 million.

- Cash flow from operations for the nine-month period was $114.769 million.

- Cash used for investing activities was $58.263 million for the nine-month period.

- Cash used for financing activities was $11.931 million for the nine-month period.

- Recall expense reserve was updated to $25.9 million.

These figures highlight YETI's financial performance, growth in sales, profitability, expense management, liquidity, and capital allocation strategies.

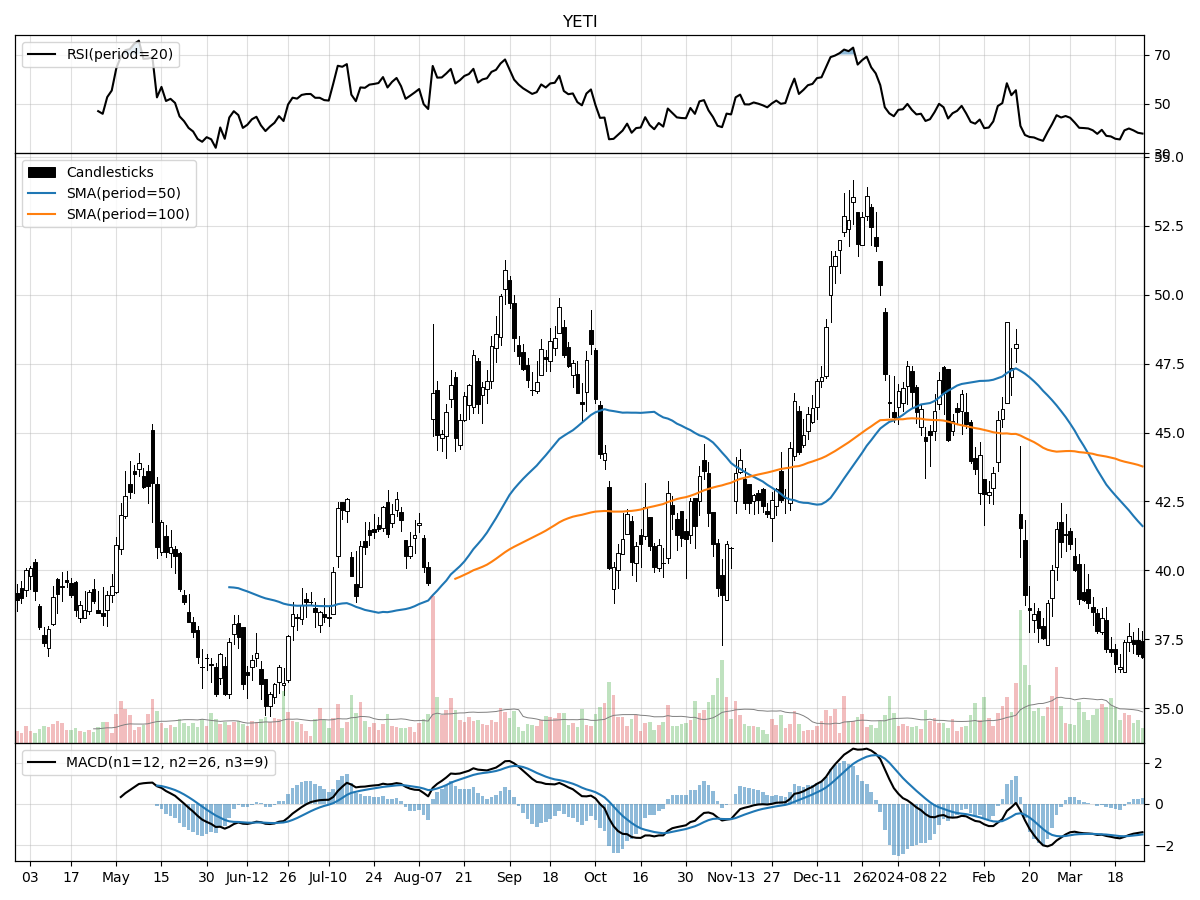

Stock Performance and Technical Analysis

Based on the provided technical indicators, the stock in question presents a somewhat bearish sentiment. The current stock price is relatively closer to its 52-week low, sitting only 4 percent above it, and substantially below its 52-week high by 31 percent. This suggests that the stock has not only retreated from its peak but is also not showing significant recovery strength as it hovers closer to its yearly low. The downward price movement of 11.25% over the last month and a more pronounced drop of 28.85% over the last three months further underscore the negative momentum that the stock has been experiencing.

The volume analysis offers a mixed signal. The recent daily volume is higher than the longer-term average, which could indicate increased investor interest or heightened activity due to price movement. However, in the context of a falling price, this could be a sign of a sell-off, as more shares are being traded in anticipation of further declines or as investors exit their positions.

The Money Flow indicators provide additional cause for caution. Heavy selling pressure and distribution suggest that larger traders or institutions may be reducing their positions or exiting altogether, which could be driving the stock price lower. This is reinforced by a bearish Moving Average Convergence Divergence (MACD) value of -1.48. The MACD is a trend-following momentum indicator that shows the relationship between two moving averages of a stock's price. A negative MACD indicates that the short-term average is below the long-term average, signaling downward momentum and potentially more declines to come.

In summary, while the stock currently presents an unfavorable technical picture, it is crucial for investors to consider the broader market context, the company's fundamentals, and any potential catalysts that could affect the stock's future performance. A bearish technical outlook may not be the sole determinant of investment decisions, but it certainly warrants caution and suggests the need for a comprehensive risk assessment before considering any investment.

The ‘Bull’ Perspective

Summary:

- Robust Financial Performance: YETI's Q3 2023 report showcases a strong gross margin of 58% and a 13% increase in gross profit, reflecting the company's ability to navigate supply chain disruptions and inflationary pressures.

- Strategic Product Expansion and Redesign: The introduction of new products and the redesign of the Hopper M Series Soft Coolers demonstrate YETI's commitment to innovation and safety, catering to evolving consumer demands.

- Solid Liquidity and Share Repurchase Program: With a cash balance of $281.4 million and a $300 million credit facility, YETI's financial health is robust, further bolstered by a $100.0 million share repurchase, signaling confidence to investors.

- Global Economic Indicators and Central Bank Policies: The latest FOMC projections and central bank rate decisions may create a favorable macroeconomic environment for YETI, supporting consumer spending and investment in durable goods.

- Mitigating Identified Risks: YETI's proactive approach to addressing its identified risks, such as supply chain management and intellectual property protection, positions the company to weather potential challenges effectively.

Elaboration on Points:

- Robust Financial Performance:

Despite the volatile economic landscape, YETI's financial resilience is evident in its Q3 2023 financial report. The company's gross margin impressively stands at 58%, with a gross profit surge of 13% to $251.3 million, despite supply chain challenges. This margin expansion is attributable to the stabilization of freight rates and a disciplined approach to product costs. Additionally, a 14% growth in direct-to-consumer sales underlines the strength of YETI's brand in a competitive market. While SG&A expenses rose by 23%, this was a strategic move to bolster distribution capabilities, a necessary investment for long-term growth. - Strategic Product Expansion and Redesign:

YETI's agility in product innovation and response to safety concerns is a testament to its strong market position. The launch of new cargo items and drinkware, along with a cast iron skillet, expands YETI's product portfolio, tapping into new customer segments and usage occasions. The redesign of the Hopper M Series Soft Coolers in response to a voluntary recall demonstrates the company's dedication to customer safety and satisfaction, which is essential for maintaining brand loyalty and trust. - Solid Liquidity and Share Repurchase Program:

The company's liquidity is more than adequate, with a cash balance of $281.4 million and an accessible $300 million credit facility. These resources provide YETI with the flexibility to invest in growth initiatives and navigate economic downturns. Furthermore, the company's decision to repurchase $100.0 million worth of shares underscores management's confidence in YETI's valuation and future prospects, which can be a positive signal for investors looking for stable investments with potential for capital appreciation. - Global Economic Indicators and Central Bank Policies:

The broader economic backdrop, characterized by the FOMC's projections of rate cuts and improved GDP growth forecasts for 2024-2026, suggests a more accommodative monetary policy environment ahead. This scenario bodes well for consumer discretionary companies like YETI, as lower interest rates typically spur consumer spending, particularly on high-quality durable goods. Moreover, the similar dovish stance of other central banks, such as the ECB and BoC, indicates a globally synchronized effort to support economic growth, which could enhance YETI's international market prospects. - Mitigating Identified Risks:

YETI is not immune to risks, but its proactive stance in addressing them is a critical factor in its investment case. The company's efforts to protect its intellectual property, manage its supply chain efficiently, and maintain a strong brand image are crucial in mitigating operational and market risks. By focusing on direct-to-consumer channels and international expansion, YETI is diversifying its revenue streams and reducing reliance on any single market or sales channel. These strategic moves, coupled with a keen eye on market trends and consumer preferences, allow YETI to adapt and thrive in a dynamic market environment.

In conclusion, YETI Holdings, Inc. presents a compelling investment opportunity for those seeking a resilient company with a track record of strong financial performance, strategic product innovation, robust liquidity, and proactive risk management. The company's ability to navigate economic headwinds, coupled with favorable macroeconomic trends, positions YETI to continue its growth trajectory and deliver value to its shareholders.

The ‘Bear’ Perspective

Why Investors Should Steer Clear of YETI Holdings, Inc.

- Stagnant Sales Growth: YETI's net sales have shown a concerning stagnation, with a mere 1% dip to $1,138.9 million in the nine-month period ending September 30, 2023.

- Rising SG&A Expenses: The company's SG&A expenses have surged by 17%, significantly outpacing sales growth and potentially eroding future profitability.

- Product Recall Impact: An $8.5 million increase in recall expense reserves due to safety issues with their Hopper M Series Soft Coolers could signal deeper issues with product quality and brand trust.

- Competitive and Economic Headwinds: YETI faces stiff competition in a market with low entry barriers, and the broader economic environment poses risks to consumer discretionary spending.

- Dependence on Key Personnel and Manufacturers: The success of YETI is highly reliant on its management team and a limited number of manufacturers, creating vulnerability to any disruptions.

Detailed Analysis

- Stagnant Sales Growth

YETI's financial performance has shown signs of stagnation, a red flag for investors looking for growth opportunities. With net sales nearly flatlining, down 1% to $1,138.9 million over nine months, there is a clear indication that the company is struggling to expand its market share and revenue base. In a market where innovation and growth are key drivers of success, YETI's inability to significantly increase its top-line figures could be a precursor to a long-term trend of underperformance. Considering the competitive nature of the outdoor products industry, stagnant sales can quickly turn into declining sales if consumer preferences shift or if competitors introduce more compelling product offerings. - Rising SG&A Expenses

The disproportionate rise in Selling, General, and Administrative (SG&A) expenses, which have jumped by 17%, cannot be overlooked. This increase has outstripped sales growth, suggesting that YETI is becoming less efficient in converting sales into profit. High SG&A expenses can be a drain on net income and may reflect costs that are not scaling effectively with the business. If this trend continues, it could squeeze margins and leave less room for investment in growth opportunities or product development, ultimately impacting shareholder returns. - Product Recall Impact

The $8.5 million increase in recall expense reserves for the Hopper M Series Soft Coolers is not just a financial setback; it's a hit to the company's reputation for quality and reliability. Product recalls can lead to consumer skepticism and brand erosion, which can be difficult and costly to repair. Moreover, such issues can divert management's attention from growth initiatives to crisis management, further stalling the company's progress. The preference for gift cards over product replacements, reflected in the recall expense reserve update, could also indicate a loss of customer confidence in the brand's product lineup. - Competitive and Economic Headwinds

Given the current economic landscape, with inflationary pressures, potential interest rate hikes, and geopolitical tensions, consumer spending, especially on discretionary items like YETI's products, could be significantly impacted. The company operates in a highly competitive market with low barriers to entry, meaning that any economic downturn could see consumers turning to cheaper alternatives. Additionally, the Federal Reserve's median projections for rate cuts in 2024 could signal a slower economic environment ahead, which traditionally leads to reduced consumer spending on non-essential goods. - Dependence on Key Personnel and Manufacturers

YETI's reliance on a few key personnel and manufacturers is a substantial risk. The loss of any key executive or disruption in its manufacturing base could lead to operational setbacks. The company's specialized product lineup requires skilled individuals for innovation and market strategy, and any gaps in this area could slow down product development and marketing efforts. Moreover, with manufacturing concentrated among a few suppliers, any logistical issues, labor disputes, or financial troubles faced by these manufacturers could disrupt YETI's supply chain, leading to stockouts, lost sales, and damage to the company's reputation for reliability.

In conclusion, while YETI Holdings, Inc. may have a strong brand and some positive financial indicators, the combination of stagnant sales growth, rising SG&A expenses, recent product recalls, competitive and economic headwinds, and reliance on key personnel and manufacturers presents a compelling case for investors to exercise caution. The potential risks associated with investing in YETI at this time appear to outweigh the potential rewards, suggesting that a "wait and see" approach may be the most prudent course of action.

Comments ()